Keefe Bruyette analyst Catherine Mealor has raised her rating for Synovus (SNV, Financial), moving it from Market Perform to Outperform. Alongside this upgrade, the price target has been increased to $65 from the previous $58. This positive outlook follows Synovus's stronger than expected performance in the second quarter, which exceeded expectations due to robust fees and provisions.

The analyst notes that Synovus is reaping the benefits of its "SynovusGo" initiative, which is contributing to earnings growth, while the bank continues to keep expenses in check. With consistent net revenue growth and stable credit conditions, Keefe Bruyette suggests that the stock’s valuation is poised for an upward trajectory.

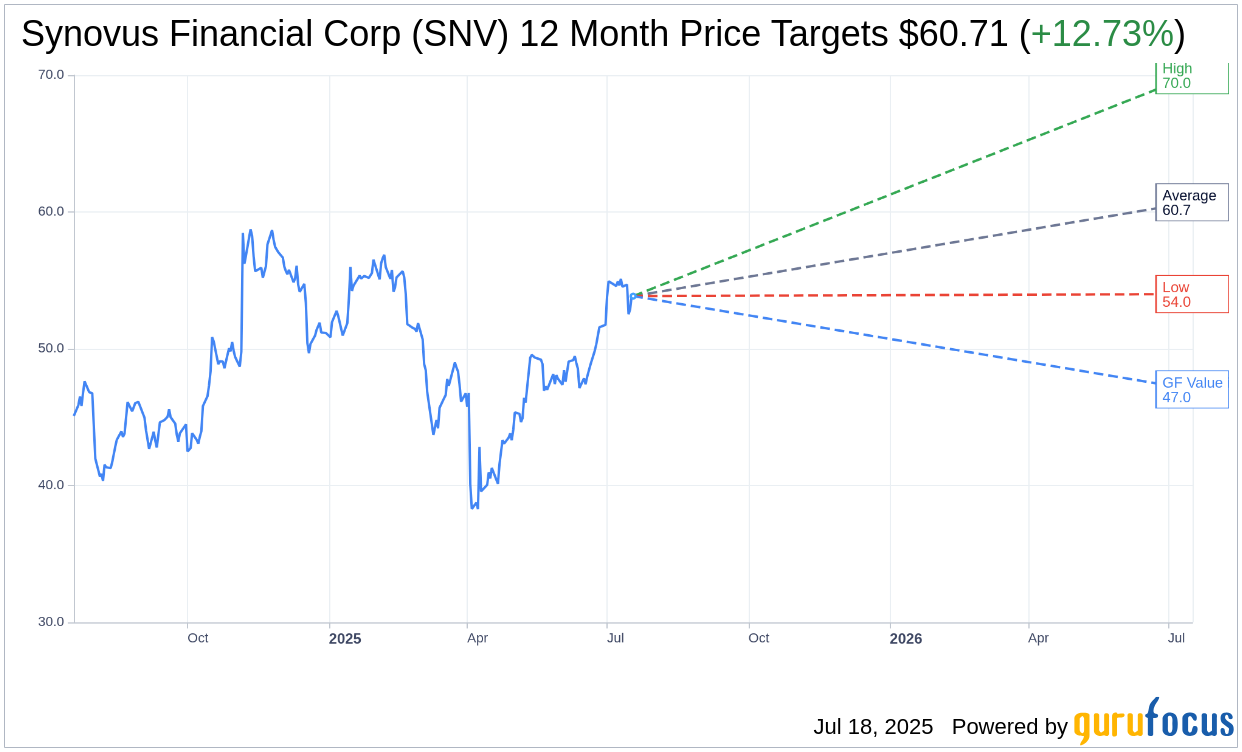

Wall Street Analysts Forecast

Based on the one-year price targets offered by 17 analysts, the average target price for Synovus Financial Corp (SNV, Financial) is $60.71 with a high estimate of $70.00 and a low estimate of $54.00. The average target implies an upside of 12.73% from the current price of $53.85. More detailed estimate data can be found on the Synovus Financial Corp (SNV) Forecast page.

Based on the consensus recommendation from 19 brokerage firms, Synovus Financial Corp's (SNV, Financial) average brokerage recommendation is currently 2.2, indicating "Outperform" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Synovus Financial Corp (SNV, Financial) in one year is $47.03, suggesting a downside of 12.66% from the current price of $53.85. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Synovus Financial Corp (SNV) Summary page.

SNV Key Business Developments

Release Date: July 17, 2025

- GAAP and Adjusted Earnings Per Share: $1.48, with adjusted EPS up 14% from Q1 and 28% year-over-year.

- Adjusted Preprovision Net Revenue: Increased 5% sequentially and 7% year-over-year.

- Net Interest Margin (NIM): Expanded 2 basis points to 3.37%.

- Loan Growth: Period-end loan balances up $888 million or 2% from Q1.

- Loan Production: Funded production increased 34% quarter-over-quarter and 60% year-over-year.

- Core Deposits: Declined $788 million or 2% from Q1.

- Average Cost of Deposits: Declined 4 basis points to 2.22%.

- Adjusted Noninterest Revenue: $131 million, up 12% sequentially and 3% year-over-year.

- Adjusted Noninterest Expense: Increased 1% sequentially and 3% year-over-year.

- Net Charge-Offs: $18 million or 17 basis points, improved from previous guidance.

- Non-Performing Loans: Improved to 0.59% of total loans from 0.67% in Q1.

- Allowance for Credit Losses: Ended at 1.18%, down from 1.24% in March.

- Common Equity Tier 1 Ratio: 10.91%, highest in company history.

- Total Risk-Based Capital: 13.74%.

- Share Repurchases: $21 million completed in Q2.

- Tax Rate: Approximately 21% in Q2, expected between 21% and 22% for full year 2025.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Synovus Financial Corp (SNV, Financial) reported strong second quarter 2025 results with GAAP and adjusted earnings per share of $1.48, marking a 28% year-over-year increase.

- The company experienced healthy net interest margin expansion and lower provision for credit losses, contributing to year-over-year earnings growth.

- Loan growth was robust, with a 60% year-over-year increase in total funded loan production, the highest since the third quarter of 2022.

- Synovus Financial Corp (SNV) continues to execute well on its 2025 strategic initiatives, including the accelerated hiring of relationship managers, adding 12 new commercial bankers in the second quarter.

- The company achieved a 6% year-over-year net interest income growth, driven by net interest margin expansion and a decline in the cost of deposits.

Negative Points

- Core deposits declined by $788 million or 2% from the first quarter, including a $405 million drop in public funds.

- Time deposits and interest-bearing demand deposits decreased, partially offset by growth in noninterest-bearing deposits.

- The allowance for credit losses declined due to positive credit trends but was partially offset by a more adverse economic outlook.

- The company anticipates short-term pressure on the margin due to the timing lag between loan and deposit repricing during the easing cycle.

- Despite strong performance, Synovus Financial Corp (SNV) faces ongoing competition for loans and talent, which could impact pricing and growth.