”‹Intel (INTC, Financial) has been on a transformational path in the last five years as the company attempts to wriggle itself out of its dependence on its Client Computing Group and move toward growth segments such as Data Center and Internet of Things. As PC sales around the world kept moving lower, the biggest casualty was Intel’s CCG, which makes processors for PCs and notebooks.

Intel’s revenue growth started to slow down big time in the last five years –Â around the same time when PC sales around the world were moving lower and lower. At the end of the third quarter, Intel’s CCG posted $8.89 billion, accounting for nearly 56.35% of overall sales. Since the proportion of revenue from this segment is quite large, Intel’s revenue growth is overly dependent on how the PC market performs around the world.

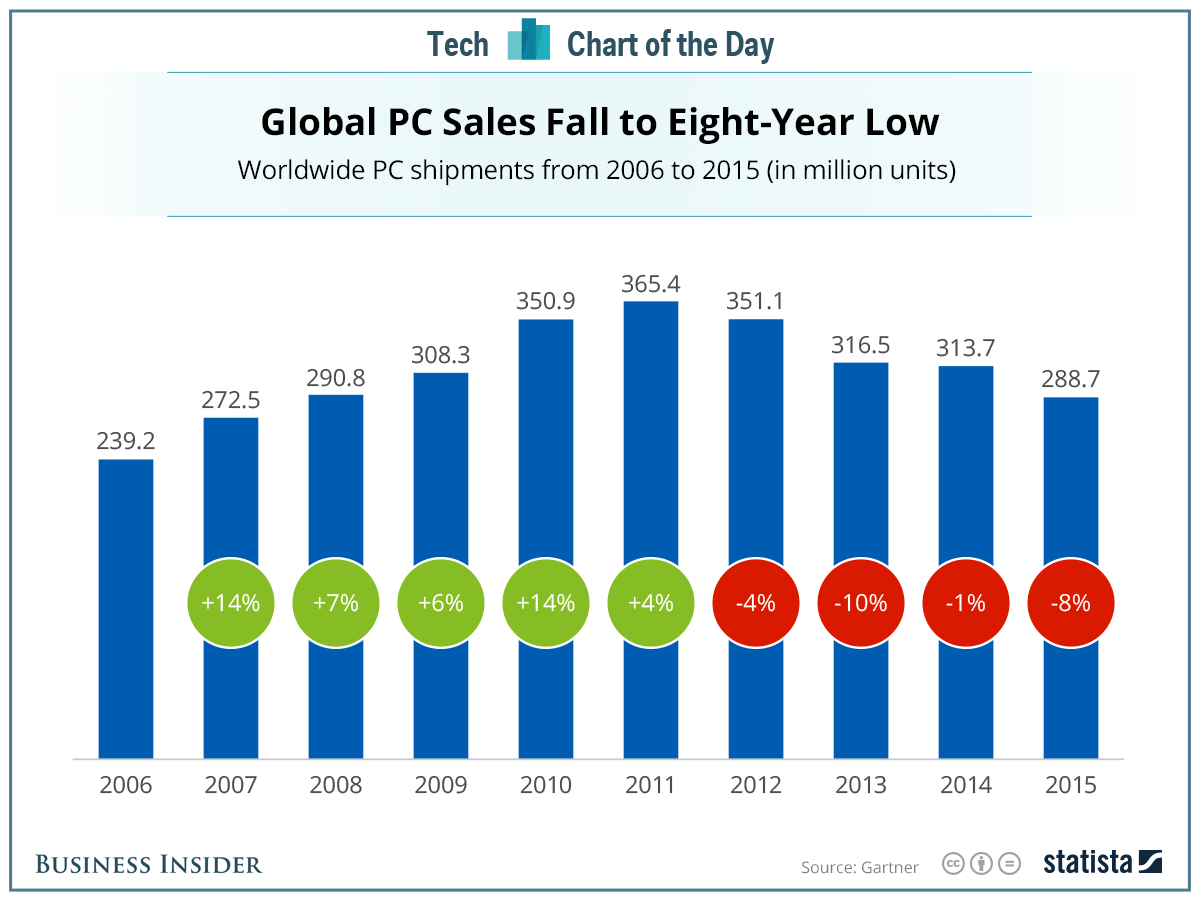

The growth of smartphones and mobile devices has severely dented the need for PCs, especially in the high volume consumer segment. The need for PCs will be there for many more decades, but the problem is that PCs have moved away from being a must-have to being an also-have. The enterprise segment’s need for PCs can never go to zero because we all need bigger screens to get our work done. But the days of solid growth are over, and the industry is moving toward more stable sales numbers around the world.

“After years of decline, I’m skeptical that we’re about to see a major uptick. Business upgrades will drive sales and might prevent a further drop for 12 to 36 months, but if consumers don’t hop back on the PC-buying bandwagon, it won’t be enough to stabilize sales long term. As someone who is still computing on a 2011-era CPU (I’ve upgraded the GPU several times), I’m not sure if Intel or Advanced Micro Devices (AMD, Financial) will field a product compelling enough to justify an upgrade from Sandy Bridge-E. Over the past four years, as we’ve met with companies like Intel and AMD, their marketing presentations have moved from emphasizing a two- to three-year upgrade cycle to a five- to eight-year upgrade cycle. At some point, the PC industry will have to face the fact that many users may simply never upgrade.” – Joel Hruska, Extreme Tech

Intel knows this problem exists and that is the reason why the company chose to double down on its efforts in data center, artificial intelligence and Internet of Things – segments that can drive growth in the future as the company earns stable revenues from CCG.

Intel’s Data Center Group (DCG), which stands second in terms of sales numbers for Intel with $4.54 billion in revenues during the third quarter, is halfway from CCG and is the one segment on which investors and the market are pinning their hopes to carry the future of the company. Intel has said the company expects a 15% annual growth rate from this segment, which was a bit optimistic but not undoable considering the rate at which cloud-based solutions are growing around the world.

Unfortunately Intel’s growth in the segment came in much lower than the bar the company set for itself. In the first nine months of the current fiscal Intel’s DCG posted a 7.67% growth, from $11.673 billion last year to $12.568 billion this year. Not a growth rate one would like to see if all hopes for revival are pinned on that segment.

“It’s a problem that has to be explained,” said Kim Forrest, a senior equity analyst at Fort Pitt Capital Group, referring to the slowing growth in the data center division. “Yes, there is some data moving to ‘the cloud,’ but they need to show that Intel supplies that area, too.”

Intel blamed the weakness in the enterprise market for the slowdown in the data center segment, but Intel has no choice but to pull up its socks and give its competitors a tough fight. CCG has done surprisingly well this year, but it cannot be expected to go on forever considering the health of the overall PC market.

Intel’s IoT group has not even touched $1 billion in quarterly revenue. During the third quarter IoT group posted $689 million in revenues and is still many years away from providing the kind of support Intel would need. Its best bet to shore up its sales numbers in the short to medium term, therefore, is DCG.

However, the current growth rate is not going to help the cause, and it possibly explains why the stock price edged lower after third-quarter results despite the company posting a 9% sales growth year over year.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.