Reviewing the changes to Murray Stahl (Trades, Portfolio)’s portfolio I noticed a particularly interesting buy: The Nuveen Energy MLP Total Return Fund. A levered closed end-fund investing in MLPs. Where did we hear this before?

Last week I wrote an article about Bill Gross' stock picks and one of his strategies encompasses buying levered CEFs. The rationale given by the Bond King, being the low interest rate environment, makes it highly advantageous to make investments that benefit from borrowing but where it's nonrecourse to you. That way you participate in the upside of the cheap leverage but run less risk.

This is just like something the highly theoretical Stahl would figure out as well. Bond recommendations (see the previous article) involved less risky type of funds that included lots of bonds, but Stahl isn’t a bond investor, of course, and has previously announced he is looking at ways to invest in resource companies.

The Nuveen Energy MLP Total Return Fund is run by an experienced management team from Advisory Research who have been in the MLP space since 1995. They first identify broad investment themes and trends in the space and proceed with bottom-up analysis to find high quality, undervalued investments.

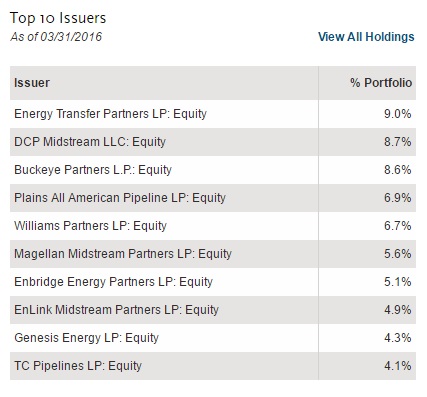

Currently the fund has significant positions in Energy Transfer Partners LP, DCP Midstream, Buckeye Partners LP, Plains All American Pipeline LP, Williams Partners LP, Magellan Midstream Partners LP, Enbridge Energy Partners LP, EnLink Midstream Partners LP, Genesis Energy LP and TC Pipeline LP (see table below):

Since its inception in 2011 the company has posted negative returns but to be fair this has been a difficult stretch. The fund also charges sizable fees of 1.6% per annum but on the bright side it carries a bunch of deferred tax benefits. These deferred tax benefits are very interesting. Morningstar did a great job of explaining how the tax treatment of an MLP CEF structured as a C-corporation works back in 2011 (when most of them traded at a premium to NAV):

NAV is simply a fund's assets minus its liabilities. In balance sheet accounting, net assets are a synonym for equity: Assets = Liabilities + Equity (aka net assets).

Most funds and corporations that pay taxes have a liability item titled "net deferred tax liabilities," or DTLs. This is because corporate accounting under generally accepted accounting principles, or GAAP, used for presenting corporate financial statements differs from tax accounting. This liability item reconciles what are estimated to be temporary differences between GAAP and tax accounting. In actuality, if the fund were ever to liquidate or the portfolio managers were to sell every holding in the fund, the liability would be realized and the fund would have to pay this as tax. Because this is a liability, when it's placed in the equation above, the net assets –Â the published NAV –Â is decreased. In other words, unless the portfolio is going to be liquidated or completely sold, the published NAV for CEFs with net DTLs is depressed.

What makes it attractive in my opinion, besides the experienced management, is the 20% leverage and the 6% discount to NAV (which in reality is much higher). This results in an annual distribution level of 14%-plus.