Amazon’s (AMZN, Financial) international operations are yet to reach a consistent state of profitability for the company the way its North American retail operations have been in the last two years. I’d like to explore why that is. As an investor or a potential one, it’s important for you to understand the implications of size and scale on Amazon’s bottom line.

Big retailers operate on small margins and, to compensate for such margin levels, they move large volumes of goods. When volumes are low, bottom line numbers won’t look all that impressive, but when gross merchandise value (GMV) runs into the order of billions of dollars, even a 2% operating margin will bring in millions of dollars to the bottom line.

Why is this different from traditional retail margins?

E-commerce operations have another layer of cost to consider in the form of shipping. Traditional retailers don’t have to contend with that on a per-customer basis. To draw a parallel, every shopper who walks into a Walmart (WMT, Financial) and walks away with a purchase brings down the overall investment in that Supercenter or Sam’s Club or Neighborhood market. But in the case of Amazon, every order puts an increasingly heavier load on overall costs because each is attached to a shipping fee. That extra cost is often absorbed as the cost of goods sold but may sometimes be passed on to the customer.

The delicate balance that this represents to the e-tail equation requires scale to make it work in terms of bottom line profitability.

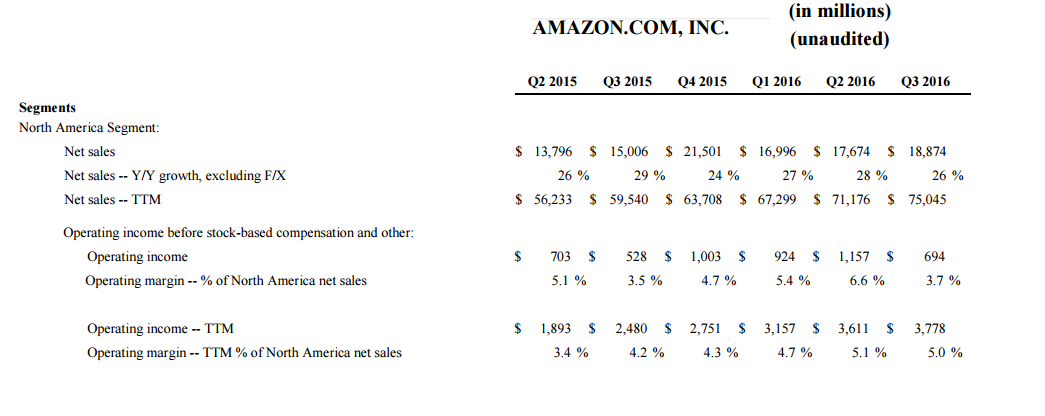

Amazon’s North American operations have now achieved that balance, and the unit is slowly moving toward profitability with margins improving steadily over the last two-year period.

As trailing 12-month sales increased from $56.23 billion in second-quarter 2015 to $75.04 billion in third-quarter 2016, operating margins improved from 3.4% to 5.0%. One or two quarters may be a coincidence, but consistent top-line growth mirrored in operating margins cannot. The higher the sales, therefore, the better the chances for an improvement in margins.

How it strengthens Amazon’s moat

In and of itself that creates a moat for any new player in the online retail space, and we’re seeing that even with seasoned e-tailers that haven’t yet reached such scale. They’re literally leaking billions of dollars in the process of attempting to achieve that delicate balance.

Even established players know that they need to increase their investments considerably in technology, subsidize some of the shipping costs if they want to price-match Amazon and keep pouring the money in as it slowly improves its sales numbers.

With deflation and competition already squeezing their bottom lines, this is not something that even big box retailers can afford. That also explains why big box stores are taking the slow and steady approach to e-commerce instead of trying to aggressively address the shift in customer preference toward online buying.

Amazon has cleverly used the slow-footed approach of its competitors to its advantage, by significantly ramping up the services it offers to its Prime members. At the core of the program lies its retail operations, and members are incentivized to order more goods from Amazon. By adding service after service to Amazon Prime, it is constantly increasing value, thereby reducing the probability of customer dropouts and increasing the odds of attracting even more customers.

That’s something we all witnessed during the deals week that started on Thanksgiving Day when online retailers gained the most from the decline in physical footfalls at major retail stores.

Since Prime members are known to spend more, on average, than non-Prime shoppers, Amazon’s GMV keeps increasing as Prime membership grows. That sort of scale allows Amazon to further reduce prices when necessary while still gaining in terms of margin expansion. That’s what we’ve been seeing over the past several quarters in its North American retail segment.

What this does is to create an increasingly stronger moat not just against traditional retailers, but even new entrants to the online retail space. Only a retailer with deep pockets and a large presence can afford to compete at those levels of efficiency – something that is critical to bottom line health. But even players like Walmart have only just stepped up their investments and activities around online retail, and it will be several years before they can start closing the gap that Amazon has created.

Having thus secured its market position in online retail, Amazon is moving to explore the physical retail domain. That’s something it has been trying to do for the last 10 years without much success. Even its new Amazon Go initiative is a long way from tasting success, but the company has realized that this is a big hole in its growth strategy for the next decade because it precludes it from competing on an even scale with the likes of Walmart and Kroger (KR, Financial) for a piece of the $606.26 billion grocery market in the U.S.

As Amazon’s moat widens by the quarter on the online retail front, the company is well aware that, unless it significantly increases its physical footprint in the world’s biggest retail market, it cannot be a holistic retailer covering all possible segments.

Disclosure: I have no positions in the stocks mentioned above and no intention to initiate positions in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.