Gilead’s (GILD, Financial) stock price has been on a never-ending slide since the second half of last year. The stock is now trading at less than 7 times earnings after dropping more than a quarter of its valuation in the last twelve months. But a key question that remains after analyzing Gilead is why the company is sitting on its cash pile without doing anything.

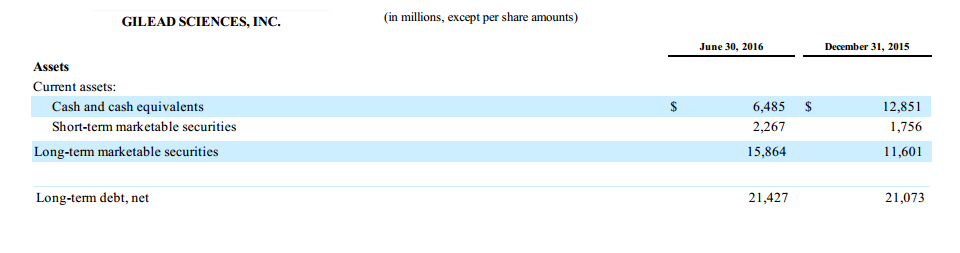

At the end of second quarter, Gilead had $6.4 billion in cash, $2.2 billion in short-term securities and another $15.8 billion in long-term securities, a total of more than $24 billion in cash and securities. Thats a full $3.1 billion more than the long term they hold on their balance sheet.

For a company that has been hit hard by declining sales, which is dragging down market sentiment, a quick acquisition could have done a lot of good to their top line and provided considerable support to its declining stock price. But Gilead has so far kept away from pulling the trigger despite the boat load of cash they have on hand.

It is not that Gilead is new to the acquisition game. Gilead bought Pharmasset in 2011 for $10.2 billion, bringing the hepatitis C franchise to the company. Gilead paid an 89% premium to buy Pharmasset and a lot of analysts believed the company overpaid on the deal, but Harvoni and Sovaldi, the two hepatitis C drugs, are the bread winners for Gilead right now, bringing in more than half of their total revenues in the recent quarter.

Despite having a successful acquisition in its past, Gilead has been extremely slow in the acquisitions market, which has recently seen tremendous activity with Pfizer (PFE, Financial), Novartis (NVS, Financial) and Sanofi (SNY, Financial), all major pharma companies, actively shopping in the market. Declining sales has hurt all the top players, and with most of the top pharma companies in the market to buy, deals have become scarce, expensive and time-consuming. Pfizer paid $14 billion to buy Medivation (MDVN, Financial) recently, paying a 55% premium to Sanofi’s initial bid.

“The offer is a 55-percent premium to Sanofi SA's initial bid to buy Medivation for $52.50 per share in April, which pushed the San Francisco-based company to put itself up for sale. It represents a 118-percent increase since Reuters reported on March 30 that Medivation had hired JP Morgan to handle interest from companies in a potential acquisition.” - Rueters

The acquisitions market is now more of a seller's market, with big companies fighting each other and running up prices to levels that defy the imagination. And this is possibly the only reason Gilead is sitting on the cash mountain, waiting for things to cool off. It’s good move by the company to not rush in, but a move that is possibly testing investors’ patience.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.