Guru John Rogers (Trades, Portfolio) is the founder of Ariel Investment LLC. His specialty is in undervalued small and medium-sized companies. Rogers favors companies that are statistically cheap when comparing the price of their stock to potential earnings or when comparing the price of the stocks to the intrinsic values of the stocks. His portfolio is monitored on GuruFocus and I want to highlight one specific company he holds, an $800 million market cap called Bristow Group (BRS, Financial).

Rogers believes the energy industry is bottoming out and is actively looking for interesting stocks in the space. However, he is not ready yet to take on the full risk associated with these commodity producers. Instead he looks carefully at other companies in the chain. Bristow Group provides helicopter services to the offshore industry, flying personnel to and from helicopter pads. It’s active in many major drilling regions from the North Sea to Nigeria and the U.S. Gulf of Mexico but also Alaska, Australia, Brazil, Russia and Trinidad.

Due to the prolonged low oil price environment, the stock price of Bristow has been decimated. The company also admits this downturn is more problematic than initially anticipated. Management is now actively taking measures to improve balance sheet health and announced several specific operational measures this month:

- We are right-sizing the business for an extended downturn, pulling levers including:

- Operating expense reductions especially G & A.

- Capex deferral as we rely on our mostly owned, modern fleet.

- Focusing on successful implementation of U.K. SAR (including additional required investment).

- These actions should help us mitigate the challenges faced by our clients while maintaining our leadership position to compete in the offshore services industry.

Just like Rogers, I have been interested in the oil and gas selloff and picking up a company here or there that has sold off with it but is not actually exposed to the extent the market thinks it is.

Bristow Group is one company I looked at but ultimately I preferred its competitor, Era Group (ERA, Financial). The underlying thesis is exactly the same. Yes, these companies' earnings and outlooks are hurt as offshore operators dial back investments, but they have sold off undeservedly far. Bristow oil and gas contracts, for example, earn on average 65% of revenue whether reserved capacity is used or not. This is because contracts incorporate both a fixed monthly charge and a variable fee based on flight hours and a fuel pass through.

What attracts me to this industry is the underlying value of the operated assets. Bristow owns most of its helicopters, and these tend to hold value really well. Helicopters are a fairly liquid asset, and they are multifunctional. Even if oil and gas don’t come back, these machines have real value and could be utilized in other industries like search and rescue, media and private transport.

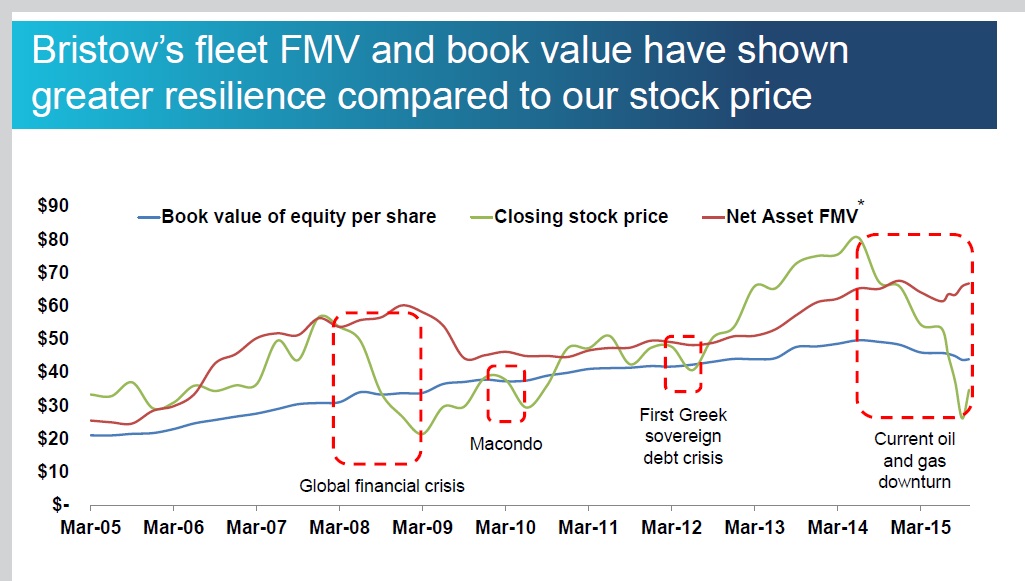

The chart below, provided by the company, illustrates this point well. At the current share price of about $24, the company trades at a deep discount to the actual net asset fair market value of its helicopter fleet, which is above $60. The chart also illustrates that it’s fairly common for the stock to trade near that fair value or even above it like it did in 2013 and 2014.

The company isn't expensive on the traditional metrics. Its forward P/E is under 9x, P/S is only 0.47x, P/B is only 0.52 and even on an Enterprise Value/EBITDA basis it isn't expensive at 7.18x. However, in this specific instance, it could be more useful to look at the aforementioned net asset values. Earnings may very well remain unimpressive for awhile, but these assets are real and their value less volatile and random compared to their earnings power.

Theoretically when the company is liquidated on the spot, shareholders should reap a nice profit after the $1 billion of debt is paid off. Potentially, buying the entire company is also much cheaper as compared to investing in new builds which opens up the possiblity of a takeover. This knowledge combined with a good level of insider ownership at approximately 20% convinces me this is one of Rogers' more interesting picks.

Also check out: