Home Depot (NYSE: HD)Â and Lowe’s (NYSE: LOW) are two companies that are sitting on top of the home improvement world. Together, these companies netted annual combined revenues of $147 billion last year and command a market capitalization of $240 billion. More importantly, these companies control the home improvement market in the U.S., creating a duopoly that will stay in control for a long time.

Let’s take a look at various aspects of these businesses to see how strong and resilient they really are.

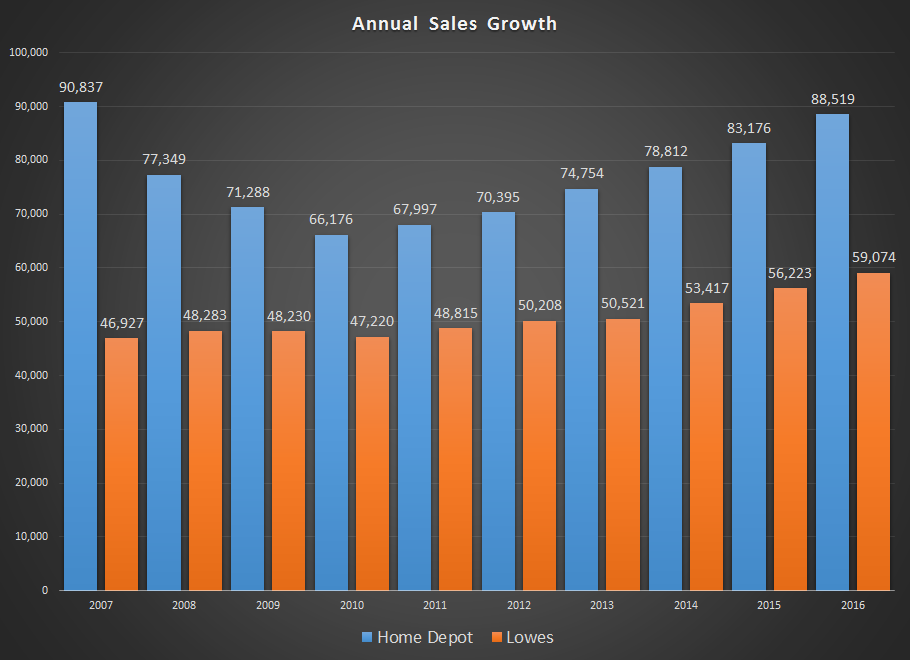

Revenue growth

The much younger Home Depot has taken the lead in terms of sales with 2016 annual revenues reaching $88.52 billion, growing in the above 5% range for the last four years. Lowe’s 2016 annual sales touched $59 billion in 2016, with sales growing in the above 5% range for the last three years.

Both the companies were hit hard during the Great Recession but have recovered nicely since then. Despite being in the home improvement business in the midst of the worst-ever housing market collapse, both companies remained profitable right through the recession, underscoring the resilience of the industry.

I agree that they won't be immune to the ups and downs of the economic cycle, but the way they got out of the recession clearly shows that this is an industry that can live long after we are gone.

The industry moat

At the end of 2015, Home Depot had 2,274 stores and Lowe's had 1,857 stores around the world, with product listings running into the tens of thousands. This is a niche segment targeting do-it-yourself and professional contractors.

Though they may not be totally immune to competition from e-commerce growth, it will be tough for pure-play online companies to compete with these companies and come out on top.

The breadth and depth of the product line will be very hard to replicate and, as long as that is not achieved, there is no easy way to compete with them. Their footprint is already huge, so for any brick and mortar company to seriously compete with them will take many years of struggle - and they still won’t be able to reach the size and scale of these home improvement giants.

Margins, cash flow and Capex

On the operating margin front, both these companies have swapped positions since the recession, with Home Depot steadily moving in the double-digit range and Lowe’s trailing with high single digits.

Here’s what analyst Carter Harrison at Conlumino, a retail research firm, says:

"One of the challenges for Lowe's is that while it is a significant player in the market, it all too often plays second fiddle to Home Depot — which remains more of a 'go-to' destination, especially for home improvement shoppers.

"Lowe's is positioning itself well as a customer-centric player for the non-expert: a potentially weak spot for its larger rival. In our view, this positioning is well thought through and gives Lowe's an opportunity to differentiate as well as steal share from non-home improvement players in areas such as kitchens and bathrooms."

- CNBC

So, although Lowe’s is definitely showing improvement, it is still way behind the curve when compared to Home Depot, and that catchup is costing them on the margin front as well. It’s going to take some more time; but, if Lowe’s can keep up with HD’s growth rate while optimizing their strategy to target the amateur market, then I do see the gap between their margins closing.

As you can see above, both companies are maintaining the pace with respect to capital expenditures and there is not much to differentiate here. It’s understandable, as neither wants to give the other a chance to spend more and thereby grow faster.

From a dividend perspective, rising free cash flows and payout ratios of less than 50% gives a lot of runway for both companies to keep their dividend growth intact as they move into the next decade.

Balance sheet health

At the end of the most recent quarter, Home Depot had $3.257 billion cash on hand with $20.904 billion long term debt, while Lowe’s had $4.561 billion cash on hand and a long term debt of $14.322 billion. With operating income staying north of $10 billion for Home Depot and $4.5 billion for Lowe’s, both companies have enough strength in their respective balance sheets to keep the dividends flowing and growing for the next five to 10 years at least, and most likely well beyond that.

Note to investors

Considering the size of the companies, their hold on the market and a niche well-capable of keeping online players at bay, this two-horse race should make ideal guests for your dividend portfolio for a really long time.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.Â

Also check out: (Free Trial)