NVIDIA’s (NVDA, Financial) revenue has grown at such a rapid pace in the last three quarters that its stock price has more than tripled during that time. The pace of growth has been so furious that valuation multiples have skyrocketed.

There are several reasons why NVIDIA will be able continue its revenue acceleration for the next several quarters so let’s take a closer look at the company’s data center segment, which looks all set to threaten the No. 1 revenue-earning position enjoyed by NVIDIA’s gaming segment.

In the last eight quarters NVIDIA’s lead earner nearly doubled its revenues while the data center segment nearly tripled its revenues. Being a newer segment and smaller in size, it’s understandable that growth will be faster.

That doesn’t mean gaming revenue growth is slowing down. It has been a long-time breadwinner for the company and a more mature market as well. But it still grew on the back of Pascal-based GPUs, accelerating growth to 63.45% in the third quarter over the prior period. Second-quarter growth was a mere 18.33% over the prior period.

Though the segment’s above-50% growth rate might continue for some more time, it will be difficult to sustain that kind of top-line growth over a long period of time. Nevertheless, the company’s leading position in the gaming market will provide it enough room to keep things moving at a rapid pace.

The growth in the data center segment is even more aggressive, driven by NVIDIA’s GPUs that address artificial intelligence, hyperscale supercomputing and the cloud industry as a whole.

Leading cloud companies such as Amazon (AMZN, Financial), Microsoft (MSFT, Financial) and IBM (IBM, Financial) have been watching their cloud revenues grow above 50% for the last several quarters. Microsoft wants to hit $18 billion in cloud revenue in the next few years, nearly double its commercial cloud revenues from last year. Clearly, this segment is growing fast and will continue that momentum for the next few years at the very least.

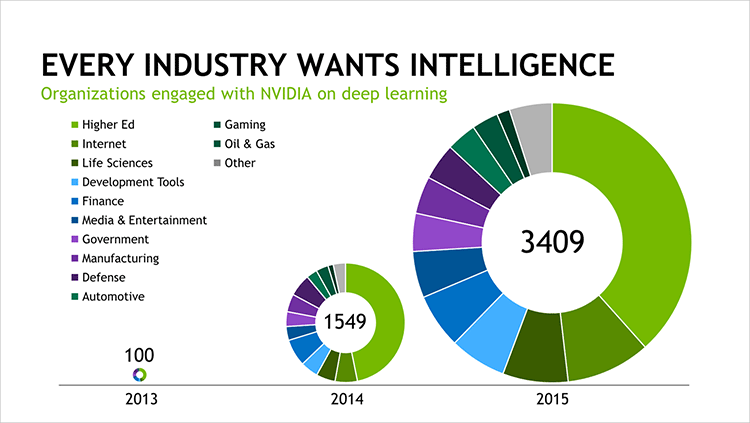

NVIDIA’s list of hyperscale and AI clients is long – Facebook (FB, Financial), Microsoft, Amazon, Alibaba (BABA, Financial), Baidu (BIDU, Financial), etc. –Â underscoring the company’s lead in the segment over its competitors. Intel (INTC, Financial) recently made it clear that it wants to compete in the AI segment but may be several years away from challenging NVIDIA.

“Cloud GPU computing has shown explosive growth. Amazon Web Services, Microsoft Azure and AliCloud are deploying NVIDIA GPUs for AI, data analytics and HPC. AWS has recently announced its new EC2 P2 instance, which scales up to 16 GPUs to accelerate a wide range of AI applications, including image and video recognition, unstructured data analytics and video transcoding.” – NVIDIA third-quarter earnings

AI and cloud computing are inseparable, feeding off each other's growth in a cyclical manner. As the push for AI heats up, it drives more demand for hyperscale computing. Conversely, the rapid expansion of data center presence by the world’s top cloud companies provides the infrastructure necessary to drive growth in AI.

"NVIDIA GPU is accelerating progress in AI. As neural nets become larger and larger, we not only need faster GPUs with larger and faster memory but also much faster GPU-to-GPU communication as well as hardware that can take advantage of reduced-precision arithmetic. This is precisely what Pascal delivers," said Yann LeCun, director of AI Research at Facebook.

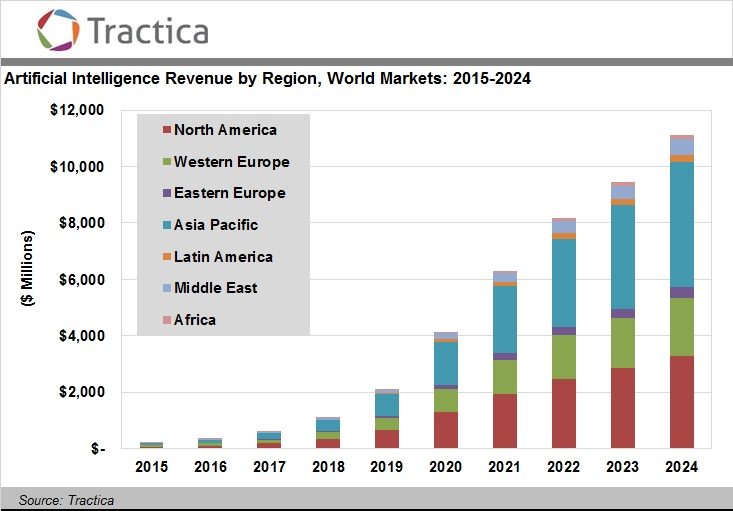

According to a Tractica forecast, AI revenue worldwide will grow from the current $643.7 million this year to $38.8 billion by 2025.

With no clear competition for NVIDIA in this segment, the company is poised to take significant market share before other companies get ready, thus providing enough runway for NVIDIA to keep its data center segment revenues growing for the next several quarters, if not several years.

But investors need to stay away from the company for some more time and allow things to cool off before jumping in. NVIDIA is already trading above nine times sales, pricing in most of the future growth and leaving no margin for error.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.