IBM’s (IBM, Financial) cloud revenues accounted for 20% of the company’s total revenues over the last 12 months.

It’s a huge achievement for the company, which forced its way into the cloud computing segment by buying cloud companies for the last several years as part of its efforts to move away from legacy products and build a software-oriented, high-margin business.

IBM admirably kept pace with Amazon (AMZN, Financial) and Microsoft (MSFT, Financial) for the last few years with all three companies growing their cloud revenues at strong double-digit rates. But IBM’s performance on the cloud front in the last few quarters makes it clear that its growth rate has slowed when compared to those of Microsoft and Amazon.

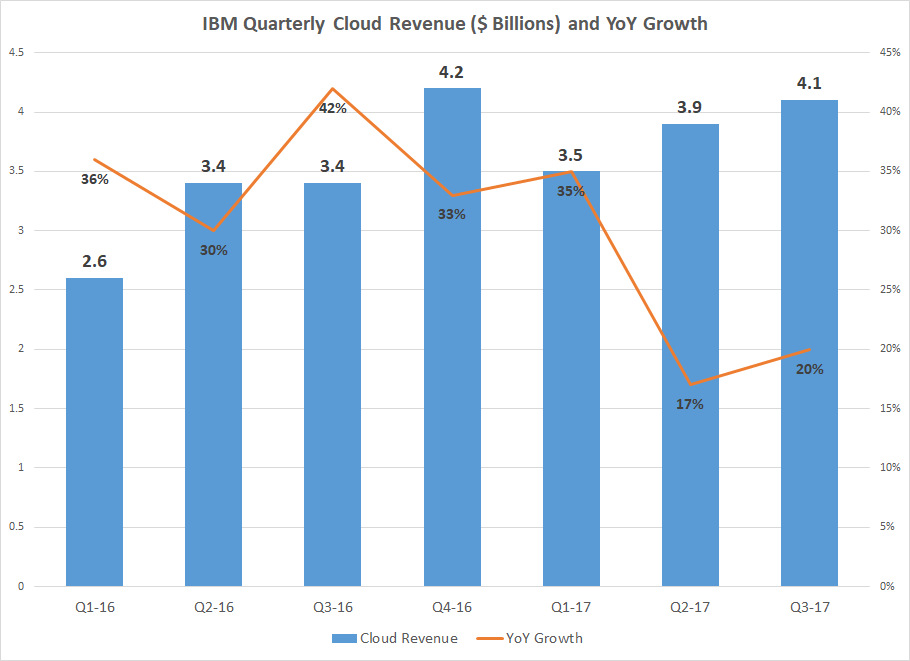

During the most recent quarter IBM reported $4.1 billion in cloud revenues, representing 20% growth when compared to last year. Amazon Web Services, on the other hand, reported 42% revenue growth during its most recent quarter while Microsoft’s commercialized cloud annual run rate increased by more than 50%.

All three companies now bring home more than $15 billion in annual revenues from cloud, but Amazon and Microsoft are still expanding at above-40% rates while IBM’s cloud revenue growth has fallen to 20% during the third quarter, following a 17% growth rate during the second quarter.

Thankfully, revenue is still growing in a segment that is pivotal to IBM, and Strategic Imperatives now account for nearly 45% of the company’s revenues. But IBM has to really pick up the pace and make sure that it keeps the gap small between itself and Microsoft and Amazon.

The greater that gap grows, the harder it will be to catch up. To make things worse, the cloud market has become overcrowded with Oracle (ORCL, Financial) and Google entering the fray.

That said, the cloud computing market is expected to continue its current double-digit growth over the next few years, allowing enough space for all the companies to grow, but the earlier IBM can get back to matching the growth rates of Amazon and Microsoft, the better it will be for the company's long-term future.

IBM is still not completely out of the woods, but the company managed to report flat growth during the third quarter and might be closer than ever to arresting the prolonged revenue decline of the past several years.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.