General Motors (GM, Financial) did itself a huge favor by beating Wall Street estimates for the third quarter. The stock price has already surged by more than 40% in the last 12 months, and a bad third quarter would have stopped the improving valuation in its tracks. But thankfully, General Motors’ restructuring and global capacity reduction helped GM beat estimates by a wide margin.

General Motors posted adjusted earnings per share of $1.32 on the back of $33.6 billion in revenue while the market was expecting adjusted earnings per share of $1.12 and revenue of $32.72 billion.

The largest automaker in the U.S. reported a net loss of $2.981 billion for the quarter as it was hit by a $2.316 billion income tax expense due to the sale of its Opel/Vauxhall business in Europe. Third-quarter revenue declined by 13.6% compared to last year as GM has been scaling back production across the globe, cutting down production capacity by 26% and reducing U.S. dealer inventory by 160,000 units as the company pushes hard to improve profitability and stay nimble on its path to an electrified future.

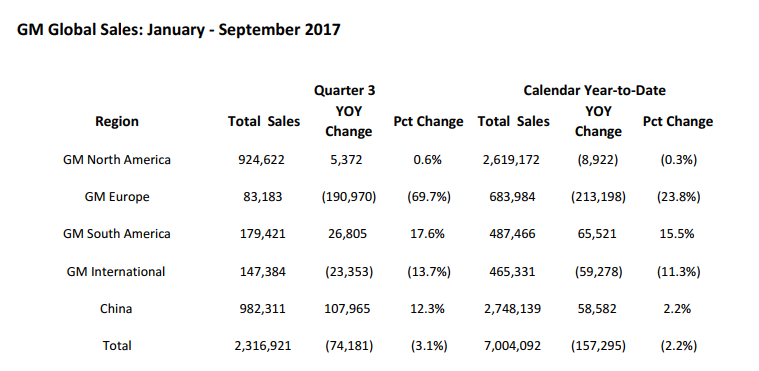

Sales remained strong in China, where GM’s unit sales increased by 12.3% during the quarter while things were almost flat in its home market. Total sales in China have now firmly gone past those in the U.S., and the double-digit growth clearly indicates that China will firmly remain the No. 1 market (in terms of volume) for GM in the future. GM has made a calculated decision to stay aggressive in the U.S. and China while slowing things down in other markets.

“We delivered solid results even with planned, lower third-quarter production in North America. We are managing the business with discipline to drive strong performance today while investing in higher-return opportunities, including those that will shape the future of transportation,” said Mary Barra, chairman and CEO of GM.

General Motors has fully committed to the EV push and has planned for two EV models in the next year and a half and 18 more by 2023. When Barra outlined the plan in September 2016, she strongly iterated GM’s vision for “a world with zero crashes, zero emissions and zero congestion.”

GM has made several moves to fortify its future in the transportation segment, which is undergoing massive disruption from the development of autonomous vehicles as well as the global push to convert entire product lines to electric or hybrid versions. GM has already invested in self-driving technology to a great extent, having purchased Cruise Automation and, more recently, Strobe Inc., a company specializing in LiDAR technology used in autonomous vehicles. Earlier this month the company also invested in Lyft, the ride-sharing rival of Uber.

GM stock seems to have broken out of its years-long struggle of being below the $40 ceiling, and if the momentum is sustained through the next several quarters, it’s possible the company will continually set new 52-week highs. If there was ever a perfect time to invest in GM, it could be now. And the higher-than-3% yield won’t hurt, either.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.