NVIDIA Corp. (NVDA) reported its earnings for the third quarter of fiscal 2018 last week and proved one thing very clearly: It's on a red hot revenue growth streak that started two years ago and is far from running out of breath.

The growth story is so strong that Wall Street keeps missing the company's numbers by wide margins. NVIDIA has now beaten analysts' forecasts for the top line as well as the bottom line for nine quarters in a row.

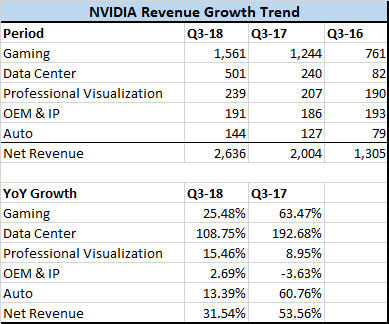

During the third fiscal quarter, NVIDIA reported revenue of $2.64 billion, up 32% compared to last year and $280 million more than what Wall Street was forecasting for the period. Revenue growth remained strong across the board as the company posted double digit growth in all the segments except for its Original Equipment Manufacturers and Intellectual Property business.

Why NVIDIA’s current growth won’t slow down in the near term

Gaming and Datacenter are the two largest and most important segments for NVIDIA. Together, these two segments accounted for nearly 78% of the company’s revenue and are still growing fast. As you can see from the table below, growth has come down a bit compared to last year, but an above 30% growth on a $10 billion annual run rate is as good as it gets.

NVIDIA doubled its revenue in the last eight quarters and may not be able to repeat that feat again in the next eight quarters, but it can still post double digit growth rates as gaming and data center segments keep outperforming the market.

Pascal remains one of the most successful graphics architectures, and the company cited strong adoption of Pascal-based GeForce GTX gaming platforms for its sustained revenue growth.

The company got into the data center business early on, and is now enjoying the benefit of being in the right place at the right time.

"Datacenter growth was fueled by strong demand by hyperscale and cloud customers for deep learning training and accelerated GPU computing," NVIDIA’s CFO told analysts during the third quarter earnings call.

With all the tech majors working doubletime on artificial intelligence and deep learning, the need for hyperscale computing is only increasing with every quarter, and NVIDIA has perfectly positioned its products to take advantage of that growth. Indeed, the data center business has a real opportunity to keep growing at a fast rate and get very close to gaming revenues over the next couple of years.

With the No. 1 revenue-earning segment still growing at double digit rates and the No. 2 revenue-earning segment enjoying a period of rapid adoption, NVIDIA’s current double digit rate of growth is far from running out of breath -- for this year as well as the next. The stock price will llikely continue to remain at these elevated levels, and investors need to stay cautious about buying into the stock.

Data by GuruFocus.com

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.