Last week, the U.S. Treasury Secretary advanced two proposals; one was a call for regulatory reform that is absolutely essential to the resolution of the current financial crisis. The other was a recipe for the insolvency of the FDIC, which would squander public funds to subsidize private speculation in troubled mortgage securities.

The Danger of Inaction

If there is any good news at present, it is that the capital infusions of late-2008 have temporarily stabilized the banking system, and that the U.S. economy is presently enjoying a brief and modest reprieve from the financial crisis. This is largely the result of an ebbing in the rate of sub-prime mortgage resets, which reached their peak in mid-2008, with corresponding mortgage losses and foreclosures a few months later. Since this crisis began, the profile of mortgage resets has been well-correlated with subsequent foreclosures.

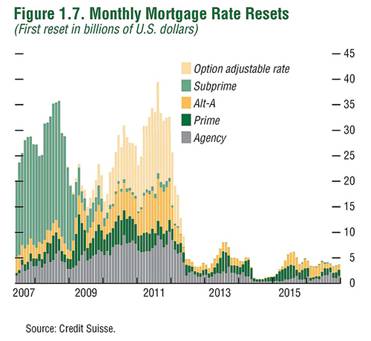

Unfortunately, the reset schedule above depicts only sub-prime mortgages. As the recent housing bubble progressed, the profile of mortgage originations changed, so that at the very peak of the housing bubble, new originations took the form of Alt-As (low or no requirement to document income) and Option-ARMs (teaser rates, with no required principal repayments).

A broader profile of mortgage resets is presented below (though even this chart does not include the full range of adjustable mortgage products).

Read the complete commentary

Also check out:

The Danger of Inaction

If there is any good news at present, it is that the capital infusions of late-2008 have temporarily stabilized the banking system, and that the U.S. economy is presently enjoying a brief and modest reprieve from the financial crisis. This is largely the result of an ebbing in the rate of sub-prime mortgage resets, which reached their peak in mid-2008, with corresponding mortgage losses and foreclosures a few months later. Since this crisis began, the profile of mortgage resets has been well-correlated with subsequent foreclosures.

Unfortunately, the reset schedule above depicts only sub-prime mortgages. As the recent housing bubble progressed, the profile of mortgage originations changed, so that at the very peak of the housing bubble, new originations took the form of Alt-As (low or no requirement to document income) and Option-ARMs (teaser rates, with no required principal repayments).

A broader profile of mortgage resets is presented below (though even this chart does not include the full range of adjustable mortgage products).

Read the complete commentary

Also check out: