The first time I read about Google (GOOG, Financial)(GOOGL, Financial) Apps for Work being gradually pushed out of the top-three position in the "business productivity suite" segment by Microsoft (MSFT, Financial)'s Office 365, I didn’t understand the implications. Perhaps my experience with Google Apps biased my outlook, but the full extent of what that meant only hit me recently.

When I started looking deeper into the matter, things started to fall into place. I was able to see how astutely Microsoft has been growing past Google’s No. 3 position and even decimating salesforce.com (CRM) and Box, the top-two Softward as a Service applications in the world.

I also dug up some very interesting things about pricing strategies for both Office 365 as well as Google Apps, which I’ll explain in a minute. But most importantly, I discovered that Microsoft’s SaaS strategy would go a long way in supporting its long-term objective of mobile first, cloud first.

For the Uninitiated

I’ve found that a lot of very savvy investors are completely unaware of the potential of Software as a Service. Even though such applications are a part of our daily lives, when it comes to linking them to investment opportunities, few investors know the reality of this segment. For that reason, I’ll first cover the basics of productivity software served via the cloud over the internet.

A productivity suite is essentially a set of software applications that increase employee efficiency and reduce IT investment costs for a business. From a cloud perspective, this is very different from virtual machines, where data is hosted off-site. In essence, it is a cloud environment that is pre-fitted with software utilities that enable collaboration between employees, facilitate voice and email communication internally and externally, and provide the tools necessary for documentation and so on.

In addition, this has to be done in a secure environment where access can be highly controlled. This is what it typically looks like:

As you can see, there’s a foundation on which the actual applications for the workloads stand, and this is comprised of data security, mobility and overall governance of the system in question. In addition, accessibility is a key consideration because today’s corporate employees aren’t always placed in the same location. There are multiple offices, and most executives need to carry around their data and communications tools wherever they go.

Therefore, it would seem like Google has an edge over Microsoft because their Apps have the advantage of being integrated with the Chrome browser. With a single login, users can access any of their tools, including Drive, Gmail, etc.

Until cloud accessibility came along, Microsoft was at a severe disadvantage. It had a bunch of standalone applications that couldn’t be served as easily as they wanted over the internet, and it didn’t have the browser edge Google did.

Today, things are different. Microsoft has taken its one major trump card and used it to transition people to Office 365. That trump card is the Microsoft Exchange Server.

The bulk of enterprise-level companies were already using Exchange for their email needs, so it was a simple marketing pitch for them to make.

Essentially, this is what they were telling their customers: “Hey, let’s take the cost burden off of you and allow you to do away with multiple tools and multiple vendors. In exchange, we’ll give you all the tools you need on the cloud, and you can pay on a per-user basis. That way, you can scale up or down to your exact requirement without the hassle of purchasing expensive hardware -- and software licenses.”

To make the offer even more attractive, Microsoft decided to throw in free credits on Azure, their IT Infrastructure-as-a-Service offering.

Put together, this was a combination most businesses couldn’t resist. Not just enterprise clients. Small businesses are more likely to feel the pinch of IT costs, not to mention hiring and staffing for IT. They came in droves, and Office 365 has since become the most popular SaaS application in the world.

Office 365 Takes to the Skies

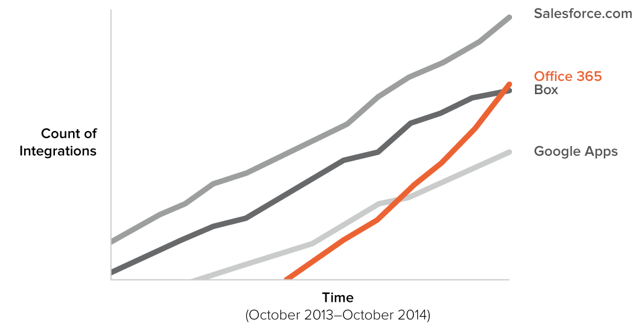

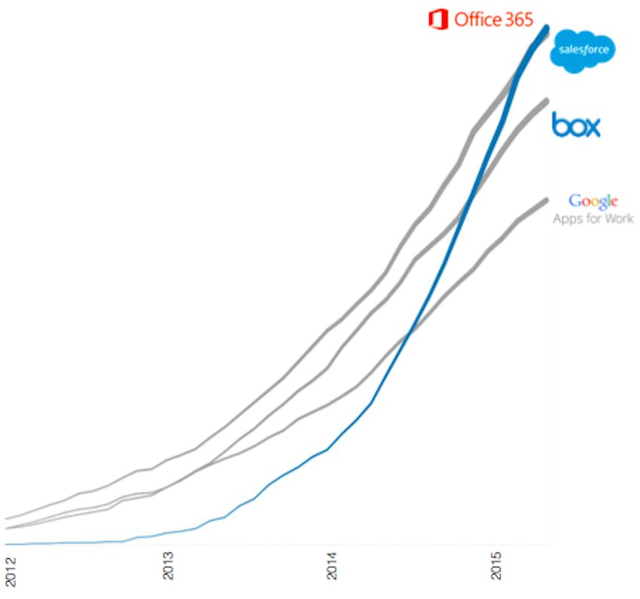

Neither company reveals the real numbers related to its office suite offerings, but I was able to dig up corroborative information from multiple sources, one of which is Okta.

According to Okta’s Microsoft Adoption Guide, usage has been on a steep climb since 2013. By the same time in 2014, Office 365 had already usurped second place, putting it well ahead of Google Apps and squarely in competition with salesforce.com to be the No. 1 SaaS application of all time.

That was in 2014. Over the next year and a half, Business Insider says Office 365 zoomed past salesforce.com and continues to grow at a rapid pace.

The question now is: How did they strategize their sales model to make this happen so quickly?

To be fair, they did have a lot of advantages. For one, business users were already very familiar with the MS Office family of software applications. Two, most of them were already using Skype, so Skype for Business was a natural transition -- and one that could be centrally controlled at the administrator level.

The third advantage is one that I think played the biggest role in top line growth: its pricing strategy.

How Critical Was Pricing in Office 365’s Success?

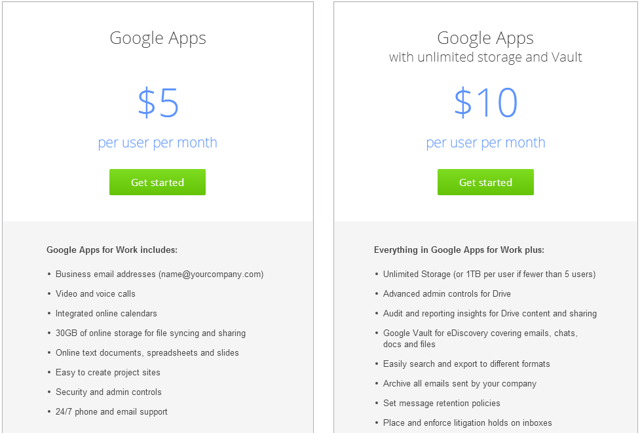

Not much analysis has been done around this as far as I’m aware, but pricing is exactly what tipped the scales in Microsoft’s favor. Here’s a look at how both services have been priced.

Source: Google

Source: Microsoft

When you first look at both deals, Google’s looks so much more attractive. You can get an email address, 30GB storage, online collaboration for all types of documents, voice and video calls and a host of other benefits even on a basic $5 plan. On the other hand, Microsoft Office 365’s entry-level plan is limited to email, storage, Skype and a toned-down online version of Office.

But the thing is, Microsoft is highly skilled at software pricing, something Google doesn’t have because its not in that space. What Microsoft did was price its various offerings and bundle the apps in such a way that the $12.50 subscription is the one most businesses would opt for. Did you notice that the strategically priced $8.25 subscription doesn’t include Skype?

As a decision-maker for an enterprise, the obvious choice would be the Premium subscription. It’s the only one that has the utilities that will make on-premises solutions redundant. This is the whole purpose of SaaS, after all. It’s a brilliant move by Microsoft, and that’s one of the key reasons Office 365 is still growing revenues at 63% in constant currency as of third quarter 2016.

Google took a different route and offered nearly everything on the basic plan. Therefore, despite grand plans last year to grab 80% of Microsoft Office’s business, Office 365 blindsided them and displaced Google in the SaaS space instead -- a major coup for Microsoft CEO Satya Nadella.

How Does the Above Reflect on Its Top Line?

Microsoft’s breakout numbers are notoriously hard to find, as most financial writers know. Using the clues they’ve given and extrapolating from past data, however, this is what I show:

There are currently 22.2 million consumer users of Office 365 as of quarter three.

That’s an increase of 7.7% over the 20.6 million figure reported for quarter two.

In quarter two, Nadella spoke of an active user base of about 60 million for Office 365 but did not give the numbers for quarter two. Take away the 20.6 million consumer users from that total, and you have roughly 39.4 million commercial users as of quarter two.

If we use the 7.7% figure to extrapolate for commercial users as of quarter three, that gives us a current level of approximately 42.5 million.

Now, using a consumer- to commercial-user base split of 20.6 million to 42.5 million, we can extrapolate earnings.

At the $5 and $8.25 price points, the Office 365 consumer base of 22.2 million can generate between $111 million and $183 million in monthly sales.

At the $12.50 premium price point, 42.5 million commercial users can generate approximately $531 million in monthly sales.

The Investment Angle

In the Productivity and Business Processes segment that these figures are reported under, third quarter revenue stood at $6.52 billion, for an annual run rate of approximately $26 billion.

As you can see, that will be a significant contribution towards overall revenues for fiscal year 2016, and this is where Office 365 will play a critical role in Microsoft’s top line growth over the next several quarters.

As Nadella rolls out his Windows 10 agenda backed by the open-source-embracing Xamarin/Universal Windows Platform ecosystem, Office 365 and overall cloud revenues, which already bring in 30% of the company’s revenue (as of quarter three), will continue to provide the floor support that the stock needs to maintain investor confidence.

To be brutally honest, this is a critical time for MSFT. The stock already took a disproportionate hit on quarter three earnings and cannot afford to continue taking such hits. Fortunately, however, these earnings shockers create an entry point for new investors in Microsoft and for existing investors to add to their positions.

Disclosure: I have no position in the stocks mentioned in this article, and no intention to open a position in the next 72 hours.