Oracle (ORCL, Financial) CEO Safra Catz opened the fourth-quarter earnings call with this statement:

“We had a tremendous quarter in just about every way as cloud revenue, new software license and earnings were all much better than expected.”

The statement clearly summed up the direction in which Oracle is traveling at the moment – one that has already shown us a glimpse of Oracle’s potential in the fast-changing technology industry.

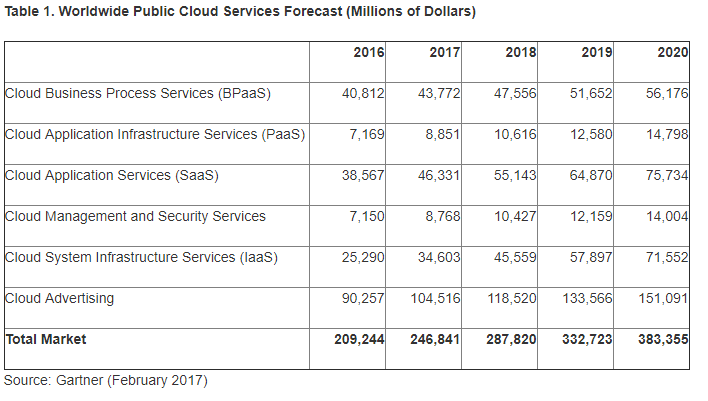

As cloud adoption around the world accelerates, more and more enterprises are eschewing traditional methods of software sales and replacing them with as-a-Service variants that reduce costs and shift the onus of upgrades and management to the vendor. The Software-as-a-Service segment is expected to expand significantly over the next five years, moving from $38.56 billion in size in 2016 to $75.73 billion by 2020.

The Infrastructure-as-a-Service segment and its close cousin, Platform-as-a-Service, are both expected to expand at double-digit rates during that period as well.

The problem for Oracle was that it was initially standing outside this wave of growth, allowing Amazon (AMZN, Financial) and Microsoft (MSFT, Financial) to run away with the shifting fortunes of the technology industry on the strength of their cloud-based offerings. Oracle’s bread and butter has been selling software and hardware to companies so that they can manage the infrastructure, and cloud was anathema to them. But it was Oracle’s own market that was slowly being eaten by the cloud industry.

And yet, big enterprises were holding out, watching the growth of cloud, some absolutely staying away, some using the hybrid approach that allowed them to keep their infrastructure but bring some of the advantages of cloud at the same time. There was a small portion of enterprises around the world that already made their move to cloud, especially the younger generation ones like Netflix (NFLX, Financial), Snap Inc. (SNAP, Financial) and so on.

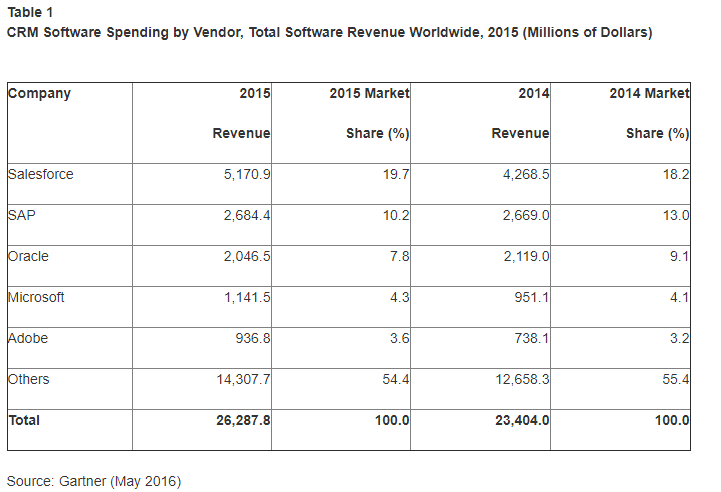

This allowed some breathing space for Oracle as its revenue didn’t plunge overnight due to the growth of cloud. But it was amply clear that finding new potential customers who would be willing to pay for annual software licenses and hardware would be fewer and farther between over the next few years and might well disappear in the long term. Take the customer relationship management – or CRMÂ –Â market for example: Salesforce (CRM, Financial), which kickstarted the as-a-Service model for selling software in the CRM segment, has been doubling its revenues every few years and is running fast toward $10 billion in annual revenues.

The entire CRM market was worth around $26 billion in 2015 with Salesforce holding nearly 20% of that market – and it was growing at double-digit rates. You cannot compete with a No. 1 player in the segment using a previous generation sales model.

Oracle realized that it had to change its approach and go head on in the cloud segment. It chose to strengthen its Software-as-a-Service segment, which led the company to pay around $9 billion to buy the world’s No. 1 ERP cloud company, Netsuite, last year. At the same time, it also expanded its data centers around the world and is slowly building out its Infrastructure-as-a-Service offering.

Cloud revenue growth has accelerated for Oracle over the last four quarters, and it might continue in that direction simply because the company has finally had a taste of success. During the fourth quarter, Oracle’s total cloud revenues reached $1.361 billion, accounting for 12.4% of its overall revenues.

The great news for Oracle is that this segment grew 60% in constant currency during that quarter, more than compensating for the 4% decline in software revenue and 12% decline in hardware. We can expect this trend to continue over the next several quarters as Oracle slowly emerges from its own shadows with a newfound confidence to compete with the big boys of cloud computing.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.