Wal-Mart (WMT, Financial) reported strong fourth-quarter results, beating the market forecast on the earnings front while missing revenue expectations. The world’s largest retailer posted adjusted earnings per share of $1.30 with revenues of $130.94 billion for the quarter. The market was expecting $1.29 adjusted EPS and $131.22 billion in revenues.

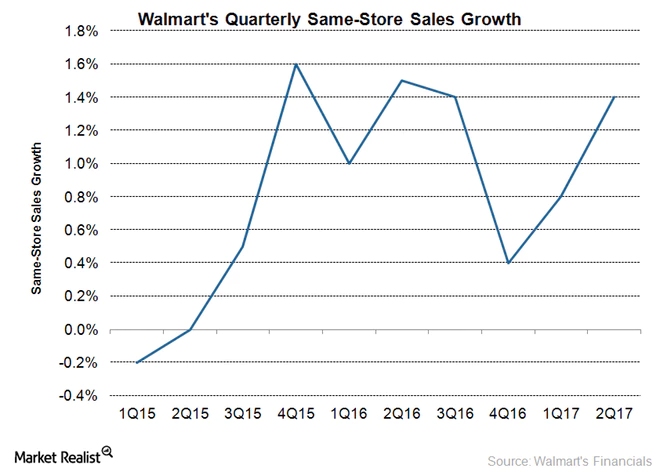

Comparable store sales increased 1.8%, representing the tenth straight quarter of comps increase for Wal-Mart. The company made massive changes to its strategy during this period, shutting down its smaller format express stores, expanding its neighborhood market stores, buying e-commerce company Jet.com and proritizing capital expenses toward e-commerce, increasing the minimum wage and so on.

Some of these decisions will eat into its margins, but Wal-Mart, spurred by competition, seems to finally be ready to sacrifice its margins as it searches for top-line growth.

The company laid out its capital expenditure plan at its investor day in October. Capital expenditures are expected to be approximately $11 billion in fiscal 2018 as it facilitates new store openings, accelerates the pace of remodels and invests in e-commerce.

Some of those efforts have already started to yield results, which is evident in the growth of comparable store sales over the last two and half years. The Jet.com aquisition will surely help the company ramp up its e-commerce sales, but it will take some time to see the results filter down to the bottom line.

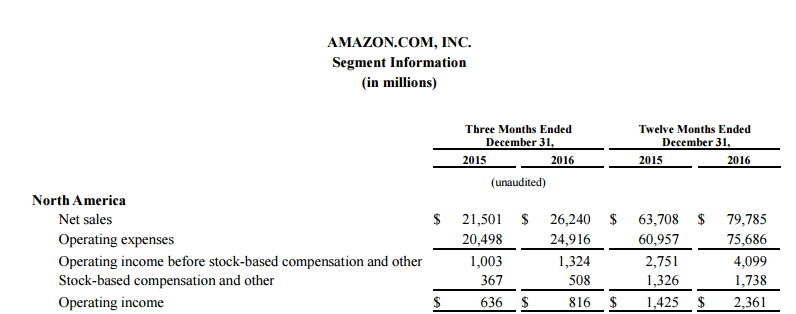

On the other hand, Amazon’s (AMZN, Financial)Â growth has been relentless, and the e-commerce giant keeps eating into the U.S. retail market. For fiscal 2016, Amazon reported $79.78 billion in net sales from the North America region, a growth of 25.23% compared to the previous year. The problem is, double-digit growth is not typical when sales volumes are approaching $100 billion. But the fact that revenues are rapidly growing and the operating margin has already hit close to 3% means there is still a lot of steam under Amazon’s retail hood.

That should worry Wal-Mart because Amazon is not creating new customers, it is merely taking them from other retailers.

But Wal-Mart has now found a way to hold its ground, as evidenced by the positive trend in comparable store sales. As the company noted during its investor conference last year, it will be slowing down store expansion plans while pushing a bit harder on the e-commerce front.

This is a great decision since its physical store footprint across the United States is already massive, apart from being something Amazon does not have. If Wal-Mart can improve e-commerce operations and streamline delivery options, then it can easily have the best online-physical hybrid store network backed by multiple delivery options such as direct home delivery and store pick-up.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.