At Simply Safe Dividends, we love nothing more than to find an easy-to-understand, time-tested, high quality dividend grower trading at a reasonable valuation. Not surprisingly, we frequently review our list of all 52 dividend aristocrats to hunt for companies that have demonstrated great consistency. During our review, we look for businesses with strong competitive advantages that protect current cash flow and, importantly, allow a company to continue growing its earnings over long periods of time.

In the case of Walmart (WMT, Financial), there is no doubt it has substantial competitive advantages. With over $485 billion in sales last year, Walmart sold the equivalent of $66.53 worth of merchandise to every single person in the world ($485.7 billion in sales divided by an estimated global population of 7.3 billion).

Let that sink in for a moment –Â $66.53 of revenue for every living person on the planet.

Walmart's massive sales base comes with many benefits and demands specialized skills that have allowed the company to dominate the brick and mortar retail market. The company's brand recognition, supply chain expertise, and 300-plus strategically placed distribution centers around the world are hard to replicate.

Most importantly, Walmart's sheer size gives it the sales volume and purchasing power necessary to be a genuine price leader in many merchandise categories. Few companies will ever be able to compete with Walmart's scale in the brick-and-mortar space, but the online world of ecommerce is changing the game.

Almost every Walmart investor knows about Amazon (AMZN, Financial), but few might realize the actual amount of products sold through its platform and what that might mean for Walmart's key competitive advantage as we think about the next decade.

Amazon did about $89 billion in reported sales last year. However, what many investors miss is that this figure represents Amazon's net sales, recognizing the products Amazon directly sells but only the fees it collects from third-party sellers (not the actual value of the merchandise they sold). In other words, it is not an apples-to-apples comparison with Walmart's $485 billion sales.

Of Amazon's $89 billion in revenue last year, $18.9 billion was generated by "service sales," which include third-party seller fees (it also includes sales from digital content subscriptions and Amazon Web Services). Third-party merchants accounted for over 40% of the items sold on Amazon last year, but Amazon "only" collects and records between 8% and 15% of each sale they make as its own revenue.

To estimate total third-party fee revenue, we need to further dissect the components of Amazon's service revenue. The company disclosed that its cloud business did $4.6 billion in sales last year, which leaves remaining service revenue at $14.3 billion. Some of this accounts for digital content and Amazon prime membership fees, so we will estimate a range of collected third-party fees of between $8 billion and $12 billion (see table below).

Given the 8% to 15% fee Amazon collects from each third-party sale, according to an Amazon spokesman, we can see that the gross product sales made by third parties selling through Amazon could be somewhere between $53 billion and $150 billion. Adding these amounts to Amazon's total product sales last year of $70 billion yields total estimated product sales made through Amazon of $123 billion to $220 billion. This compares to Walmart's total sales of $485 billion.

Source: Simply Safe Dividends

While Amazon's gross product sales are still far below Walmart's, Amazon's total sales are growing 15% to 20% per year. Depending on growth assumptions, the total value of products sold through Amazon could match Walmart's within the next decade. Amazon's online business is already more than 6x larger than Walmart's ecommerce operations, and Amazon sells more than 300 million items compared to less than 10 million available at Walmart.com. Walmart has a lot of catching up to do (i.e. more unprofitable ecommerce investments for years to come).

Importantly, Amazon doesn't have nearly as much brick-and-mortar space (just its huge network of distribution hubs and warehouses) and can rely more on robots rather than increasingly expensive storefront labor, keeping its cost structure significantly lower than Walmart's once it decides to slow its growth investments. With an ever-growing distribution reach, including the rollout of same-day delivery in several large cities, we think Amazon could increasingly challenge many of Walmart's product categories that were previously thought to be untouchable by ecommerce, such as grocery items (over 50% of Walmart's sales).

While these are very long-term concerns, it underscores the importance of Walmart successfully executing on its own ecommerce business to avoid getting left in the dust. A simple walk through any of Walmart's stores gives us skepticism that the company has the level of innovation and organizational abilities needed to compete with Amazon online.

While the continued rise of Amazon is making incremental sales growth a bit harder at Walmart today, it's not the primary reason why we didn't like this solid dividend payer earlier this year.

Why we passed on Walmartin August

We first reviwed Walmart in mid-August, passing on the stock over fears that its profit growth was stalling out. The company's most recent earnings release reinforced our concerns, and we were surprised to see such a historically stable stock plunge by 10% on the date of its announcement. With all dividend aristocrats, especially those that appear "cheap," it is extremely important to look at the next 10 years rather than the last and take an objective assessment of how the world is changing.

Let's review our rationale for recommending avoiding the stock several months ago –Â concerns about rising labor and healthcare costs.

Nationwide, where Walmart generates about 80% of its income, pressure has been building to gradually raise federal minimum wages from $7.25 an hour to $15 an hour. Even at $15 an hour, pay would still be below average private sector pay of $22 an hour. From New York to Oregon, different political figures have already proposed hiking the minimum wage in certain industries to $15 an hour.

Earlier this year, Walmart announced that it would raise the starting wage of its employees to $9 an hour in 2015 and get up to a minimum of $10 an hour by next year. Walmart anticipates $1 billion in additional expenses in fiscal 2016 as a result, which will likely prevent the company from leveraging operating expenses yet again.

It should also be noted that rising healthcare costs pose additional risk to profits –Â employers spent an average of $11,204 per worker for health benefits in 2014, up 4.6% from a year earlier, according to Mercer. Indeed, Walmart had bigger health care costs than it anticipated, enrolling more workers and experiencing faster-rising costs than expected; the company said its health care expenses would increase $500 million last year, equal to about 2% of its operating income. Note that about 60% of Walmart's 2.2 million workers are full time.

We dug into Walmart's financial statements to estimate the impact continually rising wages and healthcare costs might have on overall profitability, especially in light of the company's sluggish sales growth. In fiscal year 2015, Walmart reported about $117 billion gross profit, $93.5 billion in operating expenses and $23.6 billion in pretax operating income. While the company does not explicitly break out labor costs, we can estimate what proportion of operating expenses ("opex") they account for.

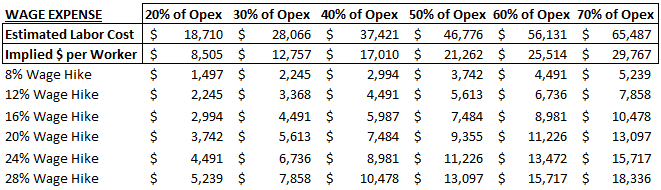

Each column in the table below assumes a different percentage of opex represents the bulk of Walmart's annual labor costs. In the first column, "20% of Opex," the "Estimated Labor Cost" is simply the $93.5 billion in fiscal year 2015 operating expenses multiplied by 20%, or $18.7 billion in estimated labor cost. With 2.2 million employees, that amounts to $8,505 per employee, which seems low.

Regardless, you can see the incremental operating expense that would be associated with different wage increases, ranging from an 8% wage hike to a 28% wage hike for sensitivity purposes. In our table, the minimum cost increase estimate would be about $1.5 billion (20% of Opex, 8% wage hike) but ranges up to over $18 billion. If the government raised the federal minimum wage to $15 an hour over the next 10 years, wages would increase at an 8% annualized rate (from the current $7.25 minimum wage). Over five years, the annual increase jumps to 16%. Walmart is a bit ahead of this with its announcement earlier this year, which will put its minimum wage at about $10 by next year (double-digit annual increases).

(click to enlarge)

Source: Simply Safe Dividends

This is a problem because Walmart's same-store growth has stalled out (or come at the expense of gross profit, like we saw with Q2 results) while square footage growth is likely to decelerate below 3% per year going forward. With labor being such a material cost for Walmart, we are not sure if the company will be able to leverage operating expenses for at least the next several years, especially in light of increasing ecommerce investments. This would mean minimal, if any, profit growth.

In our analysis below, we give Walmart credit for growing sales at a 3% clip while maintaining historical gross margins, which could prove to be generous. We can see that the company would generate $3 billion to $4 billion in incremental gross profit each year in such a scenario. However, looking back at the wage expense table above, we can see that incremental wage expenses wipe out most, if not all, incremental gross profit in many scenarios. And this doesn't even begin to account for increasing ecommerce costs. If Walmart cannot figure out a way to rejuvenate sales growth without hurting gross margins, the next five years could be tough with increased labor and healthcare laws.

Source: Simply Safe Dividends

As previously mentioned, the company's recent earnings reports have showed higher same-store sales growth coming at the expense of gross margins – lower prices are an easy way to draw in traffic and make growth look better, but margins are taking a hit. It remains uncertain if Walmart can sustain positive same-store sales growth without hurting margins in light of rising ecommerce competitive threats.

While we only looked at a few impacts from a potential rise in the federal minimum wage, such a move would likely change many variables –Â for example, labor turnover could drop and layoffs could increase to recoup some of the extra expense (although layoffs might ultimately hurt store service and same-store growth), or people might have more to spend at Walmart.

However, Walmart's results last week suggest the company will be unable to offset these headwinds for quite some time. It provided guidance for its earnings to fall by as much as 12% next year as it combats rising wage costs, ecommerce investments and store improvements.

Valuation and closing thoughts

Walmart now trades at 13x forward earnings estimates, valuing its earnings at a multiple similar to what low/no-growth telecom stocks AT&T (T, Financial) –Â 12.9x forward earnings –Â and Verizon (VZ, Financial) –Â 11.5x –Â trade at.

We see no clear path for Walmart to begin growing its earnings again. Labor costs are rising much faster than sales growth and account for a large proportion of total costs. Layoffs would result in even worse service at Walmart (hard to imagine), and automation investments would take a long time to pay off.

The company's sales base is extremely large and under stress from Amazon across numerous product categories. Walmart has yet to show it can grow same-store sales without giving up gross margin (i.e. its sales have only grown when it has been extremely promotional on pricing). Its ecommerce operations are years away from breaking even, assuming management hasn't over-promised (we see risk here – look at Amazon's profits or lack thereof). Unless inflation trends surprise to the upside (over 50% of Walmart's sales are grocery items), it's hard for us to see Walmart returning to profitable sales growth.

Is Walmart's downside risk limited at today's stock price? We believe it is. However, we prefer to invest in companies that can profitably grow in size, rewarding shareholders along the way with dividend growth and long-term capital appreciation.

As seen below, Walmart's annualized dividend growth rate has significantly slowed over the last decade, coming in at a paltry 2% most recently.

(click to enlarge)

Source: Simply Safe Dividends

While the dividend is extremely safe (40% payout ratio; healthy free cash flow generation; conservative balance sheet), we don't see a clear path for Walmart to grow earnings or command a higher multiple from the market.

As such, we will stick with the high quality dividend stocks we own in our Top 20 Dividend Stocks list.