Pershing Square's Bill Ackman (Trades, Portfolio) is waging a proxy fight against Automatic Data Processing Inc. (ADP, Financial). He wants to get up to three board seats in order to further improve at the company. Yesterday, the firm released an hour-long presentation detailing the cause. I have reviewed the entire thing and came away thinking Ackman has some good points. I have listed the points he made that were most convincing to me in no particular order.

Wrong incentives

ADP did quite well over the years and it seems somewhat hard to believe management is not competent. Regardless, Pershing argues management is not incentivized appropriately. For example, management gets a bonus in the form of restricted stock if and when it exceeds margin targets. Under the system, management is best served by exceeding the target only ever so slightly. This will qualify executives for their bonus pay, but the bar does not get raised too much on them for next year. This sentiment is echoed more or less by independent analyst Morningstar, which rates overall management as poor and puts question marks on executive goals and underinvestment in technology.

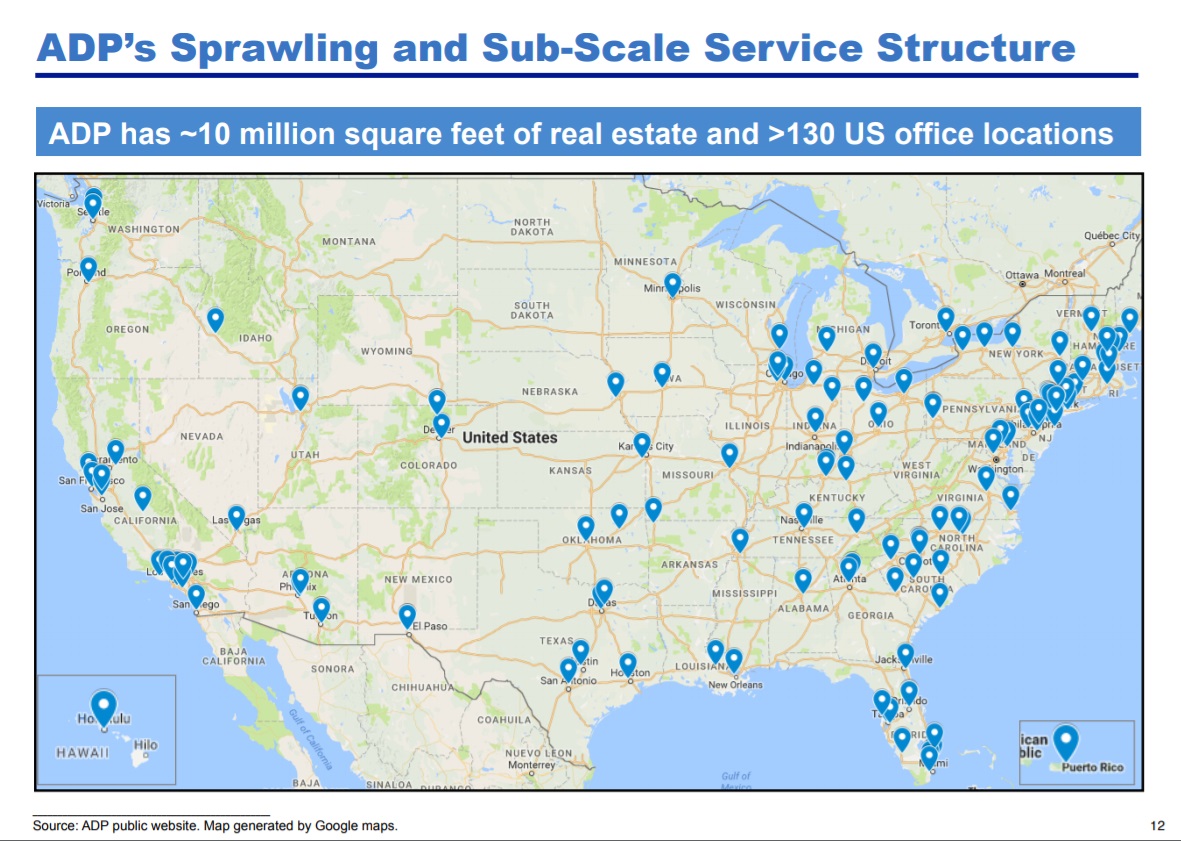

Real estate

Ackman spends about three slides talking about the incedible number of locations ADP has around the country. It does not actually need that many locations anymore. It is a legacy burden from its storied past, when physcial locations close to customers were a requirement. Even ADP's headquarters are not centralized. Important parts of the organization are spread out along the East Coast and there is even one segment controlled from the West Coast. Of course, this does not make it any easier to run ADP and it does not facilitate cooperatioin between different segments of the company. From a Glassdoor review (that are generally fairly positive):

"I honestly love this company, but if I had to pick something as a con, it'd be communication. It's a big company and communication can sometimes be a challenge, both across the company and interdepartmentally."

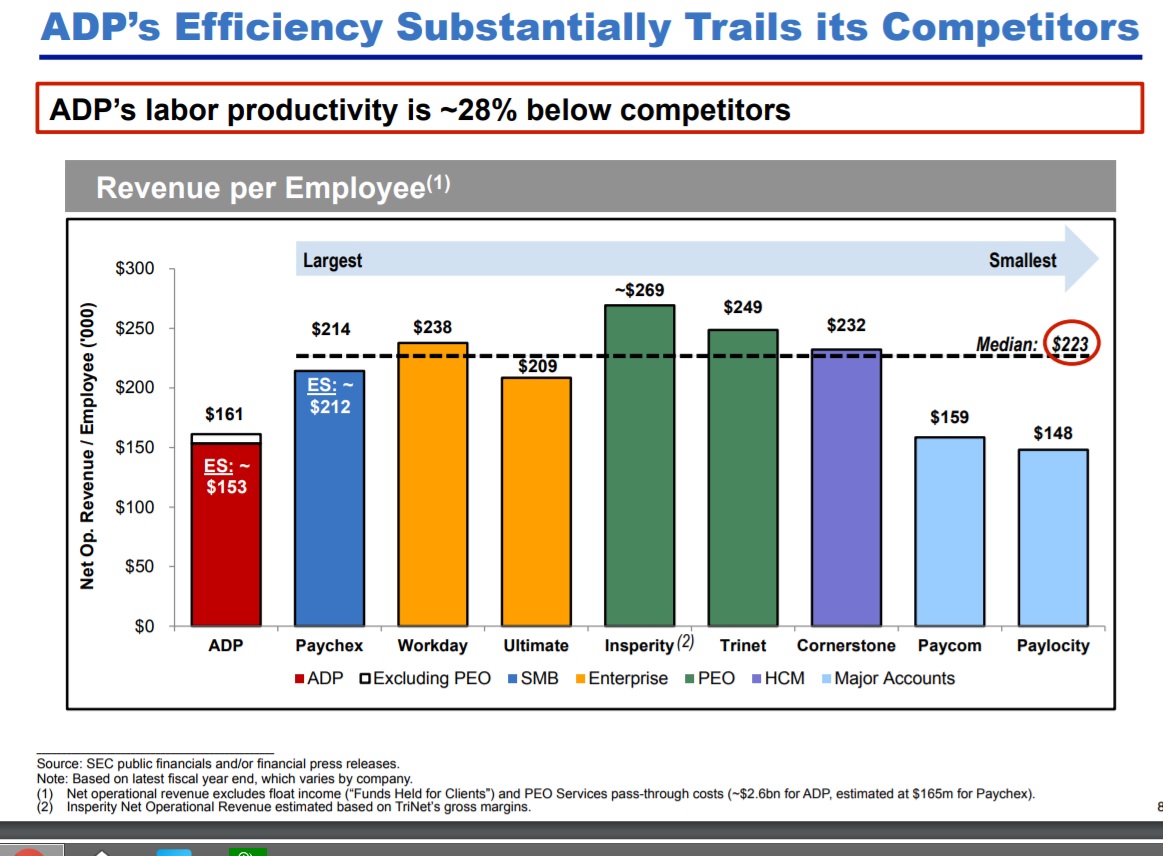

ADP is not as efficient as competitors

Pershing Square compared ADP's revenue per employee to a number of competitors that do pretty much the same thing. It turns out ADP lags most of them on this metric and, most importantly, it lags Paychex Inc. (PAYX, Financial), which is the other big player in the space. A possible explanation is underinvestment in technology, which is something both Pershing Square and other outside analysts have drawn attention to.

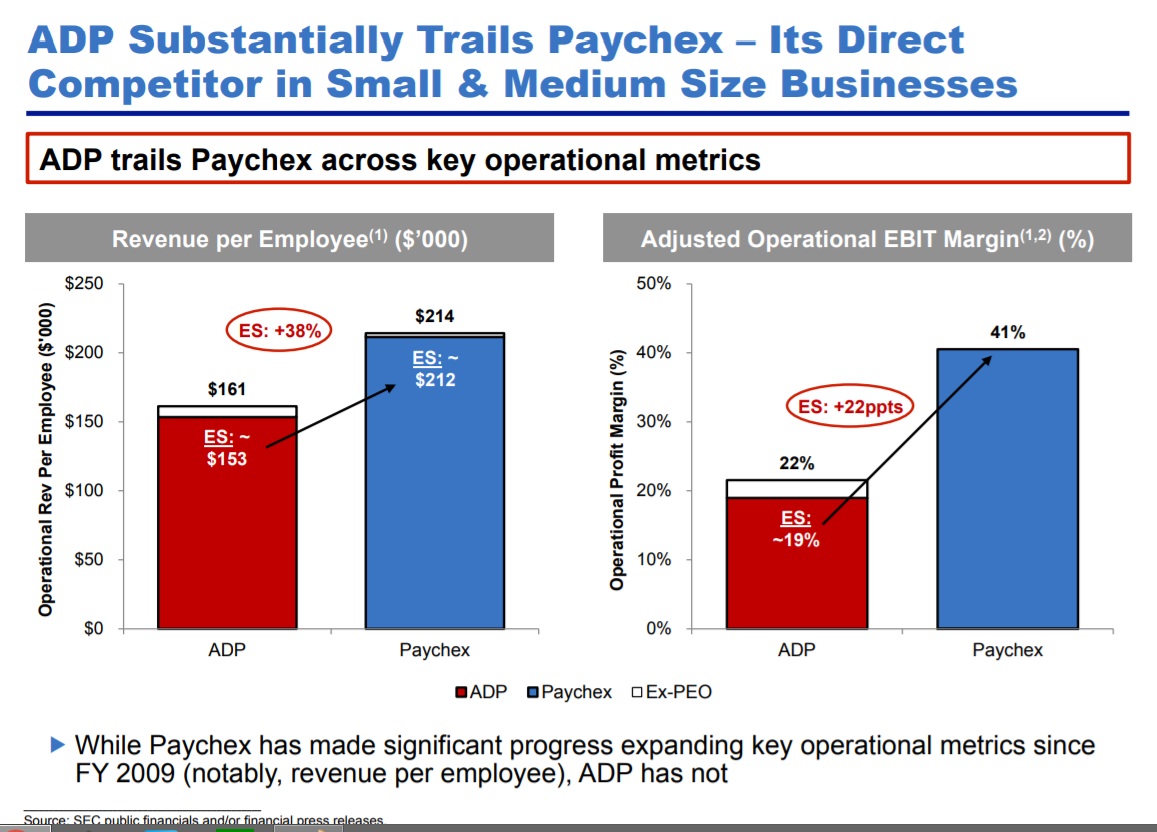

Lower EBIT margins

Paychex is an especially relevant competitor because it sports a market cap of $22 billion, which is close to half that of ADP. As companies get larger in size, they benefit from economies of scale (supposedly at least) while they cannot stay around a particularly profitable niche, which may cause margins to drop even as absolute profits go up. Paychex trades at 27 times earnings while ADP trades at 30 times earnings, which illustrates an improvement in margins would have a profound effect on the market value of the stock.

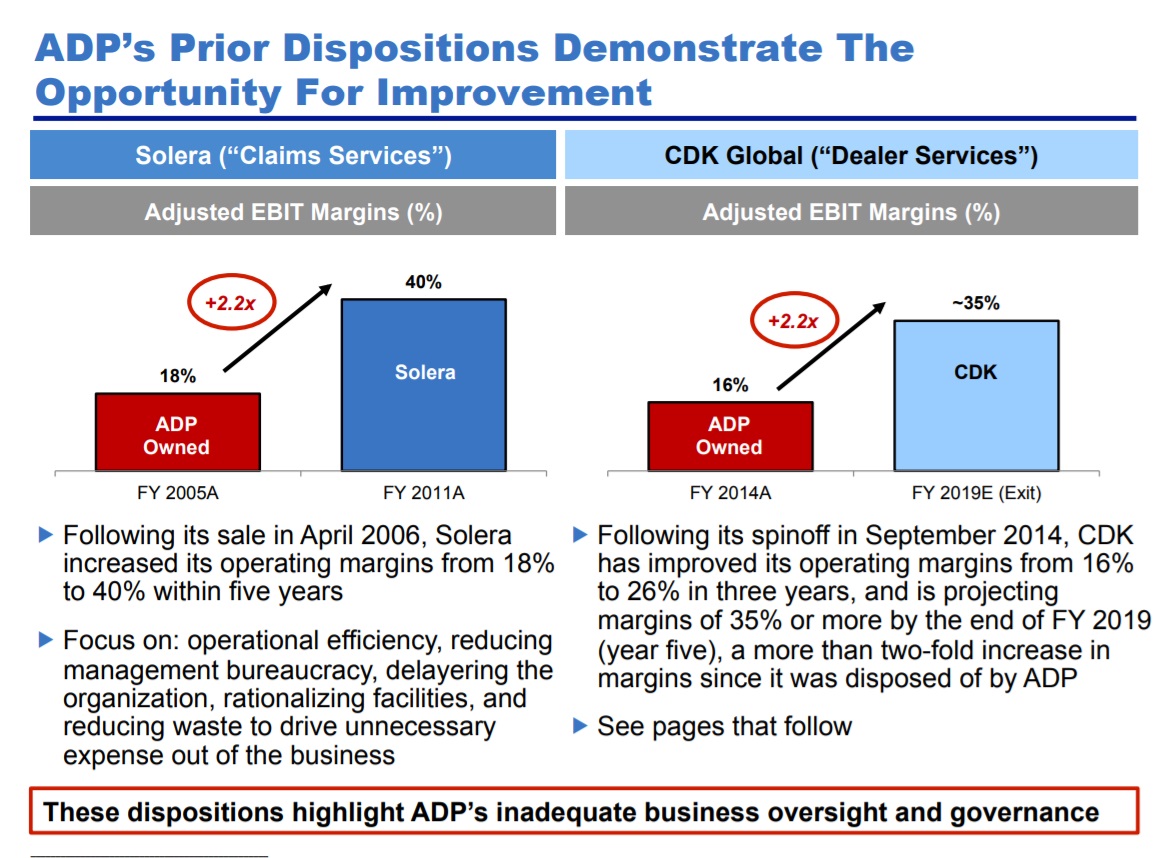

Margins

After ADP sold its claims services business to Solera Holdings Inc. (SLH), the business' margins expanded an impressive 22% within five years. It also spun off CDK Global, which increased its margins from 16% to a projected 35%. What is curious is how these companies went from average ADP margins to average Paychex margins after going out on their own. This is a very strong argument in favor of Ackman's case.

Conclusion

Ackman's presentation is an impressive display of Pershing Square's ability to do in-depth research, find unusual targets as well as come up with a compelling game plan. This kind of activist campaign is historically a strong suit of Pershing Square. It could be interesting to follow or support Ackman in this campaign.

Disclosure: No position.