Microsoft (MSFT, Financial) hasn’t been firing on all cylinders. It has been firing well on two cylinders: Productivity and Business Processes and Intelligent Cloud.

Meanwhile, More Personal Computing has been on stop-start mode. The cloud-based segments have performed so well in the last two years that they have, so far, masked the problems in the More Personal Computing segment. In this article, we will try to break things down in the More Personal Computing segment to see if it will keep dragging Microsoft’s growth rate down over the next five years.

During the fourth quarter of 2018, More Personal Computing reported $8.82 billion in revenues, accounting for nearly 38% of net revenues during the quarter. With almost one out of every $4 coming from this segment, let there be no doubt that this segment will play a huge role in Microsoft’s revenue growth rate.

More Personal Computing includes revenues from Windows, Search Advertising, Gaming, Surface and hardware. Of the $8.82 billion, a major portion of that will have come from Windows.

Surface

Surface, Microsoft’s best bet on the hardware side, brings around $1 billion in quarterly revenue for the company. As you can see from the chart above, revenue growth has remained elusive. The devices market is extremely competitive, and growth rates have already slowed to single digits for the segment. It will be extremely difficult for Microsoft to steadily improve its Surface revenue over the next five years.

Search Advertising

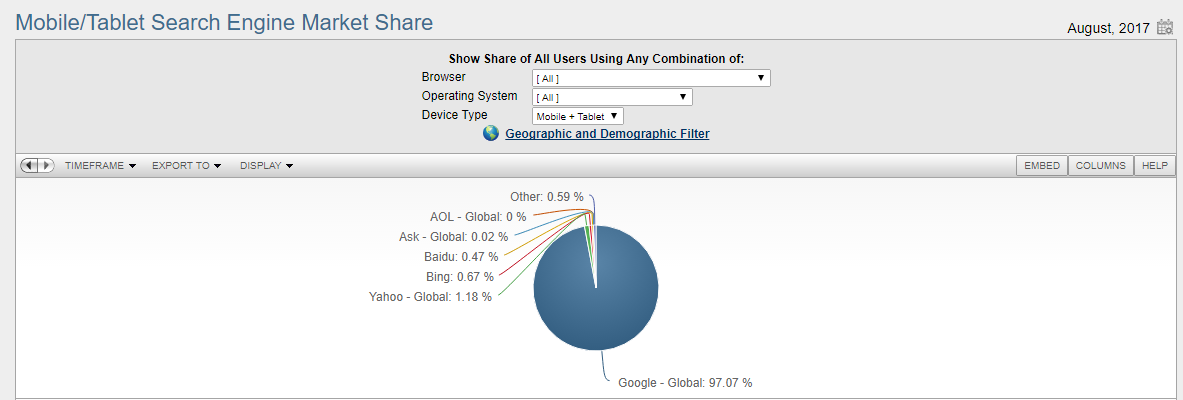

Search Advertising revenues have been growing at high single-digit to double-digit rates in the last five years. Google Search holds all the aces when it comes to search because it is the dominant force in the mobile search market, controlling more than 90% of the market. The growth of smartphones and the decline in PC shipments for the past five years or more is a clear indication that mobile search volume is going to keep increasing while desktop search volume is going to keep declining.

Source: Netmarketshare

The future of Microsoft’s search advertising revenues looks bleak in the mobile segment, which is controlled by Google’s mobile operating system Android. And let’s not forget Google Chrome, which is the No. 1 browser on both desktop and mobile. The combination of the mobile OS and browser markets being under Google’s control makes growth prospects for Microsoft’s search advertising look extremely unlikely.

Gaming

Microsoft’s position in the Gaming segment remains as good as it ever was. It is an extremely competitive market, and Sony (SNE, Financial) has always given Microsoft a good run for its money, but both Sony and Microsoft remain firmly in control of the gaming market. It will be difficult for a new competitor to rise up and challenge these two. As a mature market, growth will be slow and steady over the next five years. Gaming revenue will hold the fort, but it won’t be able to cover up for weaknesses in all the other products in the More Personal Computing segment.

That brings us to Windows, which accounts for the bulk of More Personal Computing revenues.

Windows

Desktop sales have already declined for five years in a row, as mentioned earlier, and we are well on our way to seeing the decline for six years in a row. No one really knows where the bottom is, but most of us can agree that the glory days of desktops are over. It is now in a fight for relevance in a market dominated by smaller devices such as smartphones, phablets, tablets, convertibles and so on.

The good news for Microsoft is that enterprises still need desktops, and that’s the segment that is going to help Windows revenue in the long run. It will never get back to the size it once was, but at least it will allow Microsoft Windows revenue to stabilize over the long term.

Conclusion

With nearly all the products facing issues of their own, the More Personal Computing segment will continue to weigh down Microsoft’s growth rate. The one big advantage Microsoft has is that the other two segments now contribute nearly 62% of Microsoft’s net revenues. They’re both growing fast, and they have better operating margins compared to More Personal Computing.

These two segments are already in a position to offset any weakness in the More Personal Computing segment. And the more they grow, the lower the impact More Personal Computing will have on Microsoft’s net revenues.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.