Jeffrey Ubben of ValueAct Capital recently took a large billion dollar stake in Morgan Stanley (MS, Financial) representing about 2% of outstanding shares. According to the WSJ, the incredibly successful activist endorses the current CEO and the strategic trajectory the organization is on. Although Morgan Stanley is generally perceived to be a large bank, its asset management activities are much more important than most people think. This appears to lay at the center of the ValueAct thesis, but it is not a new idea. Back in March of this year, Charlie Bobrinksoy went on CNBC with that idea, which we discussed here on Gurufocus.

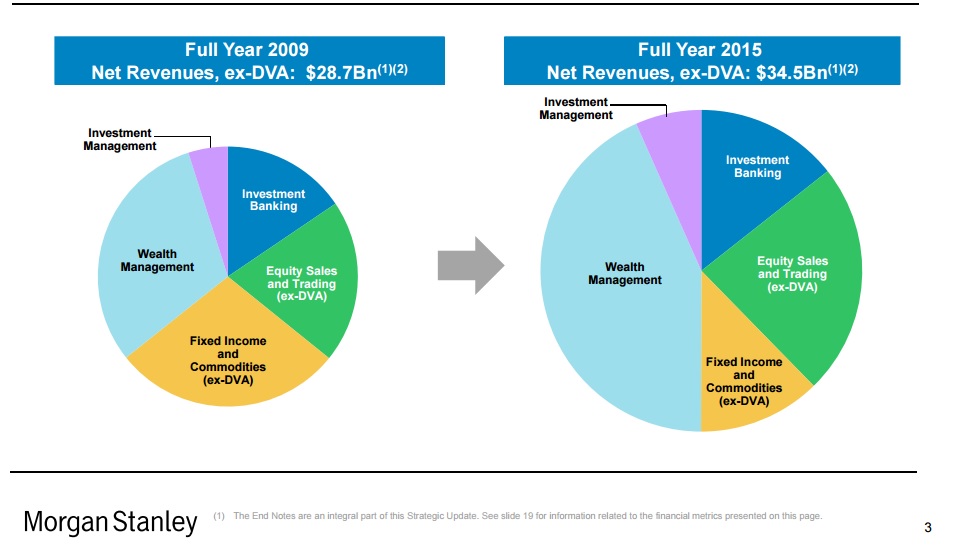

The transition from bank to wealth management is aptly illustrated in this slide taken from a company presentation:

It is immediately apparent wealth management and investment management made up about 33% of revenue in 2009, but take up 50% of revenue in 2015. Revenue did grow over this time frame which means the growth rates have been particularly strong for these segments, especially investment management.

Wealth management firms are kind of out of hated at this time, but the business model is sound. Collect a nice fee on assets under management and depending on the type of investment management offered (alternatives for example) a performance fee. Its an incredible asset light business and if you can gather AUM at reasonable cost or have particularly sticky clients, it is a terrific business.

According to a ValueAct letter to investors, which I have not been able to locate so far but is cited by Bloomberg and other sources, the firm likes how Morgan Stanley shifted towards asset-light, fee-based businesses like the wealth and investment management, but also the investment bank advisory business. These segments account for 80% of profits, up from 30% pre-crisis according to ValueAct, a shift that we also saw reflected in the revenue. Finally, ValueAct liked Morgan Stanley’s moves to make less risky loans and recapitalize its balance sheet.

The stock is owned by a lot of gurus in addition to ValueAct and it still looks attractive at 0.85x book value, its $2 trillion of assets under management make it look very, very cheap at a market cap of just ~$60 billion. Although it should be said that only $820 billion of client assets are managed in fee based accounts, which is a more readily comparable number to use. Still that puts MS at a value of around 0.5% of AUM and that is still very cheap. Of course, management sees further upside (when don’t they), but for growth to materialize they don’t need to move heaven and earth. Just stick to what has been working for them recently:

Disclosure: I have no position.

Start a free 7-day trial of Premium Membership to GuruFocus.