In what could be called a rare event, Costco (COST, Financial) posted flat comparable store sales for the first time in six years. Is that an exit signal for investors, or are there other forces at play? Let’s look at the real reasons for the comps situation and see whether it’s time to offload your Costco or load up while others fret.

The first thing we need to look at is how other retailers’ comps are faring right now. The growth of ecommerce has been putting the screws on all the brick-and-mortar stores, and Costco is no exception.

While most other retail chains actually posted positive growth in comps over the past two years, Costco is the only one that consistently declined in this area for four consecutive years. That implies that the rise of ecommerce is not affecting every company’s comps in the same way.

But is that the real reason behind sagging comps for Costco in the first place? The company is continually adding members and membership revenues have been consistently growing over the past several years. There’s no reason for that trend to change now. Besides, its annual membership renewal rates have consistently been around the 90% level.

Another metric that is incongruent with apparently poor comps performance is overall revenue. As you can see from its most recent earnings report, it delivered solid results for the period ended May 8.

In fact, both net sales and membership fees are clearly on the uptick so there’s no reason to assume that customers are spending any less this year compared to the same periods last year. The 12-week and 36-week numbers both bear this out with an overall revenue increase of 2.6% and 2.2%.

So what’s the real issue with comps?

When you look deeper into the earnings report, you’ll immediately see the problem:

Source: COSTCO

One thing is obvious: It’s not the absolute numbers that are the problem. Two specific areas are deflating comparable store sales revenues – depressed gas prices and a foreign currency headwind. Taken on a constant currency basis and discounting the effect of lower gas sales, Costco’s comps seem to be in line with what other brick-and-mortar retailers are reporting – in the range of 4% to 5%.

Now, both of these factors are pretty much outside of Costco’s control. What is within its control are membership acquisition rates, renewal rates (to a great extent) and how strong its sales are. As far as those metrics go Costco is on the right track.

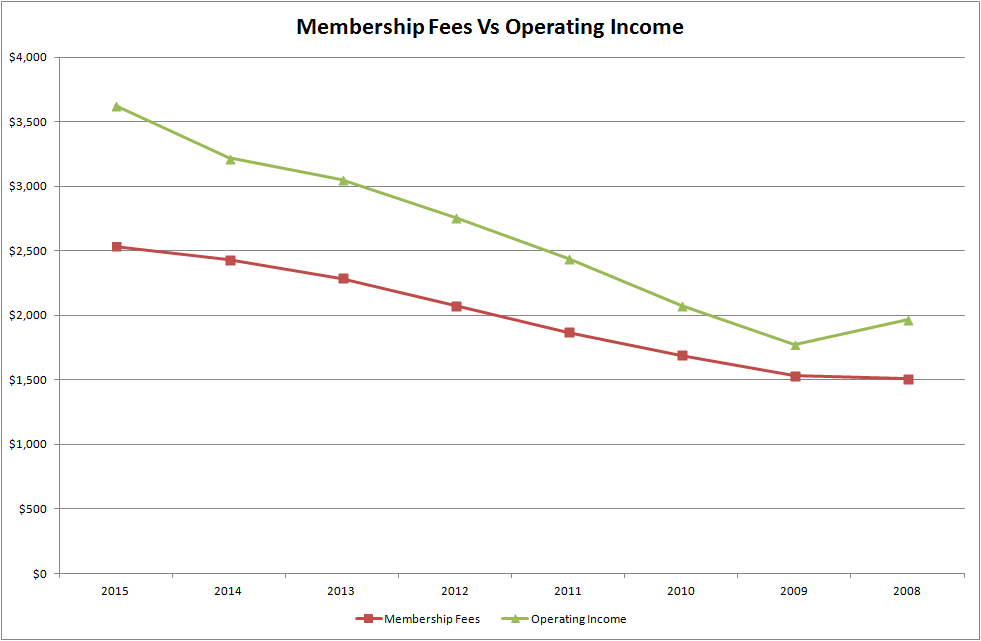

The loyalty factor

Source: Company Filings

For the most part, membership fees has been the bread and butter of Costco’s bottom line. In 2008, membership fees accounted for 76.48% of its operating income; now they account for 69.89% despite membership fees growing by a billion dollars during that period. That can only mean Costco is making more money than ever through its retail operations.

Nevertheless, the company’s wide loyalty moat is going to help it in the long run. The loyalty component has allowed Costco to remain head and shoulders above other brick-and-mortar operators despite ecommerce permeating the retail market in a big way. If there’s one company that can give Amazon (AMZN, Financial) and Walmart (WMT, Financial) a run for their money, it’s Costco Wholesale.

The investment angle: A great time to buy Costco

Growing revenues, solid membership growth, strong customer loyalty and continued store expansion across the globe mark the four pillars of Costco today. As such, it does make sense to put your money into the company even at such a high forward P/E ratio of 25.5.

For a stock that’s generally trending upward, a dollar-cost averaging method of investment often works well. Typically, you would invest fixed sums of money at equal intervals over a period of two to three years – or longer, if you prefer. Doing it this way will keep your cost basis down while gradually increasing your overall portfolio value as the stock continues to climb.

I’ve recommended the DCA approach with many companies across several industry verticals, and it ideally works with high-growth companies with long-term potential. From that viewpoint, COST is the perfect stock to invest in because of their continued expansion into the international market and a very strong and loyal user base in North America.

Thanks for reading my work! If you found value in this piece, please visit my profile page and follow me for more insightful analyses on the world’s top technology, retail and other consumer-facing companies.

Disclosure: I have no position in the stocks mentioned in this article, and no intention to open a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.