At the worst possible time American International Group (AIG, Financial) missed its earnings estimates. It is one thing to miss but to miss it just a few days after Carl Icahn (Trades, Portfolio) releases a letter he sent to the CEO, that is bad. The company reported an after-tax operating profit of $691 million which contrasts with a $1.7 billion in the same quarter last year. AIG attributes the result to its hedge fund investments and its stakes in Chinese insurance companies. AIG also took a $274 million restructuring charge associated with organizational simplification, operational efficiency and business rationalization. Carl Icahn (Trades, Portfolio) will be happy to hear. In other good news the company also continued its buybacks in Q3.

The disappointing results increase the odds Carl Icahn (Trades, Portfolio) will get things done with his 2% stake in the insurance giant. Let’s take a look at the letter he sent to the CEO and the points he is making to see if it makes sense and this is an opportune time to buy or add AIG. Below I will excerpt certain parts of Icahn’s letter and comment on these parts:

The company continues to severely underperform its peers and is now facing an increasingly onerous regulatory burden which will only further erode its competitive position. Despite definitive action on the part of Congress and regulators to encourage this company to become smaller and simpler by splitting up, you have shown no sign of urgency and have chosen a “wait and see…for years” strategy void of decisive leadership. As a result AIG consistently trades at a substantial discount to book value.

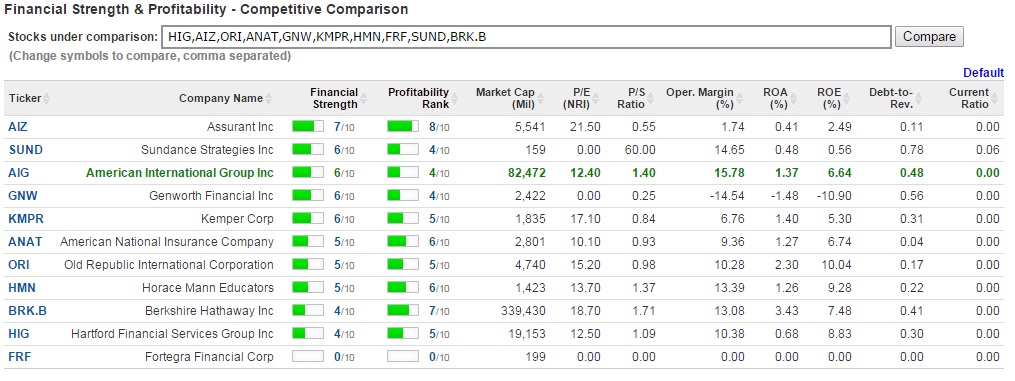

To check whether Icahn was right, I pulled up the Gurufocus competitive comparison tool (see image below). AIG has solid operational margins, but it is not delivering sound ROA and ROE numbers with those margins. The company does trade at a discount-to-book value and if Icahn is right about the cause and the remedy, a split would indeed result in at least a 25% increase of the share price.

It is a “no-brainer” that the simple act of splitting this company up will greatly enhance shareholder value. AIG should immediately:

Pursue tax-free separations of both its life and mortgage insurance subsidiaries to create three independent public companies. Each would be small enough to mitigate and avert the Systemically Important Financial Institution (“SIFI”) designation.

Embark on a much-needed cost control program to close the gap with peers.

I can see Icahn’s point that avoiding the SIFI designation could save a lot of shareholders money, but at the very least there are scale advantages that mitigate those savings to some extent. Overhead is also spread across a larger base of business. At the same time I have to admit big institutions are notorious for bloating overhead beyond what is reasonable.

The company is already on a cost-cutting program. It is cutting jobs and expects its restructuring to add $500 million in pretax income on an annual basis. I am not immediately convinced because Icahn says so; the company can do better.

Despite years of dismantling and selling noncore assets, AIG is still too large. The combination of life insurance and P&C insurance into a single entity offers no net benefit to shareholders (proven by industry low ROE), a fact that has driven other major multiline insurers to aggressively focus on a single line of business. We believe you must acknowledge that the current multiline strategy is not generating competitive returns. Separate monoline companies will be more focused, more efficient, generate better returns and, as a result, command significantly higher market valuations.

Icahn has a point that the ROE achieved over the past few years, given AIG’s scale, is not particularly satisfying. Icahn believes that, due to AIG’s size and interconnectedness, the FSOC council rules AIG a nonbank SIFI, which puts it under FED oversight and increases its capital requirement. That is a biggy. CEOs, in general, do not like to shrink the business they are running. It puts downward pressure on their salaries (a cool $12 million in 2014). CEO Peter Hancock does not own such a large pack of shares that it is obviously in his best interest to divide the company in three parts.

AIG’s ROE is below its peers not only because of size and capital constraints, but also because of lack of cost control. You have acknowledged that returns are below peers and must be improved, even going so far as to provide a long-term ROE goal of 10%, which is still below peers. At the same time you have suggested returns would not increase by more than 0.5% per year. Amazingly you have turned the quest for a 10% ROE into a half-decade journey. The one thing we do agree on is AIG’s lack of competitiveness. Do you honestly think now is not the time for the inevitable AIG transformation? You must be proactive and commit to closing 100% of the ROE gap between AIG and its peers.

On the cost side of things, I find Icahn’s arguments less compelling as compared to his objections to the regulation the company subjects itself too. ROE is also dependent on investment returns and although AIG should not be disadvantaged compared to its peer group, it could easily underperform for a period of time on this part of its business and it would severely affect ROE. Icahn does not make a strong case where costs could be cut without detriment to the operational side of the insurer. Having said all that, AIG is still widely held by gurus like: Berkowitz, Paulson, Perry and Loeb, among others. It is trading significantly below book value and missing its earnings estimates will mean large shareholders are more likely to side with Icahn.

Also check out: