Intrinsically ETFs are a tremendous innovation and a great positive. Unfortunately at this stage if you want to raise a lot of money as an asset manager you need to play into fear and greed. Customers want more, and they don’t want to lose. Ever.

ETFs get investors more. They are much cheaper to run compared to an actively managed fund. With active managers, in the aggregate, failing to deliver returns in excess of their expenses ETFs win out. So far, so good.

However investors don’t want to lose, and they and their advisors select ETFs that deliver great returns and do so consistently. Start paying attention to how often people will use “consistently” when reviewing a strategy’s ability to make money. The more consistent one will often be favored. That’s understandable as making money consistently is much more valuable. Back when we were roaming the earth in bear hides, swinging clubs, downing a mammoth one year and starving the next did us little good. One year of starvation, and it’s game over. Perhaps we are programmed to love consistency.

Our love of consistency is so great we are overestimating its sustainability. It is so strong that ETF creators are almost forced, if they want a good chance of success, to launch ETFs that backtest well for quite a few years.

At the same time the mechanic of the ETF doesn’t treat the illiquid or low float issues well. ETFs are forced to buy or sell mechanically depending on their rule set. For example there’s a closed-end trust in The Black Swan Portfolio and when it was thrown out of the FTSE index, ETFs were forced to sell it. With few buyers, the trust stepped up and offered to buy back its own stock from the indexes. It paid 309p for the shares while its net asset value is 473p per share. The trust is winding down now.

ETFs don’t care; they just follow their rulebook.

Most recently Carl Icahn warned against the dangers of ETFs:

But in the market today, the danger is that you have all this money pouring in America into ETFs and ETFs are sort of almost blind buying. You just buy these ETFs and I always question the fact that if you're buying these stocks and you really don't know what you own, you're prone to these periods of time – there could be some kind of crisis and there could be a problem.

The blind buying wouldn’t be such a problem if it were indiscriminate broad market buying.

But it is not.

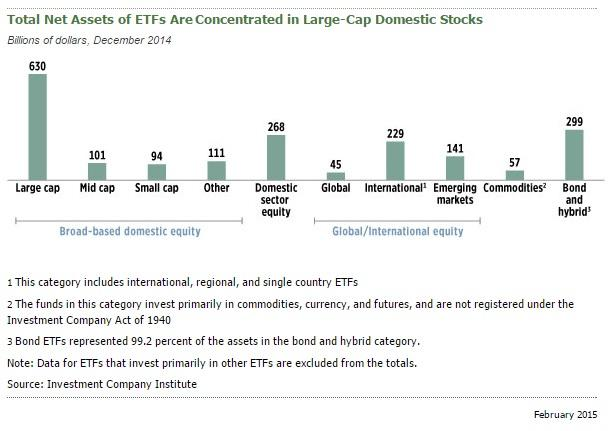

Most money flows toward equity ETFs, specifically toward U.S. large-cap companies:

Within that universe clearly companies with good momentum that backtest well are highly preferable. ETFdb.com has Amazon (AMZN, Financial) as a top 10 holding in 65 ETFs!

I just ran Sears Holding Corp. (SHLD, Financial), and it’s completely absent from the ETF universe.

The migration from active toward passive is not just a migration from high fees to low fees.

The money is pouring into a specific subset of the market that’s getting distorted although that means it is temporarily enjoyable to be present in that subset. But as Eminem said best:

When the music stops

I was happy having a deal at first

Thought money would make me happy but

It only made my pain worst,

It hurts when you see your friends turn their back on you dawg

When you ain't got nothing left but your word and your balls

Icahn has not been the first to warn us. On GuruFocus I’ve highlighted Richard Pzena’s warnings as well:

All active investors pay attention to the price. They all consider value. Passive investing pays no attention to the price paid.

That means in a sense, all active investors, within the constraints of their style box, are value investors.

Meanwhile, while allocating to passive, people are actively allocating toward liquid, momentum stocks with low volatility.

And warnings by other value investing greats, like Bruce Berkowitz (Trades, Portfolio)’s (emphasis mine):

On CNBC Berkowitz talked about index investing. It’s a great solution if you don’t get spooked, you don’t invest at a time the index is at an extreme valuation or when interest rates are at a historic low. If and when interest rates go up, that’s a gravitational pull on all assets.

Murray Stahl (Trades, Portfolio) in the FRMO Corp. (FRMO, Financial) annual letter:

As a consequence of the industrial scale upon which indexes operate, the largest companies frequently have valuations far in excess of smaller companies. For example, large-capitalization shares have outperformed microcapitalization equities for years. The Standard & Poor's 500 trades at nearly two times the price-book (P/B) value ratio of a typical microcapitalization index. This is very unusual.

However, the enormous industrial scale of indexation investing, as well as the market capitalization float adjusted methodology of weighting, requires maximum trading liquidity that simply cannot be provided by genuinely small companies.

Stahl and Steven Bregman's FRMOpublished a large amount of research on the subject that is a must read.

Bill Ackman (Trades, Portfolio) wrote in his early 2016 letter:

We believe that it is axiomatic that, while capital flows will drive market values in the short term, valuations will drive market values over the long term. As a result, large and growing inflows to index funds, coupled with their market-cap driven allocation policies, drive index component valuations upwards and reduce their potential long-term rates of return. As the most popular index funds’ constituent companies become overvalued, these funds' long-term rates of returns will likely decline, reducing investor appeal and increasing capital outflows. When capital flows reverse, index fund returns will likely decline, reducing investor interest, further increasing capital outflows and so on. While we would not yet describe the current phenomenon as an index fund bubble, it shares similar characteristics with other market bubbles.

When the music stops you know where you won’t be finding any chairs.

Disclosure: Author doesn't own any stocks mentioned but is short an S&P 500 low-vol ETF which may contain stocks mentioned.

Start a free seven-day trial of Premium Membership to GuruFocus.