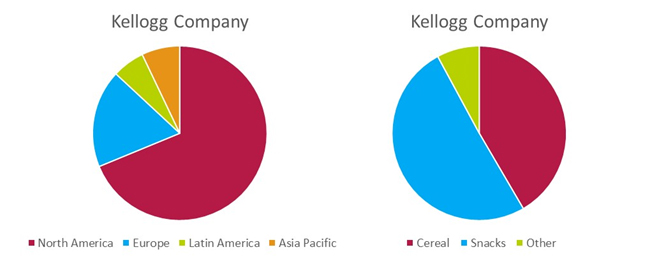

Kellogg (K) is a well-known, century-plus-old cereal and convenience foods manufacturer. The Michigan-based company has manufacturing operations in 21 countries and sells its products in over 180 countries across the world. Suffice it to say that Kellogg is a trusted brand that has penetrated all over the world.

But things have not gone according to plan for this global snacks powerhouse as sales growth has remained elusive to the company in the last five years. Net revenue has fallen from $14.197 billion in 2012 to $13.014 billion in 2016. Things are yet to improve, as the company reported $9.714 billion in revenue during the first nine months of the current fiscal, compared to $9.917 billion last year, a decline of $203 million in revenue.

The global consumer goods as well consumer staples industry has been going through a lean phase with nearly all major companies experiencing sales slowdowns. The high maturity level of the market, intense competition and slow growth in developing countries has made it extremely hard for these companies to show consistent growth, and things are not just going to be easy for them over the next five years.

With revenue growth remaining elusive, Kellogg will have to depend on balance sheet strength to keep its dividends flowing to its investors. The yield of 3.5% is indeed attractive for a dividend investor, but the company has plenty of short- to medium-term troubles to address before it can sustainably start increasing its dividends.

At the end of the third quarter Kellogg had $7.21 billion in long term debt with $267 million cash on hand. The company paid $64 million toward interest during the quarter, and the current debt looks manageable as the operating income during the quarter was $398 million.

The company paid $550 million in dividends during the first nine months of the current fiscal, or 50.7% of its operating income of $1.084 billion during the period and 65.3% of its net income of $841 million. The above-65% payout ratio is a bit concerning, especially because Kellogg is yet to return to a period of revenue growth.

Kellogg has a long history of paying dividends and has increased its dividends for the last 12 years. The company has been a bit frugal recently with its dividend payouts as dividends increased from $1.98 in 2015 to $2.04 in 2016, a growth of just 3%. Kellogg will probably continue the low single-digit dividend growth until the company starts to see some momentum in sales.

Data by GuruFocus.com

This loss of sales momentum explains why the dividend yield has shot up to more than 3.5%. But due to the strength of its brand name across the world, Kellogg should recover sooner rather than later, or at least be able to stabilize its revenues over the medium term. Kellogg is trading at under 14 times earnings, and investors should consider investing in Kellogg for the long term because there is quite a good margin of safety.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.