IBM’s (IBM, Financial) stock price recovered nicely in 2016, with a near 21% return in the last 12 months.

One of the reasons for the recovery was the rate at which revenue was sliding slowed down. The company is still a year or two away from balancing the growing parts of its business against the declining parts, but with a near 3.2% yield, IBM’s stock is trading at an appealing price point. How stable will its dividend growth be in the near future?

At the end of 2016, IBM’s short-term debt was $7.513 billion, nearly canceling out its cash and marketable securities position of $8.527 billion. Long-term debt stood at $34.655 billion with an interest expense of $630 million. One of the reasons IBM’s debt is at such a high level is that, despite revenues declining year after year, the company kept making big-ticket acquisitions while it spent more than $21 billion in repurchasing shares in the last three years.

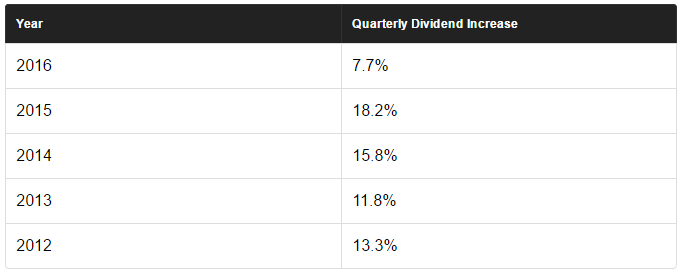

IBM paid $5.256 billion in cash dividends in 2016, or nearly 34% of its operating cash flow of $16.95 billion and 44.27% of its income from continuing operations of $11.87 billion. As is the case with any company that is watching its revenues decline, IBM’s dividend growth has inevitably dropped down to more sustainable levels.

Source:Â Motley Fool

With IBM not yet in a position to improve its revenues and considering the amount of debt on its balance sheet, IBM’s dividend growth rate will be slow for the next few years. Even if the company starts moving the revenue needle upward, it's not going to be easy for it to get back to the double-digit dividend growth period.

IBM’s free cash flow was $11.6 billion in 2016, which puts its dividend payout ratio at around 45%. It’s still at a manageable level from the free cash flow perspective, but IBM is likely to play it safe, doling out small dividend increases until it knows for sure that revenue growth has returned to the company.

With a near 3.2% yield, IBM’s dividend looks appealing, and there is the possibility of capital appreciation as well, but if you are looking for a pure dividend play stock for your portfolio, IBM’s risk vs. reward is not that attractive. Microsoft (MSFT, Financial), with its 2.4% yield, is much more attractive due to its cash hoard and its strong cash flow and balance sheet, which will allow the company to keep increasing its dividends.

Disclosure: I have no positions in the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.

Also check out: (Free Trial)