Of the top five retailers in the U.S. I have always liked Costco (COST, Financial) for several reasons.

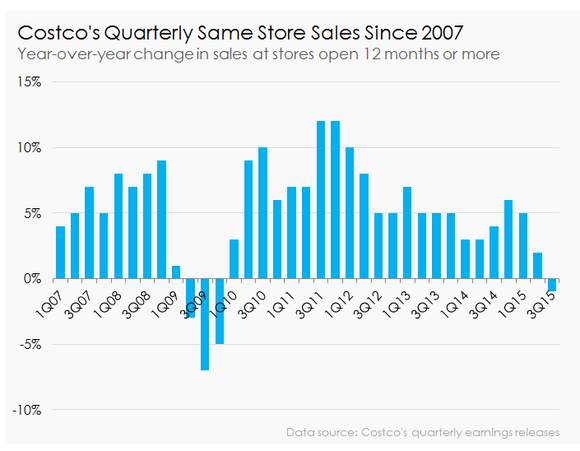

The more than 40 million-strong paid user base that keeps renewing its membership year after year is a huge validation for the company’s business model. Not only has it kept Sam's Club from getting close, it has also effectively thwarted the online onslaught despite Costco itself not having a fully functional ecommerce division. But after many years of strong comparable store sales growth, Costco’s store sales this year have been weak.

A case of duplicitous comps

Comparable store sales for the last year and half have been flat – a shocker for many Costco investors – and the stock is down nearly 7% since the start of the year. Though its numbers are much better than some of the other retailers such as Target (TGT, Financial), now is definitely not the time to show weakness when the brick-and-mortar retail industry is showing symptoms of Amazonitis (a condition wherein sales erosion for physical retailers can be directly attributed to competition from online retailers.)

Costco was one of a few companies that enjoyed double-digit store sales growth after 2010, a key period when Amazon (AMZN, Financial) moved from $34.2 billion in annual sales to above $100 billion. But after showing remarkable consistency during the 2010-2014 period, Costco’s comparable store sales severely weakened during the last four quarters and the company reported flat growth for the year.

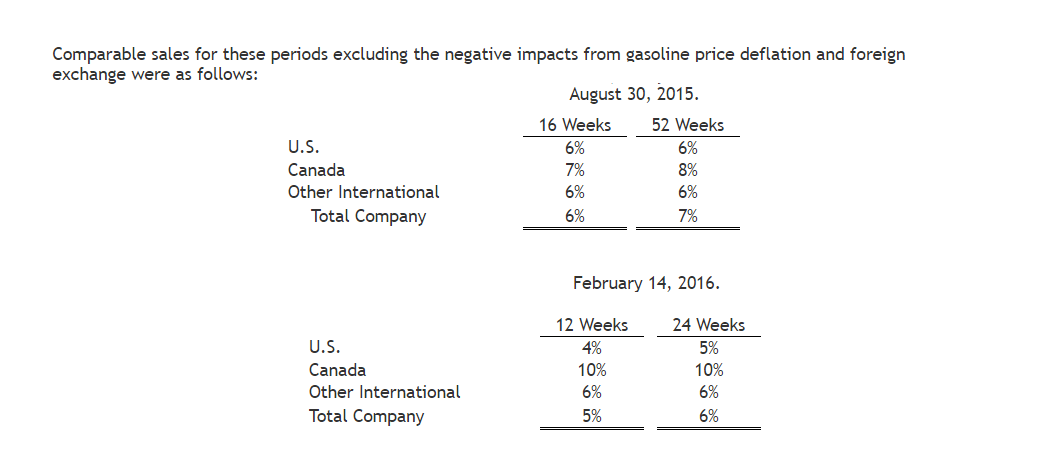

Two key factors that put enormous pressure on Costco in 2014 were the stronger dollar and the oil price crash. Though oil prices have somewhat recovered since, it is still a long way from the highs it touched before falling. Once you remove the effects of foreign exchange and gasoline sales Costco’s comparable store sales for fiscal 2015 reach 7%, and for the first six months of the current fiscal comps stand at a healthy 6%.

If two things brought its comps down, then two others took their place as compensators – foot traffic and new store additions. As reported by Motley Fool, Costco’s foot traffic went up 3.25% the same month that same-store sales declined, and the growth that accompanied new store openings actually gave Costco marginal year-over-year growth.

Should Costco be worried?

Several factors now contribute to making Costco look weaker than it actually is. On the other side of the world China is crashing toward a more reasonable growth rate than the five-year high it has been on, and in Europe there is uncertainty with only certain parts showing growth; as a result, the dollar will inevitably remain strong in the short to medium term, making Costco’s numbers look bad.

As long as the status quo doesn’t change Costco will continue to have its actual growth marred by these headwinds quarter over quarter.

On the positive side the fact that we’ve seen gains in store additions and foot traffic is an indication that the brand remains strong. And with only 494 warehouses in the U.S. and 706 globally, there is obviously ample room to expand the brand’s presence and, with it, top line growth.

The pattern of current comps is merely a prolonged blip that presents investors with a great opportunity to build their positions in Costco so go through the numbers carefully and see if they add up for you.

Disclosure: I have no positions in any of the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.