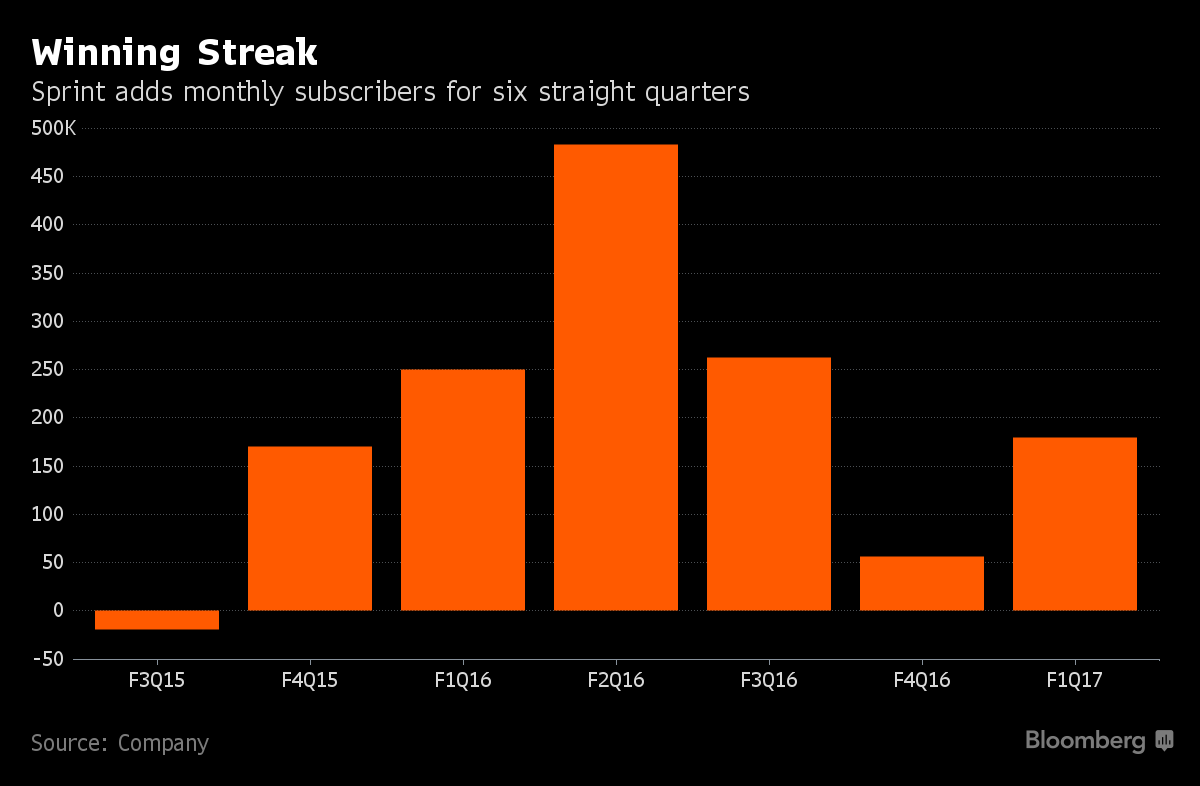

Sprint’s (S, Financial) stock skyrocketed to above $6 after the company posted better-than-expected results and recorded its fourth straight quarter of growth in its postpaid phone base. It took almost two years for Sprint to get above the $6 level so this is indeed good news for its investors.

I have been skeptical about Sprint’s fortunes, as the U.S. market is approaching peak penetration in smartphone growth; and I covered that in detail in my article "Sprint Running Out of Steam as Market Nears Peak Penetration."

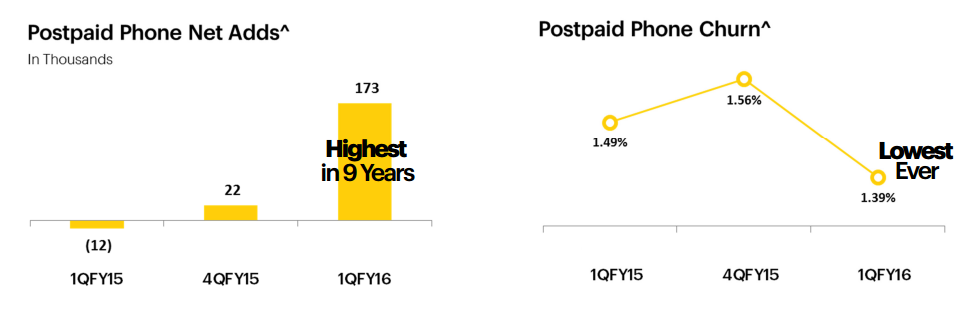

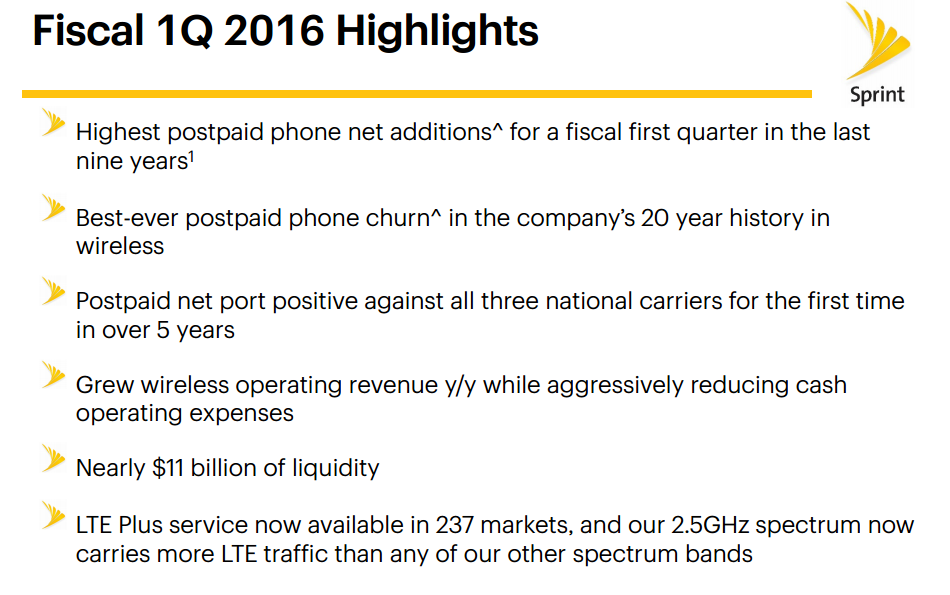

The No. 4 wireless carrier in the U.S. beat estimates by a small margin in the second quarter, adding 173,000 postpaid wireless customers during the quarter – the highest it's recorded in the last nine years – and 180,000 monthly subscribers, which was way above the 112,000 consensus estimate reported by Bloomberg.

The first-quarter result

Sprint reported revenues of $8.01 billion and a loss of $8 per share while analysts’ consensus expectation was $7.99 billion and a loss of $8 per share. Net loss widened to $302 million, up from $20 million a year ago, as the company stepped up its game to garner subscribers by offering plenty of discounts and perks. The company was also able to do a better job in holding its own customers, and postpaid churn – the rate at which subscribers leave for other networks – was reported at 1.39%, the lowest level in Sprint’s history in the wireless segment.

Why celebrate an insignificant consensus beat?

The jump in stock price looks disproportionate to the actual gains made by the company so why were investors so pleased with the results?

A major reason is the company expects to meet its former guidance given for the full fiscal.

No upward guidance revision usually makes for a lukewarm reception at the hands of investors, but in Sprint’s case, the story has been a downhill one for so long that even meeting expectations is taken with more than a pinch of optimism. Sprint performed well during the first quarter, no doubt, and that has given investors the confidence that Sprint will be able to make its growth strategy work for the entire fiscal.

The $9.5 billion to $10 billion adjusted EBITDA estimate for fiscal 2016 remains intact as does the $1 billion to $1.5 billion range for operating income. The cost-saving measures undertaken by the company have borne fruit, and the sustainability of those measures will decide how Sprint finishes out this fiscal.

Possibly the tipping point for the stock rally was that the company expects this year to be break-even on cash flow but expects to close next year on a cash flow positive note.

Which challenges remain?

The ride is far from over for Sprint. It's grown its postpaid subscribers at an admirable pace, it's seen record performance in the same segment, and it's improved its margins tremendously year over year. But now it’s going to be a fine balancing act between cost cuts and net adds.

It's already sacrificed margins for growth, and if not for the cost-control measures, it would only have net adds without the added benefit of expanded margins. It’s that delicate balance that’s vindicated Sprint in the eyes of investors. But now, it will have an even thinner tightrope to walk over the next three quarters. Unless it can continue to show margin expansion along with subscriber additions, its stock may well slide back to its old levels.

In summary, it's had a great quarter and set the tone for a very positive quarter – at least, as far as investors are concerned. If it can maintain that momentum on multiple fronts like it did over the past few months, even its break-even cash flow is going to look like a major achievement come fourth quarter.

Sprint now has a simple formula to follow: keep them coming in and stop the money from flowing out. If they can master that during the next three quarters, it’s going to create a significant upside for the company.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.