Intel, one of the world’s largest and most well-known chip makers, is going through a huge transition pace as the company tries to balance out its declining PC-based revenue streams with new ones. Intel’s revenue growth has been flat since 2011 as the slowdown in PC sales impacted their top line sales. The company has been slowly limping back into growth territory, but with more than 50% of their income coming out of PC-based business lines, Intel itself remains cautious about its short to medium term prospects.

Revenue growth and moat

From a dividend investor’s perspective the moat is an extremely important criteria. You want to buy and keep companies that have strong moats, which will allow them outlive you. Intel is still a dominant player in the PC segment, but the problem is that PC sales has been declining over the years as the world moves to smaller, mobile and more powerful devices. I don't think PC sales will plummet to zero, but it may never again be in a position to keep posting stable growth. Stable is still possible, but stable growth is going to be highly improbable in the long run.

To offset their dependence on PC-based revenues, Intel is ramping up its efforts in Internet of Things, Data Center and Artificial Intelligence. They are still lagging behind NVIDIA on the Data Center and AI front, but both are growth industries and the segment itself is looking for competition so innovation to thrive. There is still time, as these are nascent industries in the process of early adoption. It is the ideal direction for Intel to take, but returns are going to be a bit slow.

With their main revenue driver - the Client Computing Group, which is dependent on PC sales - looking at a not-so-rosy future, and future revenue drivers such as IoT and Data Center still too small to be an offset, in the medium to short term Intel can deliver top line stability at best.

Cash flow position

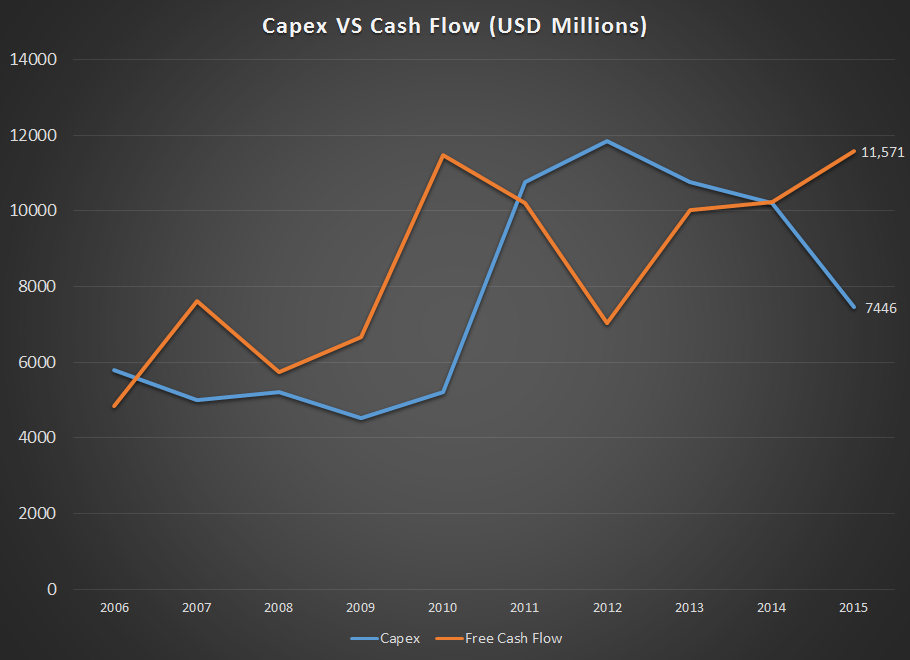

The chip-making business is research intensive. You have to continuously innovate to stay on top of the industry because your competitor is not going to stop. As such, it requires significant amounts of continuous capital expenditure as well as R&D. In the last five years Intel has spend nearly $50 billion dollars in Capex, while free cash flow has been holding steady around the $10 billion dollars a year level.

Intel’s payout ratio has been well below the 50% level, which will allow the company to keep its dividends flowing to its investors. The company has also been steadily buying back shares from the market, reducing their total outstanding shares from 5,936 million in 2007 to 4,894 in 2015. Intel paid $4.5 billion in dividends, while buying back shares for $3.4 billion in 2015. With an annual operating cash flow of nearly $20 billion, Intel’s cash flow is strong enough to support its dividends in the medium term.

Balance sheet

At the end of second quarter Intel had $8.1 billion in cash and short term investments with a long term debt of $24.053 billion and another $3.5 billion in other long term liabilities. The balance sheet position is healthy enough for the company to keep up its dividends.

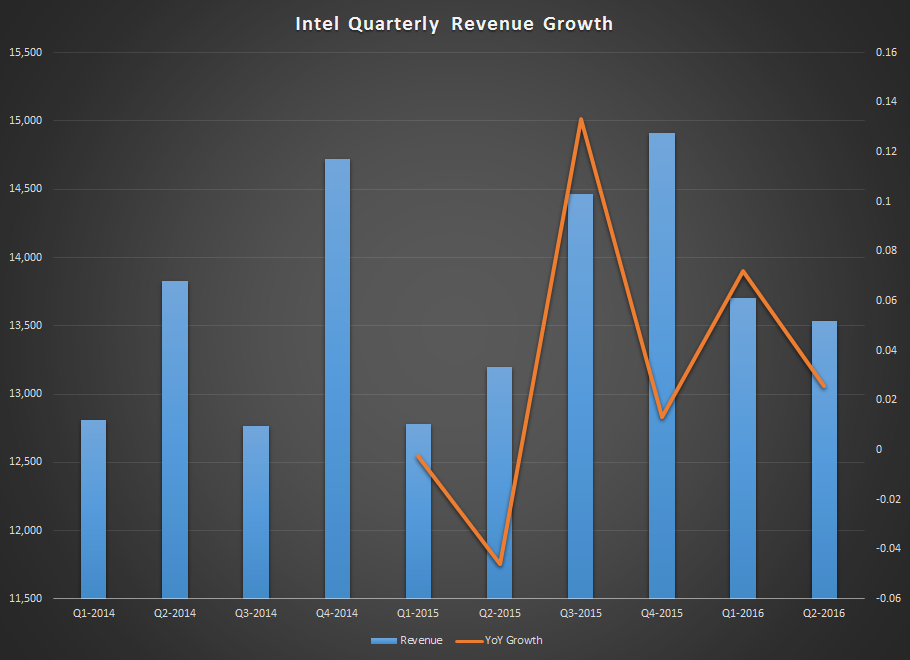

From a cash flow perspective and balance sheet point of view, Intel is indeed strong enough, and their 2.74% yield looks attractive. The biggest area of concern would be around how long the company will need to start posting consistent growth. It has done well so far this year with revenues growing from $25.97 billion in the first half of last year to the current $27.23 billion, and their guidance for the year is for mid-single digit growth.

Things are looking good for the fiscal, although it will be at least another two more years before we see the results from new revenue lines starting to impact the top line in a big way. There is a risk of slowdown in the medium term, and that's the reason why Intel’s yield is hovering around the 2.7% mark. Intel’s PC business will hold its ground, but the company has to urgently accelerate its new lines of business. Until that happens the risk profile of the company is indeed high.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

About the Author

Sangara Narayanan holds an MBA from Kent State University, Ohio, and has worked on the floor as a trader in New York. You know where. He is passionate about capital markets and specializes in business analysis, stock valuations and making chicken curry.

Â