Let's analyze the 2.5% dividend yield from Whirlpool (WHR, Financial) to see if the underlying fundamentals align with what looks like a solid long-term dividend play.

First of all, we need to acknowledge the fact that growth has slowed to a crawl and could stay in the low- to mid-single digits for a while despite strong numbers posted recently. Over the nine-year period from 2008 to 2016 revenues have grown by a mere 9.6%, from $18.9 billion to $20.7 billion.

The only saving grace is that operating profits during the period have expanded by nearly 250%, from $549 million to $1.35 billion.

But Whirlpool is one of few companies with a globally recognized brand that the company can still leverage for steady – if slow – revenue growth in the future.

On the bright side, this year has seen Whirlpool report a decent 5.5% operating margin on the back of an 3.2% revenue growth. That’s not only a jump-start of strong revenue growth after a long hiatus, but it has set the tone for more positive expectations for the future. 2017 shipments in the U.S. are expected to come in at 4-6%, while other regions are expected to report flat to 2% growth.

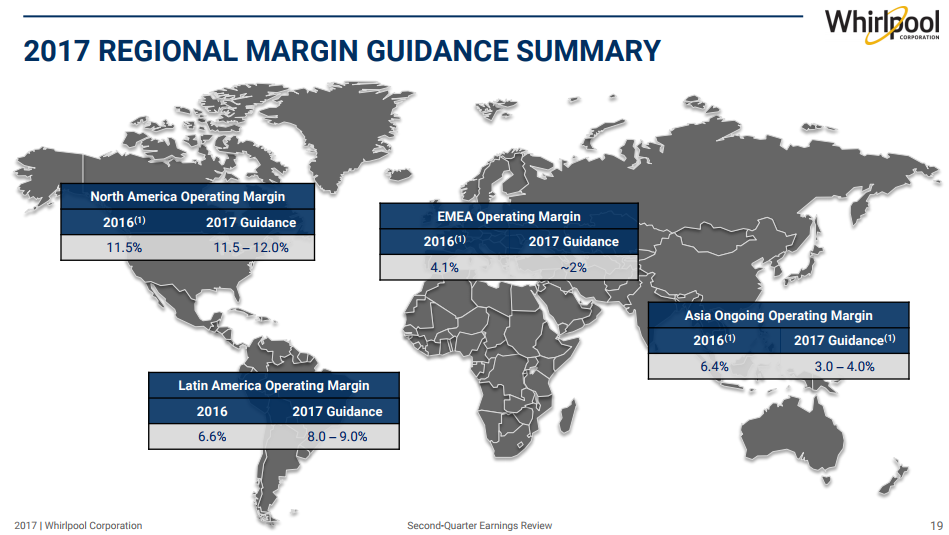

Whirlpool also expects strong margins in its key market (U.S) with a guidance of 11.5 to 12% in the region, which is great news considering that more than half of third quarter global net sales of $5.4 billion, about $3 billion, came from North America.

Source: Whirlpool Q2 Presentation

All this is indicative of Whirlpool being able to grow slowly and steadyily in a global household appliances market that is expected to grow at a CAGR of a little more than 6% through 2022.

From a fiscal health perspective, Whirlpool’s debt position is relatively safe. With a debt pile of $3.6 billion and cash on hand of $1 billion, the $42 million in interest paid during the third quarter looks very manageable.

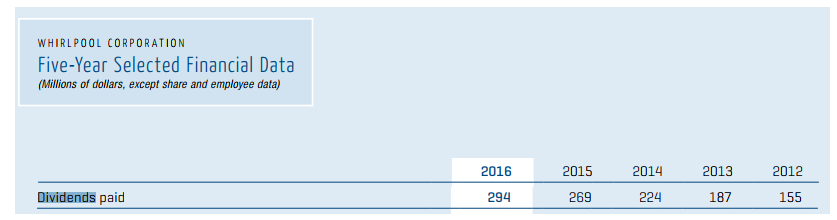

Dividend payout for the first nine months of the current fiscal year stood at $235 million, or a little more than 38% of net income.

Source: Whirlpool 2016 Annual Report

The per-share dividend has more than doubled to $3.90 as of 2016, compared to the $1.72 reported in 2008. A more than $300 million oulay for 2017 seems reasonable, and an indication that dividend per share can easily grow over the next five years.

The underlying fundamentals show a fair margin of safety for investors at the $170 price point that the stock is currently trading at, which was not true around six months ago when it popped over the $190 level around June 2017.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.