Qualcomm’s (QCOM, Financial) shares surged after the company reported better-than-expected third quarter results. Earnings per share came in at $1.16 on the back of $6.04 billion in revenues while analysts were expecting 97 cents EPS with a revenue estimate of $5.58 million.

The strong results can be directly attributed to the progress Qualcomm has made in China and the chipmaker shipping 16 million more chips than it guided.

"The key piece is the underlying technology migration to LTE, which has been the engine that is really driving the importance of getting China in a good spot for us as a business,"Â CEO Steve Mollenkopf told CNBC. "China will continue to be an important component of the growth story for Qualcomm moving forward."

Investor sentiment about the company was mixed as the processor company had to cut 15% of its workforce last year due to the slowdown in smartphone sales, and the stock price kept edging lower and lower through 2015 before starting to move up again in February; and with third quarter results and forecasts looking upbeat, it may well continue the recovery.

Advanced Micro Devices (AMD, Financial), which has been promising to get its business and profitability back on track, also had a good quarter as the company reported a non-GAAP loss of 5 cents while analysts were expecting a loss of 8 cents per share. The company also reiterated its guidance for the rest of year, making it clear that it does not see any potholes on its way. Advanced Micro Devices' future performance will be extremely reliant on the success of Polaris and Zen franchises, and I have covered the challenges the company might face in its long road to success in my recent article “Polaris Can’t Save AMD.”

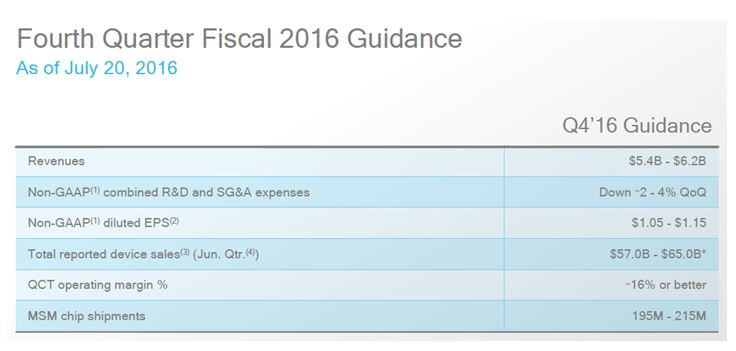

Qualcomm, on the other hand, has always been profitable. After seeing its revenue slide during fiscal 2015, Qualcomm’s revenue growth seems to be on track; however, much will depend on how the company does in China, and the health of the smartphone market around the world. Though the current guidance might indicate that flat or zero growth for the fourth quarter compared to last year is a possibility, in reality the company is possibly expecting to reach the top end of its guidance or maybe even more. Qualcomm reported $5.456 billion revenues in fourth quarter 2015 and is guiding for $5.4 billion to $6.2 billion for the fourth quarter.

“In terms of the upside to guidance as we indicated our Q4 guidance is really set at the low end of the full year range for QTL. So the upside would be the agreements in addition to the ones that we expect to sign that we put into the guidance. There is still $400 million of revenue upside that is possible for the quarter and not in our guidance.” – George Davis, CFO Qualcomm, Q3 Earnings Call

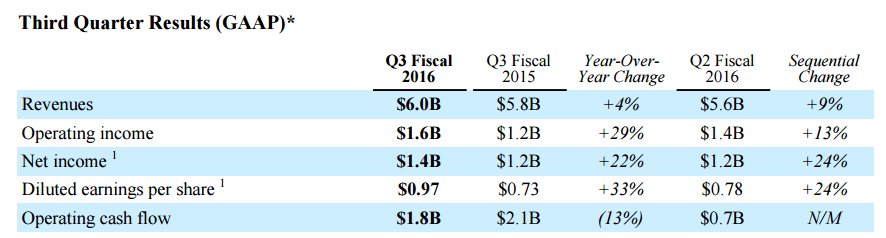

Thanks to the rude shock the company received in 2015 – where it saw its revenues slide after seeing it grow nearly 3.5 times since 2006 – Qualcomm has stepped up its efforts to improve operational efficiency and save some money, a move that has already started to pay off. During the third quarter, revenue was up by only 4% but operating income was up by a whopping 29%.

Note to investors

Between the two chipmakers, Qualcomm is obviously in better shape than Advanced Micro Devices. Although the former does depend heavily on the smartphone market in China for growth, its top line seems in much better shape than it was a year ago. Advanced Micro Devices, on the other hand, is walking a much thinner tightrope.

From my earlier article on Advanced Micro Devices:

“By no means is the new product line going to get them out of the woods. The company has been losing money for the last four years and revenue has been stagnant for the last 10 years.”

From an investment perspective, Advanced Micro Devices is a HOLD while Qualcomm is much easier to recommend as a BUY because of the upside supporting its guidance.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.