Last week we talked about how the market derives its expectations (it simply extrapolates current data ad infinitum) along with why it’s important to view macro data at the second derivative level (the rate of change leads important inflections in the trend).

A process that looks something like this.

We used these mental models to comment on a macro development we’re tracking, which is the decelerating growth in China, as well as what this could mean for markets. You can read the piece here.

These concepts are going to be vital in understanding how markets will unfold over the coming year. And this is because we’re on the cusp of some important trend reversals that will be occuring at the same time the market has become firmly anchored to the old narrative — in this game, winners anticipate and losers extrapolate.

The driving force behind this trend change will be a strengthening dollar. And it’s likely to kick into gear a positive reflexive loop that will drive large returns for those who are positioned correctly.

This reflexive loop is centered around George Soros’ idea of benign and vicious circles, or what we refer to as the core/periphery model.

We’ve written extensively on this idea, which you can read here. But the gist of it is that bull markets that are accompanied by a rising dollar tend to last longer than ones where the dollar is falling. That’s because there are numerous self-reinforcing processes (hence Soros’ use of the word “circle”) that drive an extended trend.

Here’s Soros on the power of benign circles (emphasis mine):

"The longer a benign circle lasts, the more attractive it is to hold financial assets in the appreciating currency and the more important the exchange rate becomes in calculating total return. Those who are inclined to fight the trend are progressively eliminated and in the end only trend followers survive as active participants. As speculation gains in importance, other factors lose their influence. There is nothing to guide speculators but the market itself, and the market is dominated by trend followers."

The dollar recently broke out of a four-month consolidation zone and is now rocketing higher, fueled by crowded short positioning and powerful fundamental tailwinds (i.e., rate and growth differentials).

If this bullish dollar trend continues it’ll become the most powerful macro driver of markets over the coming year(s). Not only will it extend the duration of the current bull market, but it will drastically impact market trends that have dominated over the last two years. We often refer to the U.S. dollar as Archimedes’ Lever. This is now more true than ever.

The incoming data suggests this trend is just getting started (again).

U.S. relative growth versus the rest of the world has rebounded and is expected to accelerate in the coming quarters. Stronger relative growth means more attractive returns which draws more capital flows that in turn push up the dollar, increasing total investor returns, thus making the U.S. more attractive and giving birth to a feedback loop.

When looking at the dollar you have to analyze the U.S. relative to Europe since the euro accounts for over 60% of the movement in the dollar on a trade-weighted basis. And on this front, the euro looks ready to kamikaze.

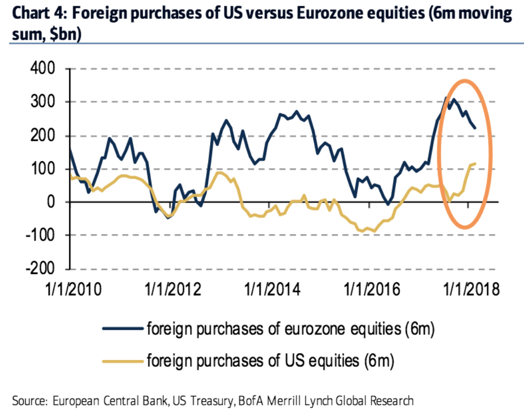

The improving relative U.S. economic picture makes for more attractive return prospects in U.S. markets as relative equity momentum picks up. This is driving speculative flows back to the core (the U.S.) and these flows drive exchange rates.

We can see this change in flows directly in the following chart from Bank of America. Foreign purchases of U.S. equities relative to eurozone equities have recently picked up, and quite significantly so.

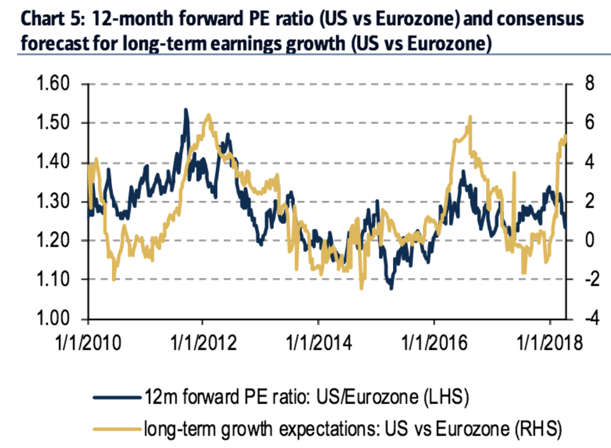

On a forward price-earnings basis, the eurozone is now not much cheaper than the U.S. While at the same time, growth expectations have strongly diverged in favor of U.S. companies.

This dollar trend is going to affect everything from rates to commodities (think gold and oil), to emerging markets stocks, as well as specific U.S. sectors. It will benefit some markets while hurting others.

Market wizard Ed Seykota once said, “Fundamentals that you read about typically are useless as the market has already discounted the price, and I call them ‘funny-mentals.' However, if you catch on early, before others believe, then you might have valuable ‘surprise-a-mentals.'”

The market is positioned for a weakening dollar. Everyone knows that everyone knows that the dollar is in a bear market because of the widening deficits in the U.S., chaos in the White House, overvalued U.S. stocks, the technical breakdown of the dollar bull trend, USD bull cycles only lasting seven years, and so forth. This is common knowledge and is now embedded in the price. Positioning shows that this narrative has become entrenched. The market, as always, has been extrapolating the past into the future. It hasn’t realized yet that the future has changed. It’s about to be in for a surprise.

Â