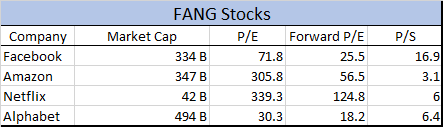

Facebook (FB, Financial) and its FANG counterparts trade at a premium compared to most companies. All of them are valued with high forward price-earnings multiples, and all are billion-dollar companies that are disrupting the world in their own way. But if you take a closer look at the numbers, it is clear that Facebook stands out in terms of price-sales. Trading at nearly 17 times sales, which is nearly two and a half times more than that of Netflix (NFLX) and Alphabet (GOOGL, Financial) and more than five times that of Amazon (AMZN), this is one company that deserves a closer look.

The question is: How can a company that recorded a net revenue of $5.3 billion during the latest quarter and a mere $17.92 billion for the last fiscal year be worth more than $330 billion? Revenues are indeed growing, but does that make the company worth nearly 17 times sales —Â or is this a classic case of over-hyped valuation or market expectation?

A look at Facebook’s user base

When it comes to growth for such a company, the first thing to look at is user base because it is one of the touch points where revenue is generated.

Facebook cannot keep growing its user base forever, and that metric is slowly arriving at saner levels as it penetrates the world further and further.

Logically, Facebook’s user base growth should mirror world population changes as it approaches peak penetration. It may not happen within the next few years as it still has several more countries to cover, but it is a reality that the company will have to face down the road.

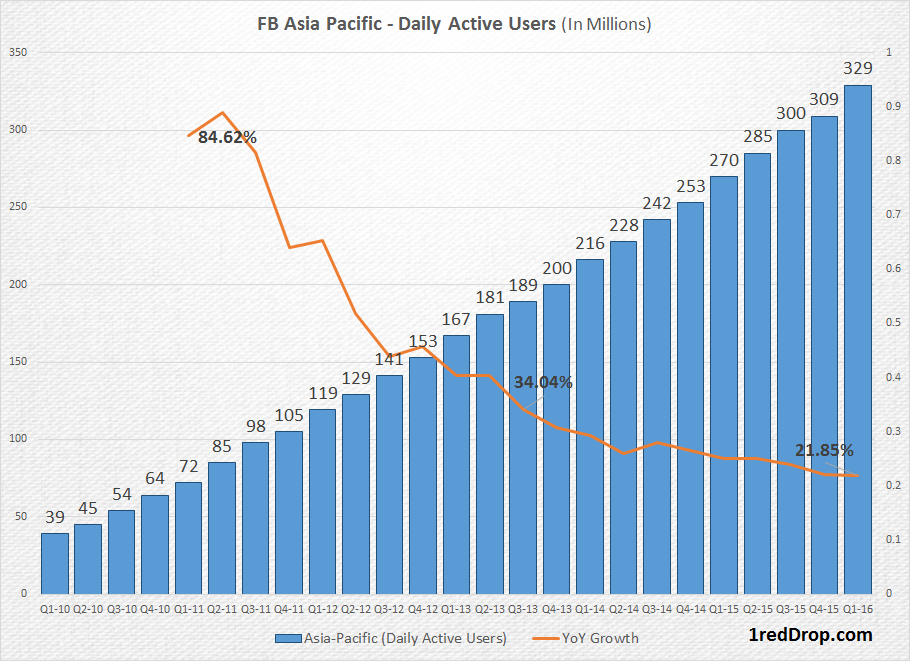

Daily active users (DAU) around the world is a segment that actually generates the bulk of Facebook’s revenues — simply because they are the ones that actively use the site or app on a daily basis.

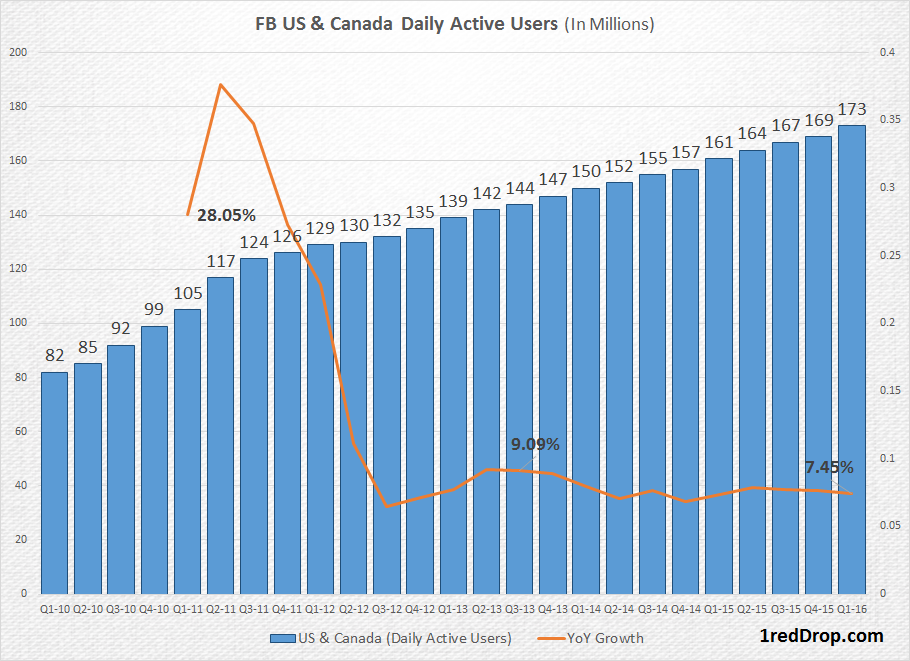

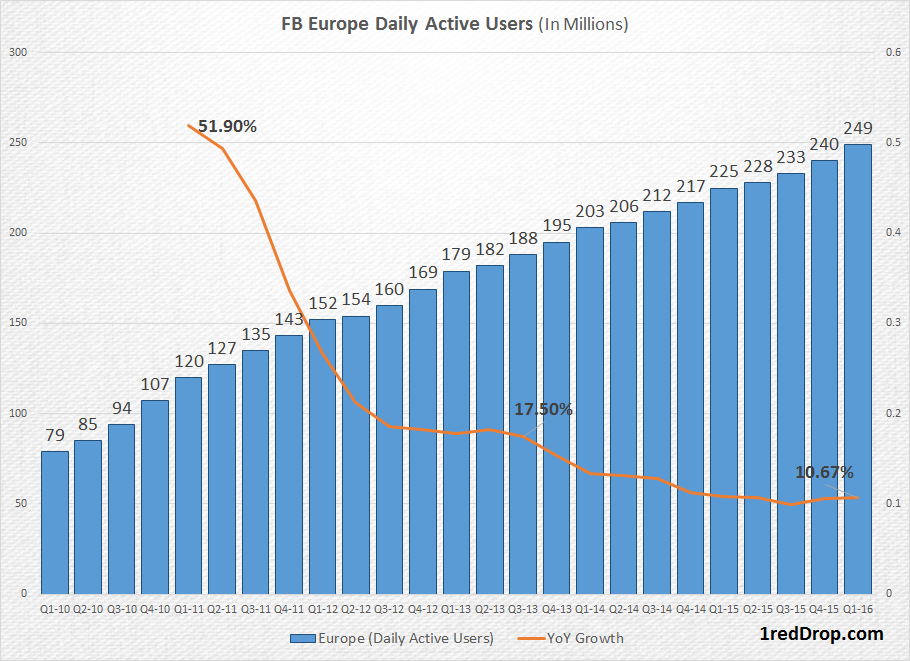

As you can see from the charts above, user base growth in developed countries is near high single digits, while APAC is still growing at double-digit rates. That is understandable because internet usage penetration is very high in developed countries and still growing at a fast pace in emerging markets.

Nevertheless, all the segments have come down from the high double-digit rate of user growth that Facebook enjoyed during the 2009-20011 period. If this is the case, why is Facebook trading at near 17 times sales, far higher than the other FANG stocks?

The monetization aspect

The key to that answer lies within the company’s main platforms. At this point, Facebook has three primary user base groups that can generate money:

Facebook

Instagram

WhatsApp

Oculus VR, its virtual reality product, is only just taking off, so there are three most promising growth drivers. There are others as well but not of significant enough future value to be considered in this argument.

The primary Facebook platform is where all the advertising money comes from. As such, it is currently the biggest breadwinner for the Facebook family of social applications.

Instagram recently joined the workforce and has started earning, ably helped by the network of advertisers that Facebook already has on board. Instagram still has a long way to go, however, before reaching proper monetization levels.

WhatsApp, the most popular messenger app in the world with more than billion users, is yet to be monetized at all. Though there are talks of business accounts and special access, nobody really knows how this will pan out. For now, it is unclear whether the company has a clear forward plan on how best to monetize this massive group of users. Facebook is very aware of the branding sensitivity for the app itself, and it is likely to be the decisive factor in what it intend to do.

What we have now is one fully monetized platform, one that has just started its journey and one that is not yet out of the gate. And that is where the high expectations are coming from. It is known that Facebook has the second highest number of advertisers on its platform, and it is a very close second to Google. Estimates put Google’s advertiser base at slightly under 5 million, while Facebook announced last year that it had already crossed the 3 million mark.

The point to note here is that the entire pool of advertisers around the world is a finite number, give or take. If Facebook is growing its advertiser pool, it necessarily means that Google is missing out, and vice versa. When you look at it from an advertiser’s point of view, Facebook’s platform makes more sense because it is not just a single user base —Â it is Facebook, it is Instagram and possibly even WhatsApp a few months down the road. You can see why advertising on Facebook would be a more attractive option for a typical advertiser.

The video play

One major point no one can ignore is Facebook’s aggressive push into video. Right now, the bulk of video advertisers are with Google or, more specifically, with YouTube. But Zuckerberg’s keen eye sees video as the future of Facebook, and Facebook has already started experimenting with various video initiatives, such as Facebook Live, video commenting and so on. At scale, these will soon form a massive body of user-generated video content that is immensely shareable but more significantly, it will also be highly monetizable.

The moment Facebook enters into video advertising in a big way it could spell trouble for companies like Alphabet.

As far as Facebook is concerned, that is another huge top-line initiative just waiting at the starting line —Â as is WhatsApp.

The investment angle

Essentially, Facebook’s high valuation is based on the potential upside brought by multiple user bases across at least three social applications, a video initiative that could take off in a big way and the fact that advertisers are joining its fold by the droves.

Even with those upsides, however, the valuation does seem to be a bit steep. Factor in all the variables, future acquisitions and new projects that may be launched, and it seems more than partially justified.

In any case, shorting Facebook now would probably be the biggest investment mistake you could make, but indiscriminate buying could be equally disastrous.

This is a great company at a not-so-great price, so it looks like a good buy keep adding to on the dips. You can also take the dollar-cost averaging route to keep your cost basis down — do this over the next two-three years and you could be sitting on a very handsome asset at the end of the period.

Disclosure: I/we have no positions in any stocks mentioned and no plans to initiate any positions within the next 72 hours.