1. The company

Groupe Guillin (XPAR:ALGIL, Financial)

As of Nov. 23, 2018:

No of shares: 18.53 million

Free float: 5.9 million

Share price: 17.16 euros

Market cap: 317.25 million

Groupe Guillin's share price has declined substantially over the last six month to a level that appears undervalued. The new regulation environment has impacted the share price to levels not justified by fundamentals. The share price has the potential to double over the next 12 months.

1.1 History

Founded in 1972, Groupe Guillin is a family-owned company and a leader in plastic food packages in Europe. After two decades focusing on the French plastic market, the company turned into an international group in the early 1990s, accelerated by the acquisition of two French and one Italian competitors and the creation of a distribution subsidiary in the U.K.

1.2 Activity (brands and business model)

Based in France, Groupe Guillin is one of the largest European plastic food packaging manufacturer companies. It produces and sells thermo-formed plastic packaging for pastry, prepared foods, meats, fruits and vegetables. The company’s trademark includes “Patipack,” “Multipack” and “Ravipack.” Supermarkets and hypermarkets in France and Western Europe are among its largest clients.

The sales can be broken down per product as follows:

- Plastic packaging (93.8%): For pastry, prepared foods, meats, fruits and vegetables (No. 1 in Europe for pastry and prepared food). Moreover, Groupe Guillin sells plastic sealing films to industrial companies.

- Catering equipment (6.2%): Related to distribution for institutional catering such as hospital, schools, restaurants (insulated transport, meal distribution on trays and multi-serve meal).

The geographical sales breakdown comprises France (35%), U.K. (17.4%), Italy (11%) and others (36.6%), all located in Western Europe.

1.3 Strategy

Groupe Guillin has pursued an aggressive acquisition strategy.

July 2018: Purchased the CPET packaging business in the U.K. (total annual sales of 6 million euros) of German Etimex Primary Packaging GmbH through its U.K. subsidiary Sharpak Bridgewater Ltd.

September 2018: Strategic association with the French leader for recycling, Paprec Recyclage, to speed up recycling of PET plastic food trays.

October 2018: Started bilateral closed negotiations to acquire Groupe Thiolat (sales of 31 million euros in 2017, with 156 employees in two production sites in France and Romania), thereby strengthening its strategic positioning in paper and cardboard food packaging. The transaction should be finalized by the end of January 2019 at the latest.

2. Management

The key management positions are held by the members of the Guillin family.

François Guillin -- chairman

Sophie Guillin-Frappier -- CEO

Bertrand Guillin -- COO

In addition, Christine Guillin and Jeannine Huot-Marchand are members of the board.

2.1 Compensation

There does not seem to exist any public information with regards to the compensation of board and executive committee members, but this is a family-owned business (more than 64%), which has operated under a similar structure for nearly 50 years.

2.2 Company’s ownership

The following shareholders are holding more than 1% of the shares:

SC La Brayere: 22.90% (Guillin familly)

SC L’atelier: 20.06% (Guillin familly)

SC Le Chateau: 19.33% (Guillin familly)

FCP CDC PME Croissance: 3.43%

Guillin Family: 2.07%

KBC Group NV: 1.84%

BFT Investment Management: 1.46%

Candriam Investors: 1.43%

The Guillin family controls 64.36% of the capital, and the rest is the float. Apart from the Guillin family, there are three institutional holders of more than 1% of the shares. Other holders of less than 1% include Norges Bank (0.58%), Janus Henderson (0.71%) and Financiere Tiepolo SAS (0.50%).

In January 2018, Sophie Guillin-Frappier, CEO, purchased 10,000 shares at a price around 35.50 euros per share, and in November purchased 36,724 shares at a price around 17 euros per share, showing confidence in the company.

3 Company’s operating performance

3.1 Operating performance

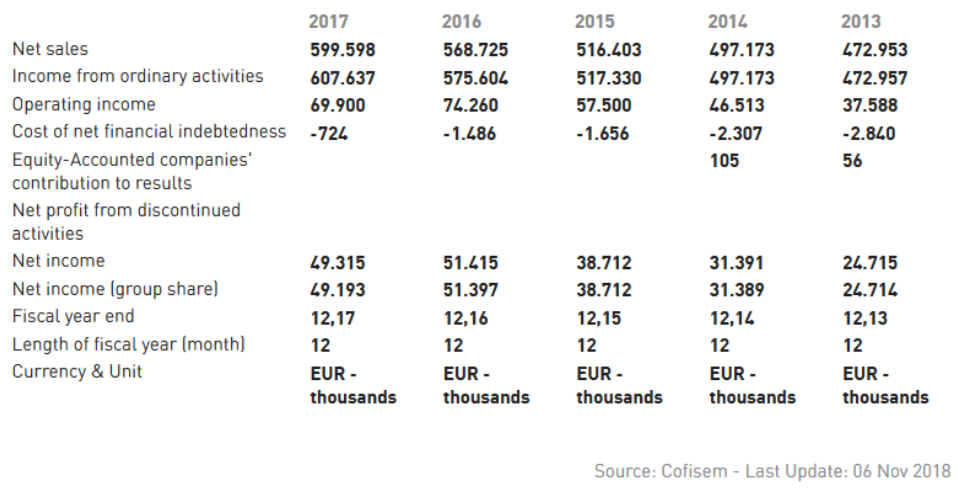

The revenue increased by 5.4% to 599.6 million euros in 2017 (revenue per share: 32.43 euros) after a steady increase in 2016 by 10.1%. The semi-annual accounts show revenue of 304.8 million euros as of June 30, 2018, a slight decline (-0.6%) compared to the first semester of 2017 (306.6 million euros). According to a company’s statement, this is mostly due to adverse weather conditions, causing a decline in sales in the fruits and vegetables sector.

Going forward, the recent acquisitions are expected to reinforce the company's position as European leader and boost profitability. The strategic association of Groupe Guillin with a leader in the key recycling business may be a visionary step for the company and offers potential growth for the future.

3.2 Financial situation

The group is managed by vigilant leaders.

Debt is low (105 million euros) and has consistently declined in the last 10 years (debt-equity around 20% as of June 30).

The current ratio is at its highest level ever (1.8).

The return on equity has been strong over the last 11 years (above 10% for nine fiscal years out of 11 and at 7% in 2008 and 2011, which were rough years for the European economy).

The management is properly incentivized, as this is a family-owned business where board members run the business themselves.

The group has long-term prospects.

(See section "risks" for more details.)

In short, the products that Guillin produces are persistent over time, and some simply need to be adapted to upcoming regulation. The company is fully aware of this necessity and took a series of measures over the past 20 years, which are listed in the "risks" section.

The group is stable and understandable:

The group's book value has grown consistently in a linear fashion over the last 10 years.

The group pursues an expansion strategy to build a strong and dominant European presence. This is a sustainable competitive advantage (also known as "moat").

The group’s shares can be acquired at an attractive price :

The margin of safety is very good versus earnings-based and FCF-based DCF valuations.

Low historical price-earnings ratio.

Low historical price-book ratio.

See section "market valuation of the company" below for more details.

3.3 Market valuation of the company

The share price has lost half of its value since June, falling to a market capitalization of 317.25 million euros. As a result, the price-earnings ratio declined sharply from 13 to the current level of 6.45, which looks reasonably cheap, well below its median of 8.99 and in the bottom part of the 10-year range between 3.87 and 16.47.

Similarly the price-book ratio is cheap, now below 1 at 0.9875 (three-year low), which is less than the industry median of 1.41 and in the bottom part of the 10-year range between 0.5 and 2.86.

Despite the difficult environment, the company has not issued any warning regarding its revenues or margins for the future, which seems to indicate that management has stable expectations. Moreover, the CEO purchased additional stock in January and November.

4. Risks

The first risk relates to the cost environment and increasing oil and plastic prices in 2017 and 2018, which has penalized Groupe Guillin’s margins. The recent decrease in oil prices may reverse some of the negative impact observed over the recent past.

The second risk is regulatory. Environmental concerns about plastic bags and products have increased among the population, and politicians began to respond with green policies to mitigate the impact. Analysts have taken into account the emergence of new regulations in Western countries that may impact the plastic business. In France, a new law (Loi EGalim) was passed in November that listed some plastic products that will be banned starting in 2020. There is another list of plastic products that will be forbidden from 2025. Groupe Guillin closely follows the list of products, which has evolved over time.

At a first glance, the new regulation is expected to penalize Groupe Guillin, yet these concerns have largely already been reflected in the share price and seem to offer an investment opportunity for two reasons.

First, the regulatory impact on Groupe Guillin’s future activity may be overdone.

Second, the company is diversifying its activity and started exclusive talks with Groupe Thiolat, a French company in paper and cardboard food packaging.

Moreover, Groupe Guillin appears to identify opportunities in the recycling business as another layer of diversification or complementary activity and engaged in R&D in association with Paprec Recyclage, a French leader in recycling and waste management. Being a frontrunner in recycling would allow Groupe Guillin to reap the benefits of the new regulatory environment. The plastic business is here to stay, accompanied with the adequate and fast-growing recycling business.

Environmental issues are actively tackled by the group, and going green is a priority.

In terms of materials, as early as 1998 the group made the strategic decision to abandon PVC and switch to PET. This material is in the same category as plastic bottles and is thus 100% recyclable. The group has also been producing RPET packaging materials, which include recycled used PET material. New substances are constantly being tested and considered, in anticipation of future environmentally friendly developments.

The Guillin Group’s production units are highly environmentally friendly. The cooling systems required by extrusion and thermoforming processes operate using water, which is fully recycled in a closed circuit. The very low levels of mechanical, solid and liquid waste emitted by manufacturing plants are treated by accredited waste management agencies, while all plastic off-cuts are reused internally.

The group’s carbon footprint was calculated recently, and operations have virtually no impact on the environment (water, air and soil quality).

For fruit and vegetable packing, cellular trays and wrappings are made using pulp produced from recycled paper. The Guillin Group is committed to reducing the plastic industry’s environmental impact, making sure that customers are aware that packaging products are lighter, recyclable and often made using recycled materials. Each year, the Group reduces the weight of its packages by 0.5-2%.

The Guillin Group is an active member of the plastic packaging trade association and has a long standing track record of committment to the active development of recyclable packaging.

Disclosure: the author owns shares of Groupe Guillin at the time of writing.

Read more here:Â

Contest: Seth Klarman Invested in This Junior Copper Mining Operation

Contest: Dickson Concepts - Growth and a Lot of Liquidity

Contest: Charles & Colvard Near an Inflection Point That Will Reveal Strong Growth