Trading at 18 times earnings, Apple (AAPL, Financial) is the cheapest of the top 10 largest companies ranked by market capitalization. Thanks to smartphone sales slowing down around the world and the lack of new product launches from Apple other than the cyclic iPhone release and other product refreshes, the market is not expecting Apple to aggressively grow its revenue over the next 10 years. As a result, the company trades at low valuation multiples in comparison to other tech giants.

To a large extent the market’s fears are true. Apple, which used to surprise the world with groundbreaking products, has now gone after incremental innovation as it keeps upgrading its products and software instead of launching new products that can radically change our lives. With nearly 60% of Apple’s revenue coming from iPhone sales, a bulk of Apple’s revenue growth is directly tied to the state of the smartphone market in the world.

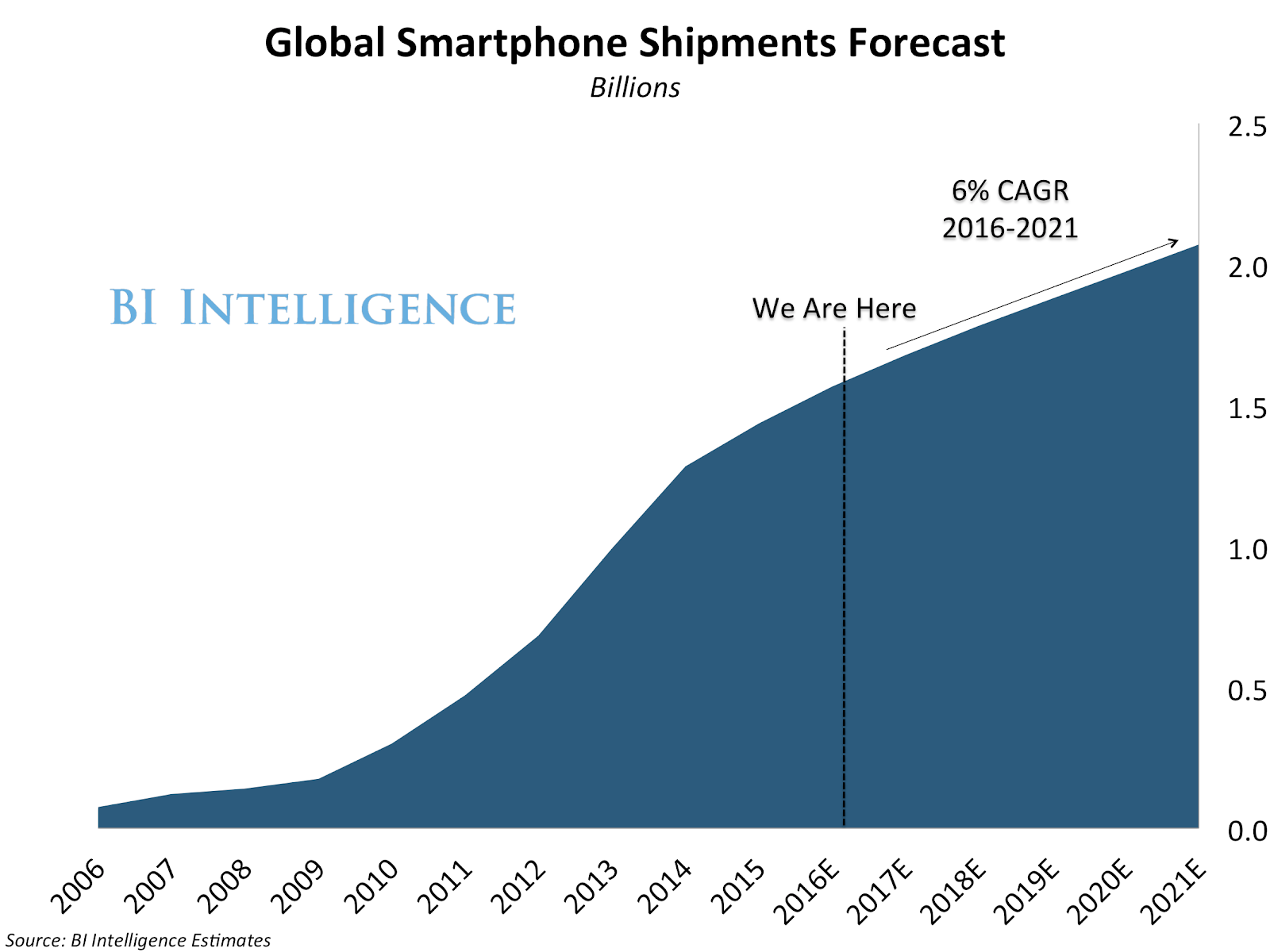

Smartphone sales have moved from a period of double-digit growth to midsingle-digit growth, and most of that growth is now coming from emerging markets, where the market for premium smartphones is not as big as it is in developed economies. Apple has quickly moved to beef up its services portfolio, the lead growth segment, which posted double-digit growth in the last few quarters and helped Apple’s overall revenue growth in the process.

But even if we accept the new reality that Apple’s revenue growth is going to be slower over the next two decades, we cannot discount the brand Apple has built. Its products are still some of the best in the world and, according to estimates, there are more than 550 million Apple users around the world and 1 billion active Apple devices.

These customers who are used to living within the Apple ecosystem will not be an easy target for competitors because they remain extremely loyal to Apple. And the growth of Apple services is a huge validation of the strength of that user community. The further the services segment grows, the higher the probability of users sticking to Apple in the long run.

Apple has already moved to a mature growth phase, and growth will be slow and steady over the long run, but its user base around the world will keep buying products and keep using its services, making sure that Apple’s cash flow generator keeps running for many decades to come.

Apple is already sitting on a mountain of cash and has now resorted to piling on debt to fund its share repurchases. Apple’s current dividend yield of 1.5% is something that investors should not miss as the current payout ratio of less than 40% provides an enormous amount of room for Apple to keep increasing those dividends over the next several years.

AAPL data by GuruFocus.com

Apple could have bought so many companies with the $250 billion-plus cash it has, but it hasn’t done that so far, and it’s most likely not going to do that in the future. Apple might buy few key technology-oriented companies that help its newer product lines such as autonomous vehicle software and augmented reality endeavor, and that gives it the edge in those areas. But this is not a company that is going to use that cash to diversify its business lines, which means most of that cash is going to be ploughed back to investors in the form of dividends and share repurchases.

AAPL data by GuruFocus.com

Apple is a steady buyer of its own shares from the market, and the company spent $25.105 billion in the first nine months of the current fiscal doing that. Apple will continue in that direction in the future as well. If you are a dividend investor, Apple should be an automatic choice for your portfolio due to its ability to generate cash and the cash mountain on hand.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.