Recently, Scion Asset Management, the hedge fund founded by Michael Burry, one of the key protagonists from "The Big Short", reported on its long holdings. An earlier GuruFocus article highlighted his heavy weighting toward financials; however, his single largest position is in Nexpoint Residential Trust (NXRT, Financial). With its $283 million market cap, it’s a tiny company in the REIT space that specializes in residential multifamily real estate.

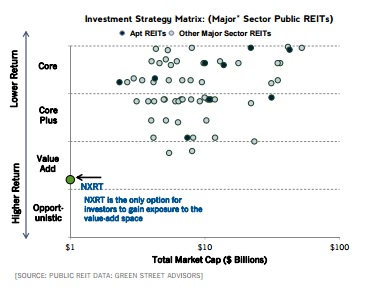

Curious what attracted Burry to the company, I went digging through the company’s materials on its investor relations site. Nexpoint is the only REIT in Burry’s portfolio, and Nexpoints claims to be the only REIT with a value-added strategy, which it claims generated ROI north of 20%.

The company focuses on residential real estate because declining home ownership and increasing student debt support the strong current demand for residential rentals. Meanwhile, new supply is only very slowly being added. According to the company, completions add under 2% per year to the existing stock until 2019 at least.

To achieve its ambitious return targets, management buys underperforming, under-capitalized properties and upgrades them in order to be able to raise the rents and extract market rates. The strategy probably doesn’t scale up without limitations, but given the company’s tiny market cap, it could have some runway left. Most of the value creation hasn’t taken place yet, to quote from the company’s presentation:

Current and Planned Value-Add: As of March 31, 2015, NXRT has planned to upgrade a total of 7,797 units of the 11,816 units owned* As of March 31, 2015, we have upgraded a total of 610 units Average cost per upgraded unit is $4,014 Average rent premium per upgraded unit: $83 Average return on investment: 24.6% (range: 13.9% - 41.1%)

One reason the company could be valued below its intrinsic value is because investors are overly fearful of the impact of the oil bust on the company’s risk profile. The company is associated with the Houston market, but the city actually makes up less than 2% of the company’s number of properties and contributes below 3% to NOI. The company actually views the oil bust as a net positive because it reduces risk as most of its tenants effectively received a tax cut.

From a valuation perspective, the company is a screaming buy if it is able to achieve anywhere near its ambitious return on investment goals. A company with such capable and ambitious management would deserve to trade at a multiple well-above book value, but in fact Nexpoint trades at a discount to net asset value, which the company estimates to be somewhere between $15.71 and $19.61 per share.

Disclosure: Long NXRT.