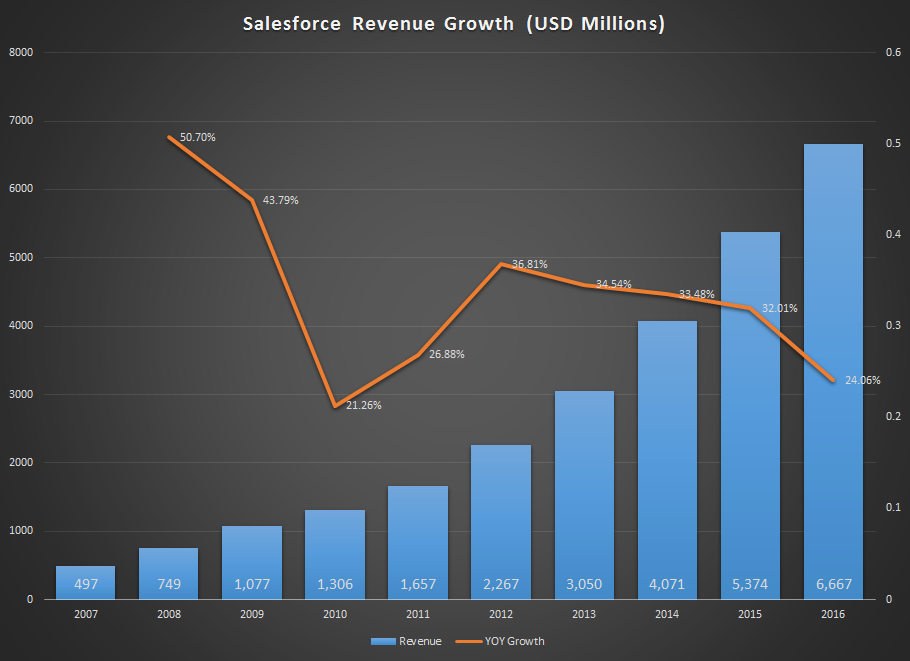

Not many companies can boast of doubling sales every two to three years, but Salesforce.com (CRM, Financial) is one of them. Growing at healthy double-digit rates since 2007, the company continues to grow unabated. In the first quarter of the current fiscal, it reported revenues of $1.92 billion – that’s a 27% year-over-year growth. If that isn’t enough, it's raised its already-high guidance for 2017 by $80 million.

CEO Marc Benioff, during Q1 Earnings call:

“With our strong start in the first quarter, we are raising our fiscal year 2017 revenue guidance to $8.16 billion to $8.2 billion. We’re also raising our fiscal year 2017 non-GAAP diluted EPS guidance to $1 to $1.02. We now expect year-over-year operating cash flow growth of 25% to 26%.

"For the second quarter, we’re expecting revenues of $2.005 billion to $2.015 billion. Non-GAAP diluted EPS of 24 cents to 25 cents, and our year-over-year deferred revenue growth of 26% to 28%.”

Profitability vs. growth

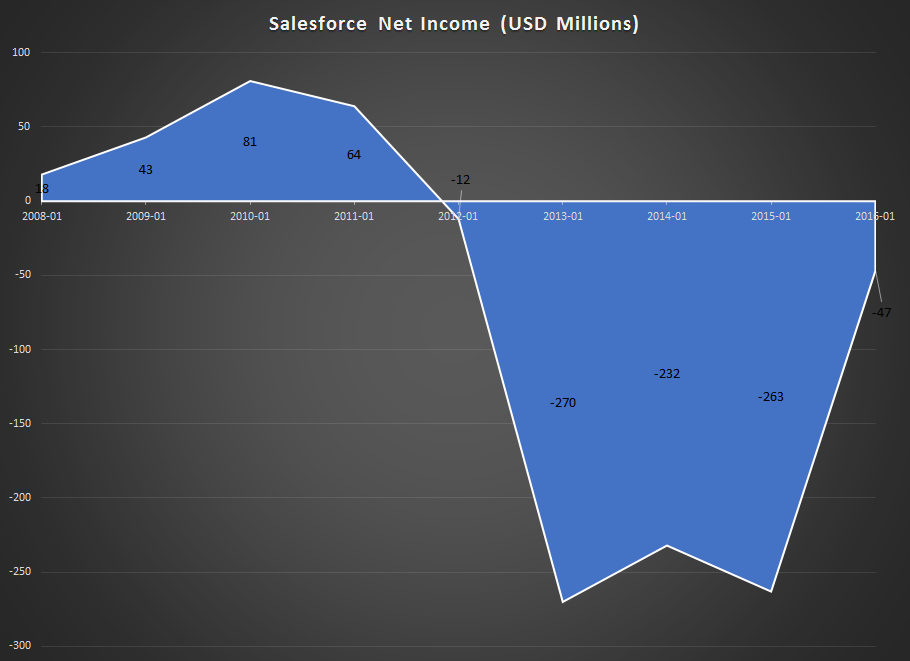

In the past, everyone wanted to know what the “bottom line” was for every company. In fact, that expression was used so much that it gradually made its way into casual conversation. Today, people don't care about a company’s bottom line as long as one other metric makes them happy – top line growth.

We’ve seen it over and over, with Amazon (AMZN, Financial), with Facebook (FB, Financial) during its early days and now with Salesforce.com. Despite being notoriously famous for not being profitable, the market is happy with Salesforce.com as long as it keeps that top line growth intact.

But that’s going to give rise to a plethora of problems, not least of all the fact that it's spending half its revenue on marketing and sales.

Of course, investors are being rewarded by growing share price, but the cost of customer acquisition is still too high for comfort. And now that Oracle has stepped up its game in the cloud industry (specifically with its Human Capital Management offering), it may not be smooth sailing for Salesforce.com as it moves into the next stage of growth.

Â

Source: Forbes

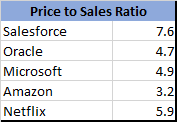

Considering the fact that Salesforce.com spends all the money it earns, it will be pointless to use earnings multiples to analyze the company's valuation. With nearly 7.6 times price to sales ratio, Salesforce.com will have to keep up its growth momentum in the face of increasing competition.

Agreed that it is in the right space. The cloud industry is growing, and it is the undisputed leader of the Salesforce.com market – the two things that will give it a huge growth runway. But it comes with a greater amount of risk now: to double your revenue when you’re at a billion dollars in sales isn’t the same as doing it when you’re at $10 billion. And that’s exactly where Salesforce.com is headed over the next two years.

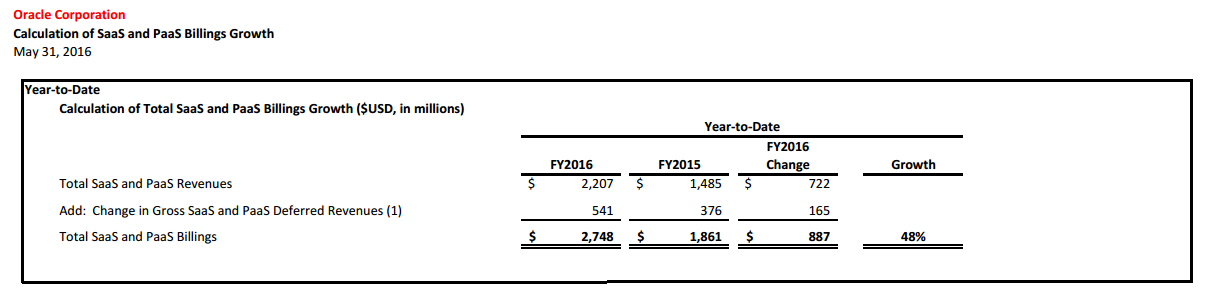

Salesforce.com has had the advantage of Cloud+Salesforce.com for a long time as Oracle (ORCL, Financial) fell asleep at the switch, doing its best not to wake up. But SaaS and PaaS revenues for Oracle grew by nearly 48% during the first quarter; and with other revenue prospects not looking too bright, this is the area that Oracle will have to hit hard. And that puts Salesforce.com right in the line of fire.

Salesforce.com CEO Marc Benioff, during Q1 Earnings call:

“We’re well positioned for another great year. This is amazing; I think that one of the reasons that we are doing so well is because Oracle and SAP are doing so poorly in the cloud. They just have not been able to make that transformation that we’ve made, that other companies have made, and we just continue to take market share from them and gain customers at a record level, and you can see that their growth numbers are nothing like we’re putting up here as we deliver our first quarter, and it’s happened because Salesforce is really the only company totally focused on companies helping to connect with their customers in a whole new way.”

While his words ring true right now, it may not stay that way for long. Oracle has been slow, for sure, but it's now at a point where it cannot afford to remain that way. It's still far away from Salesforce.com when it comes to cloud, but it's not slacking around doing nothing about it. A 48% growth is SaaS and PaaS revenues is not something Salesforce.com can afford to overlook.

There’s no doubt that Salesforce.com will do its utmost to stay in front of the competition and continue its market leadership position, but the issue at hand is that at a price of nearly eight times sales, there’s literally no room for cover for investors. And that's why it's a HOLD for me until it starts showing consistent growth without the sky-high expenditure.

Disclosure:Â I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.