1. The company

Covestro AG (XTER:1COV, Financial)

As of March 10:

No. of shares: 181.3 million

Free float: 92%

Share price: 48.38 euros

Market cap: 9.18 billion euros

Covestro manufactures and markets polymers and high-performance plastics. It distributes polycarbonates, polyurethanes, adhesives, coatings, insulating materials and sealants, which are supplied to various industries such as construction, automotives, health, medical engineering and electronics.

Covestro’s share price declined in 2018 from a high of 95.70 euros to a low of 41.50 euros per share. This decline by more than 50% reflects the global weakening demand for chemicals and fears that the cycle for chemicals could be turning, which affected the entire chemical industry. Nevertheless, at the current price level (despite a significant rebound since the start of 2019), the company seems widely undervalued in view of Covestro’s strong fundamentals (see Section 3.2), position as market leader in premium polymers and resilient business for more than half its sales.

With a price-earnings level of 4.36 among the lowest in the industry (industry average 13), the share price has the potential to double over the next 12 months.

1.1 History

Covestro, formerly known as Bayer MaterialScience, arose from the Bayer Group’s chemicals and plastics unit, which started back into the 20th century. Covestro was established as a legally independent company only in 2015, as a spinoff from Bayer. Since its IPO in October 2015, Covestro's market capitalization and free float have increased continuously. In March 2018, Covestro was included in the leading German equity index DAX.

Innovation and sustainability seem to be two of the driving forces behind Covestro development. Among its recent achievements and innovations, Covestro and its partners demonstrated in 2017 that they can produce the crucial raw material aniline from biomass at lab scale and intend to accelerate the process, which is a significant contribution to sustainability and resource efficiency. In 2016, after testing that CO2-based materials have the same high quality as products created using conventional methods, Covestro opened a plant that uses the waste gas carbon dioxide as raw material for plastics. In 2015 Bayer MaterialScience developed Desmodur, the first bio-based curing agent for polyurethane (PUR) paints and adhesives, for which it won the “Bio-based Material of the Year 2015” award.

1.2 Business model

Covestro sees the global tremendous challenges, climate change, rising mobility, population growth and increasing urbanization as business opportunities for technological progress and economic growth. In its mission statement, Covestro appears to be committed to making a better world, inspiring innovation and driving growth through profitable products and technologies that benefit society and reduce the impact on the environment.

Covestro also places environmental social and governance (ESG) considerations at the top of its agenda, striving to reduce impact on the environment and create value, in line with the sustainability principle: “People, Planet, Profit.” It has set ambitious goals like reducing greenhouse gas emissions by 50% by 2025 through technologies that save energy and emissions in the production processes. R&D projects are aligned with United Nations’ sustainable development growth. High environmental awareness led Covestro to require all suppliers to be compliant with Covestro sustainable requirements.

1.3 Strategy

Covestro focuses on cash generation, with products that can generate above-GDP volume growth and aims at building resilient and diversified businesses that can perform well through the business cycles. Covestro seeks leading and defendable global industry positions and believes in product innovation as a long-term growth driver, by developing premium polymer materials, promoting innovation and providing sustainable products, technologies and solutions that benefit future generations.

Covestro’s global strategy is based on the acknowledgment of global megatrends such as climate change, increasing mobility, growing global population and rising urbanization. These challenges are viewed as significant value creation opportunities and a specific approach for each of its core business segments has been developed to face these challenges:

- Polyurethanes (PUR): Demand for polyurethanes is expected to grow at a rate higher than the economic growth rate. Hence, the group intends to reinforce its strength in the construction industry by making its products more sustainable, energy-efficient, and affordable, and evaluating the potential for optimizing facilities and production sites.

- Polycarbonates (PCS): New forms of mobility (including electromobility) call for innovative products, and Covestro is well positioned to take advantage of this trend through, for example, fiber-reinforced composite materials or materials with low-weight, high-quality optics and transparency. This segment is also expected to grow at a higher rate than that of the global economy.

- Coatings, Adhesives, Specialties (CAS): Covestro’s strength lies in the supply of coatings and adhesives to producers supplying the automotive, construction and furniture industries. Efficient expansion of capacities and product development closer to customers is therefore the main focus in this segment, which is also expected to grow at an above-average rate versus the global economy.

Each business segment of Covestro’s portfolio is aligned with the UN Sustainable Development Goals (SDGs) in support of global progress at the ecological, economic and social levels.

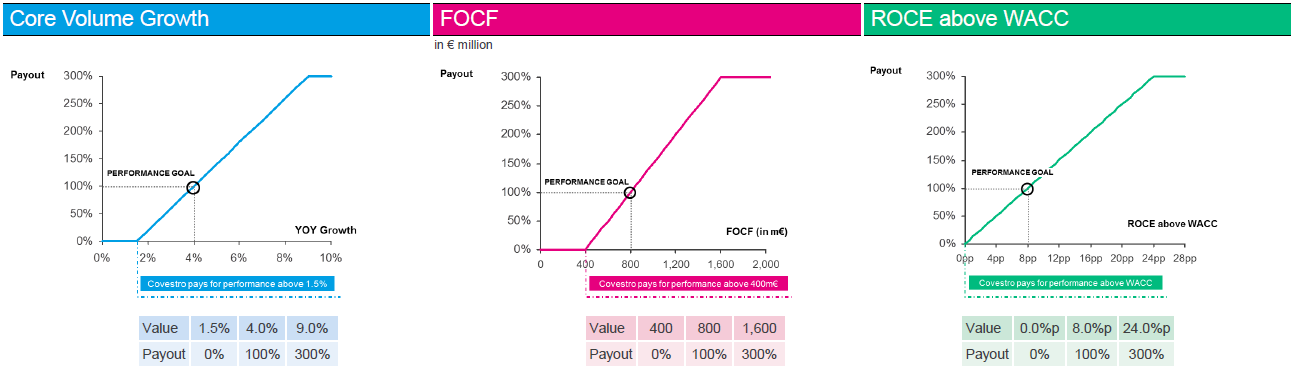

Furthermore, Covestro implemented a Short-Term Incentive (STI) program for 2019-2021, which consists of a uniform bonus system for all employees (including board members) based on three key metrics: core volume growth (CGV), free operating cash flow (FOCF) and return on capital employed (ROCE) above weighted average cost of capital (WACC):

Source: 2018 financials highlights presentation

This approach makes a lot of sense and is expected to yield efficiency and performance.

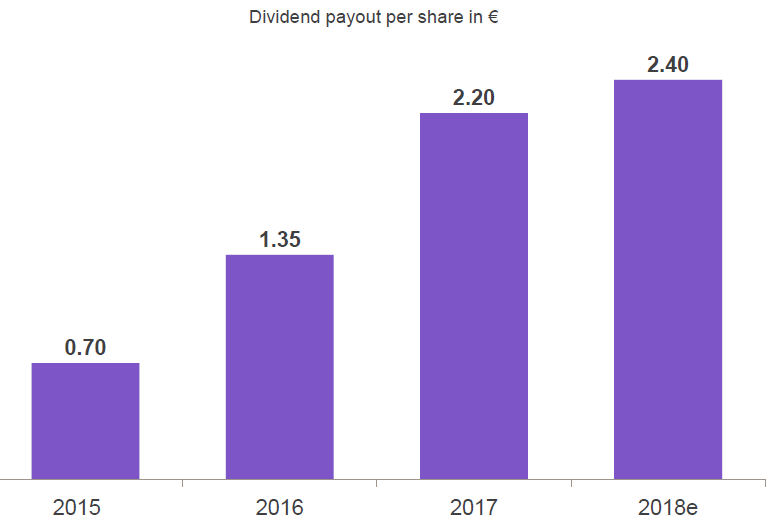

In terms of dividends, Covestro’s policy is to at least maintain or possibly increase dividends every year. For fiscal year 2018, a divided of 2.4 euros per share will be proposed at the annual general meeting, representing 9% year-over-year growth and 4.7% dividend yield.

Source: 2018 financials highlights presentation

Covestro entered into a new stage of its strategy in 2019, which follows two stages since its 2015 IPO:

- The 2015-2016 period was the initial phase of establishing the business based on Bayer’s organizational set-up and the creation of a new culture driven by the above-mentioned key metrics. The timing of the IPO was right considering the normal supply-demand conditions of the industry and mid-cycle margin levels in 2015 to 2016.

- 2017 and 2018 have been strong years on the back of tight supply conditions and margins at historic peak levels, and priority was put on output maximization and minimization of disruptions.

- In the period 2019 to 2021, Covestro intends to focus on increased efficiency, which includes maximizing portfolio synergies and streamlining standard businesses while extending differentiation and cost leadership.

In view of the current slowdown of its activities, Covestro has completed a significant buyback program of 20 million shares for a total of 1.5 billion euros since November 2017. A new share buyback program will be voted at the next annual general meeting for up to 10% of share capital, suggesting that Covestro’s management perceives the currently depressed share price as an opportunity to acquire shares well below fair value.

2. Management

The management of Covestro AG is divided into two different boards: the board of management and the supervisory board.

The board of management positions are held by CEO Dr. Markus Steilemann (who is also chief commercial officer), Chief Technology Officer Dr. Klaus Schäfer and Chief Financial Officer Dr. Thomas Toepfer.

The supervisory board has 12 members: Chairman Dr. Richard Pott (former member of the board of management and labor director of Bayer AG), Vice Chair Petra Kronen and 10 other members.

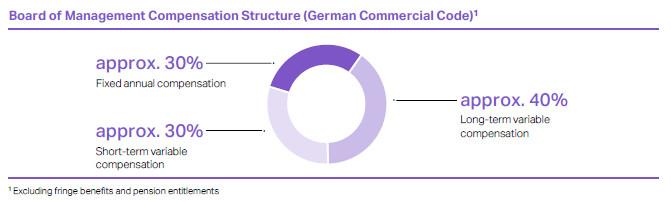

2.1 Compensation

The company has a compensation system for the members of its board of management and supervisory board. This system complies with the requirements of the German Commercial Code.

The structure of the compensation system for the board of management is presented in the figure below:

Source: Covestro Annual report 2018

The members of the board of management are eligible to participate in the Prisma compensation program as long as they remain in the service of the Covestro Group and acquire for their own account and hold Covestro shares according to defined policies. This program is based on a target opportunity set at 130% of the fixed annual compensation. When a member of the board of management retires, current tranches may be shortened, thus reducing their value.

2.2 Company’s ownership

As of end of February 2019, the following shareholders were holding shares of the Group:

Bayer AG: 8%

Free float: 92%

It has to be noted that this ownership evolved dramatically during the year 2018. According to the 2018 Covestro annual report, Bayer AG held 35% of the shares before initiating a massive 12% share reduction to 23% during January 2018. Then, in May 2018, another massive sale of shares operated by Bayer AG took place to reduce its shares from 23% to roughly 8%. The total block of shares from the two operations was aimed exclusively at institutional investors. Accordingly, the free float increased from 65% to 92% during the year 2018.

3 Company’s performance

3.1 Operating performance

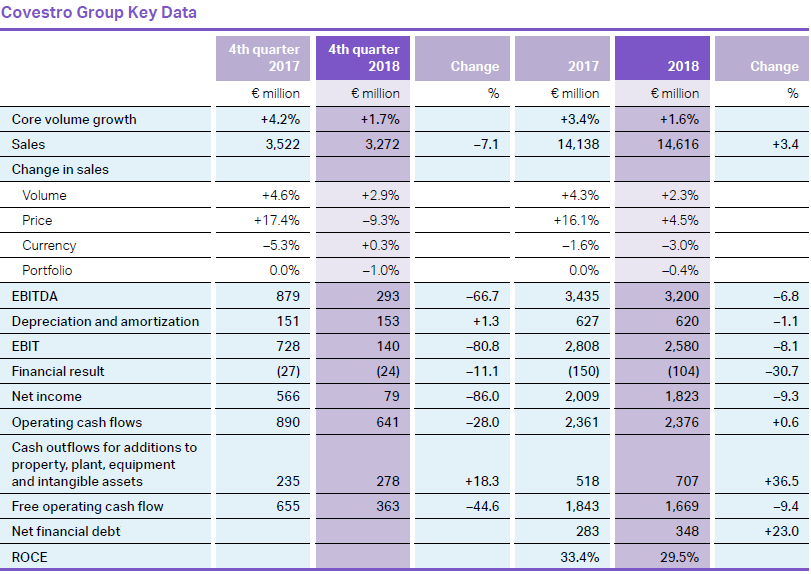

Covestro AG booked a solid fiscal 2018 thanks to a very strong first half. Global core volume growth grew 1.6% year-over-year, mainly driven by Asian demand. The group managed to secure net free operating cash flow (FOCF) of 1.7 billion euros, down 9.4% from 2017 and with an Ebitda-FOCF conversion rate at 52%. Working capital-sales ratio was up year-over-year at 16.2% in 2018 versus 15.4% in 2017.

Despite a challenging fourth quarter of 2018, the company managed to maintain Ebitda at a robust level, slightly down from 2017. Ebitda margin decreased to 21.9% versus 24.3% in 2017, which remains strong nevertheless. The sharp Ebitda decline in the fourth quarter of 2018 is due to pronounced negative pricing delta and seasonality, which we believe is mainly cyclical and not structural.

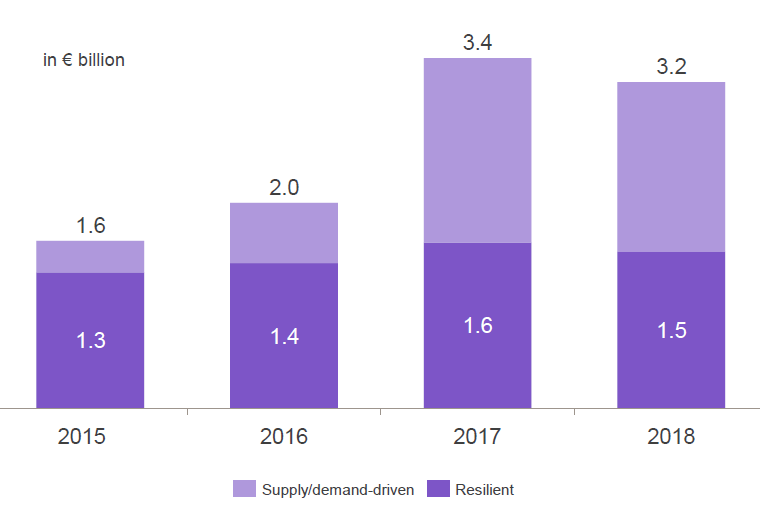

Covestro’s management expects negative pricing delta effects for 2019 and has already proactively warned investors about anticipated margin compression, below mid-cycle margins. Despite these negative expectations, resilient businesses such as CAS, Polyols, half of PCS volumes and a quarter of MDI volumes, are expected to keep the company afloat and profitable as they generate between 1.3 billion and 1.6 billion euros in Ebitda under normal economic conditions.

Evolution of Ebitda components over the last four years:

Source: 2018 financials highlights presentation

Source: Covestro Annual report 2018

3.2 Financial situation

The company is run by vigilant leaders:

On July 30, 2018, Covestro’s credit rating was upgraded by Moody’s from Baa2 to Baa1 with stable outlook. This assessment by Moody’s was justified by consistently strong operating cash flows in recent years and a faster paydown of debt.

Book value per share has continuously trended upward, and the debt/equity ratio downward. The level of financial debt is low compared to peers. Ebit covers more than 28 times the interest payments, the current ratio is comfortable (2.19) and the return on equity (ROE) stands at 42%, which compares favorably to the industry median of 9.43%.

Management is properly incentivized as explained earlier in the Strategy and Compensation sections.

The company has long-term prospects:

Covestro has a strong and diversified portfolio of products, a large share of resilient businesses and is well positioned in key growth sectors that will exhibit high demand for its products in the years to come.

The company is stable and understandable:

The group's book value has increased by 20.3% annually since its initial public offering in 2015.

It has strong know-how and expertise to foster innovation in sustainable polymers.

It has a clear strategy driven by cost efficiency, extended differentiation and maximization of portfolio synergies.

It has a clear and effective incentive system for employees, contributing to its moat.

3.3 Market valuation of the company

The share price stood at 90 euros at the start of 2018 and collapsed over the following months. As a result, the price-earnings ratio declined sharply from 9 to the current level of 4.36, which looks extremely cheap considering the size of Covestro’s business, well below its median of 10.2 and industry median of 18.54.

Similarly, the price-book ratio appears very cheap and is now at 1.72, down from the highs of late 2017 and early 2018 around 3.5.

The company’s shares can be acquired at an attractive price:

Price-Graham number is 0.57.

The margin of safety is 61% (fair value 125.51 euros based on DCF valuation).

Low historical price-earnings ratio (4.36).

Low historical price-book ratio (1.72).

Low historical price-free cash flow (5.14).

Covestro is a multi-billion dollar business listed on the DAX, the benchmark index with the 30 most important listed companies in Germany. It represents a rare opportunity to acquire one of the top German polymer producers at a very attractive price, and thus benefit from the know-how and growth in this sector with a strong expected return.

4. Risks

In terms of business environment, a slowdown in global economic conditions and, in particular, in China and the other geographic regions in which Covestro operates, may affect the company’s earnings, owing to the cyclical nature of Covestro’s business, as part of the polymer industry.

Covestro may be exposed to the risk of negative publicity, which may harm its reputation, due to the fact that it is part of the chemistry industry. The development of a negative social perception of the chemical industry in general or Covestro’s processes or products in particular could have a negative impact on the company. The incorrect use and handling of its products by third parties can also harm the company’s reputation.

In addition, concerns about product safety and environmental protection could influence public perceptions regarding Covestro’s products and operations. Covestro might also suffer from negative headlines related to Bayer AG, a group of which Covestro was part before 2015, in particular in the context of the controversial and expensive takeover of Monsanto.

As regards production and supply chain, risks associated with the production, filling, storage or shipping of products seem contained through integrated quality, health, environmental protection and safety management. The materialization of such risks may result in personal injury, property and environmental damage, loss of production, business interruptions as well as liability for compensation payments.

In terms of implementation risks and compliance, Covestro uses large quantities of hazardous substances, generates hazardous wastes and emits wastewater and air pollutants in its production operations. Consequently, its operations are subject to extensive environmental, health and safety laws, regulations, rules and ordinances in multiple jurisdictions. The company must dedicate substantial resources to complying with these regulations and the additional voluntary commitments. Costs relating to the implementation of and compliance with these requirements are part of Covestro’s operating costs and must therefore be covered by the prices at which the company is able to sell its products.

Operations at some sites may be disrupted by natural disasters, fires, explosions or supply shortages for Covestro’s principal raw materials or intermediates. These risks are mitigated by distributing production for certain products among multiple sites and by building up safety stocks. An obvious recent example is the low level of the Rhine River, which in 2018 disrupted an important transportation channel for supply and final products, and caused some harm to Covestro’s profitability. There is an obvious trend with regards to the Rhine water level going down year after year on the back of climate change. But this element is already largely priced in at this stage, as the company would be able to find alternative routes over time.

Disclosure: The author owns shares of Covestro at the time of writing.

Read more here:Â

GuruFocus Value Idea Contest: January and February Update