Acquisitions are a major part of a company's history and evolution. They allow the company to quickly get into business lines to which they never had access. They help keep revenue flowing in, and, without acquisitions, some segments wouldn’t even have large companies, like pharma, for instance.

In many cases acquisitions are replacements for organic growth, but in Salesforce’s (CRM, Financial) case the speed of acquisitions has been so fast and furious it’s hard to believe this is a company that’s already been growing revenue at double-digit rates for the past several years.

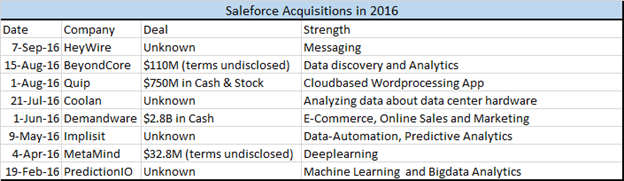

Over the past eight months the company has made eight acquisitions totaling more than $4 billion, and it’s only September. The company isn’t even sitting on such a huge cash pile that can justify the number of acquisitions. At the end of January this year the company had $1.158 billion cash on hand and, to boot, Salesforce has not been profitable since 2012.

During the second quarter of the current fiscal Salesforce’s revenue jumped by 25%, not an unusual number considering the company’s track record. The question here is, why would you want to go on an acquisition spree when you have always found a way to re-invest in your operations and keep expanding at a breakneck pace?

"But Salesforce CEO Marc Benioff doesn't seem concerned about the pace of acquisitions, saying the M&A market just opened up this year with companies becoming available at reasonable prices. During the company's earnings call, Benioff hinted it will likely continue to scoop up companies for the rest of the year."Â –Â Business Insider

Salesforce’s acquisition of Demandware for $2.8 billion this June was the largest the company has ever made, even more than its previous record of $2.5 billion for ExactTarget three years before that. Salesforce paid a 56% premium for Demandware because it wanted to offer ecommerce solutions to its customers. So much for reasonable prices!

Although Benioff clearly talks about reasonable prices, it seems he’s using it as a relative term. Why else would Salesforce have been in the race to buy LinkedIn (LNKD, Financial), which Microsoft (MSFT, Financial) swooped in to acquire for $26 billion – more than half of Salesforce’s current market capitalization of $50 billion?

That the company was seriously thinking of buying LinkedIn clearly shows that the dynamics of the landscape in which Salesforce has been operating has changed.

As for successful acquisitions this year, it is clear that Salesforce is pushing deeper into the artificial intelligence and data analytics side of the business, which will enhance its current product line. It is also branching out into ecommerce software, a new business vertical for the company.

From a competition perspective Microsoft and Oracle (ORCL, Financial) are both bringing a lot more heat to Salesforce’s front door. Though there is no head-on collision as yet, Microsoft is clearly focusing on the enterprise segment. By building software that can be served in the office environment and augmenting the growth of its cloud business, the company is bound to start beefing up its business management software as well, hitting Salesforce in the process. Oracle, on the other hand, has made it abundantly clear that Software-as-a-Service is its core area of focus, and the company is now targeting $10 billion in revenues from its SaaS and PaaS segments.

These threats may be in the future, but Salesforce is clearly choosing not to wait before dealing with the problem.

Disclosure: I have no positions in any of the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.