1. The company

NetEnt AB (OSTO:NET B)

As of April 19:

Number of shares: 240 million

Free float: 166 million

Share price: 30.23 Swedish krona

Market cap: 7.22 billion Swedish krona (around 650 million euros)

NetEnt AB is involved in the online gaming business. Its share price has fallen below 30 krona for the first time since 2014, on the back of slowing growth and a downgrade by Norwegian bank DNB at the start of April 2019.

The company’s outlook remains good: Fundamentals are strong with solid revenues and no debt. But the share price multiples are currently at 10-year lows, providing a cheap entry point with an attractive risk-reward tradeoff.

1.1 History and market overview

NetEnt is a market-leading digital entertainment company that develops gaming and system solutions for the world’s most successful gambling operators. The product offering of this Sweden-based company comprises around 200 game titles in 24 languages and a powerful technical platform with hosting and 24-7 support. NetEnt and its customers, the casino operators, use a partnership model, whereby NetEnt is responsible for operation and monitoring of gaming transactions. Gambling operators pay royalties to NetEnt based on a percentage of the game win (player bets less player wins) generated by NetEnt’s games.

Founded in 1996, this small-cap, tech-driven company has grown fast with reliable and predictable income streams from consistent small-ticket transactions. As of 2019, it has reached a leading market position in Europe as a supplier to the digital casino industry with around 1,000 employees. Annual sales amounted to 1.782 billion krona and operating profit was 601 million krona in 2018.

Market overview

The online gaming market has grown steadily in recent years. Global revenues for online gaming, including all game segments, has been estimated at 40.5 billion euros for 2017, an increase of 9% compared to the previous year. The corresponding size of the global online casino market has been estimated at 10.6 billion euros in 2017, an increase of 9% from the year (source: H2 Gambling Capital, February 2018).

Europe is by far the largest gaming market and is expected to represent close to half of the gross gaming yield in the coming years. Deregulation and reregulation of national gaming laws is also taking place in many European countries. NetEnt has had a local license since 2015 in the U.K., the largest gaming market in Europe where new regulation was introduced in 2014. As a result, all operators offering gaming services to British players need to have a British gaming license and pay gaming taxes in the U.K., regardless of where the operator is based.

In Italy, all NetEnt’s game traffic now takes place through licensed operators. The market in Denmark was regulated in 2012, and NetEnt’s games are offered through several operators, including Danske Spil.

Online gaming is regulated in Spain, where NetEnt holds a gaming license, and its games have been available with several customers since 2015. The online gaming markets have recently been regulated in Portugal, Romania, Bulgaria and the Czech Republic. In Romania, NetEnt obtained a gaming license and launched its games with several operators during 2016. In Bulgaria and Portugal, NetEnt’s games were certified and launched with customers in 2016.

New gaming legislation is expected in the Netherlands towards the end of 2018. In Sweden, the gaming commission presented its proposal for new gaming legislation in March 2017 and according to the government, the new legislation will be introduced in the beginning of 2019, which is likely one of the main drivers of NetEnt’s recent share price decline.

Currently the majority of NetEnt’s customers are in Europe, which is expected to remain the focus, but expansion into North America is also expected to contribute to long-term growth. In the U.S., a few states have opened for online gaming: Nevada (poker), Delaware (all games) and New Jersey (all games). Political steps towards reregulation have also been taken in other states, for example in Pennsylvania. NetEnt has applied for a license in New Jersey and has been granted transactional waivers to launch games with several operators in the state, while its full license application is being reviewed.

NetEnt is continually monitoring developments in other U.S. states that are close to regulating, and the company intends to launch its products in these markets if the conditions are right. In Canada, the market is regulated and open for online casino in several provinces such as Ontario, British Columbia and Quebec. As a first step to enter Canada, NetEnt has applied for and obtained a license in British Columbia.

1.2 Business model

NetEnt runs a partnership model in which it is responsible for hosting, operating and monitoring gaming transactions while gaming operators pay royalties to the company based on a percentage of the games' gains generated, known as the game win (players’ bets less players’ wins).

NetEnt is a business-to-business company developing and distributing premium software (games and gaming solutions) to online casino operators globally. Revenues are generated according to a licensing model based on revenue-sharing with customers. Customers and the gaming operators pay a monthly royalty fee to NetEnt, which is based on a certain percentage share of the gross game win that is generated in the customers’ online casinos. NetEnt takes responsibility for all technical operations such as monitoring gaming transactions for its customers, known as hosting, so that the operators can focus on their core operations. NetEnt also plays an active part in the integration work for new customers.

NetEnt has a flexible and scalable product offering, and the company has pledged to release more games than it ever has in a single year in 2019. As a leading supplier to the digital casino industry in Europe, NetEnt’s ambition is to drive the digital casino market through better gaming solutions.

1.3 Strategy

NetEnt’s overall objectives are to further strengthen its position as a leading global supplier of online casino games and system solutions, drive development and grow faster than the market.

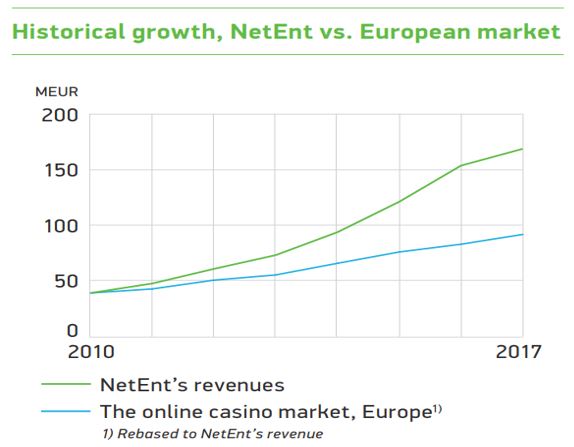

Since 2007, NetEnt has increased its revenues by 29% annually, while the online casino market in Europe has grown by 16% annually over the same period. In 2017, revenues grew by 11.7%, compared to estimated market growth of 10.7% in Europe.

Source: Company year-end report 2018

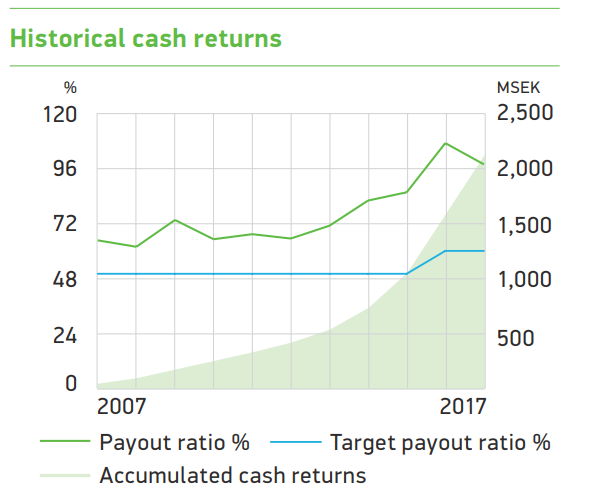

With no debt, NetEnt aims to pay dividends of a minimum of 60% of net profit after tax, taking the company’s long-term capital requirement into account. The board’s target is for ordinary dividend payout to grow in line with earnings per share. The 2018 proposed dividend is 2.25 krona per share, unchanged from the previous fiscal year.

Source: Company year-end report 2018

2. Management

The board of directors has overarching responsibility for NetEnt’s organization and administration in the form of establishing business goals and strategies, evaluating executive management and securing systems for monitor and control of established goals.

Between annual general meetings, the board of directors is the company’s highest governing body. The board is elected by the shareholders at the AGM with a mandate period extending from the AGM until the end of the following AGM.

The 2018 board of directors includes:

- Jenny Rosberg (who owns 15,600 B shares).

- Peter Hamberg (who owns 1,218,000 A shares, 580,400 B shares and 150,000 B shares in endowment policy).

- Maria Hedengren (who owns 19,000 B shares).

- Pontus Lindwall (who owns 4,100,000 B shares, 2,109,000 A shares in endowment policy and 760,520 B shares in endowment policy).

- Maria Redin (who owns 11,880 B shares).

- Fredrik Erbing (who owns 120,000 B shares and 120,000 B shares in endowment policy).

- Michael Knutsson (6,000,000 A shares and 8,600,000 B shares).

Apart from the CEO, NetEnt senior management includes six more people, four of whom are women. The CEO is appointed by and receives instructions from the board of directors. In turn, the CEO appoints the other senior management members and is responsible for ongoing administration of the group’s operations in accordance with the guidelines and instructions of the board.

2018 senior management of NetEnt includes:

- Anna Romboli, communications director (who owns 2,000 B shares).

- Camila Arvidsson, enterprise risk manager (who owns 2,932 B shares and 13,800 stock options).

- Pamela Morris Williams, chief compliance officer.

- James Elliott, general counsel (who owns 7,600 stock options).

- Therese Hillman, CEO (who owns 8,065 B shares and 40,000 stock options).

- Lars Johansson, chief financial officer.

2.1 Compensation

In terms of compensation and share holding, NetEnt’s Board members and employees appear adequately incentivised. The AGM determines remuneration for board members. At the AGM on April 25, 2018, it was resolved that for the period until the 2019 AGM, that board member fees would be 2.72 million krona, of which 710,000 krona goes to the board chairman and 305,000 krona goes to each of the other members of the board, with an addition of 110,000 krona for the chair of the Audit Committee and 35,000 krona to the other members of the Audit Committee.

In 2018, total remuneration to the current and former CEO was 3.924 million krona, of which 226,000 krona was variable remuneration, 771,000 krona was pension benefits and 415,000 krona was loyalty bonus costs. Remuneration for other senior executives in 2018 amounted to 15.331 million krona, of which variable remuneration was 472,000 krona, pension benefits totaled 2.063 million krona and loyalty bonus costs were 213,000 krona.

Employees are offered the chance to take part in share-based incentive schemes in the form of stock options or stock saving programs that are issued on market terms to motivate long-term commitment and promote a greater alignment of interests with the company’s shareholders. In order to strengthen loyalty to the company, share-based incentive programs in the form of stock options issued on market terms can be combined with cash remuneration, which is payable in connection with the redemption period during which stock options can be exercised, to employees who are still employed at the time of redemption. Such remuneration may not exceed 70%, net after tax, of the premium paid for the stock option. The company’s cost of loyalty remuneration is recognized on an ongoing basis over the vesting period.

Considering the elements above, the existing corporate governance structure and senior management incentives appear sound enough for the long-term growth of NetEnt.

2.2 Company ownership

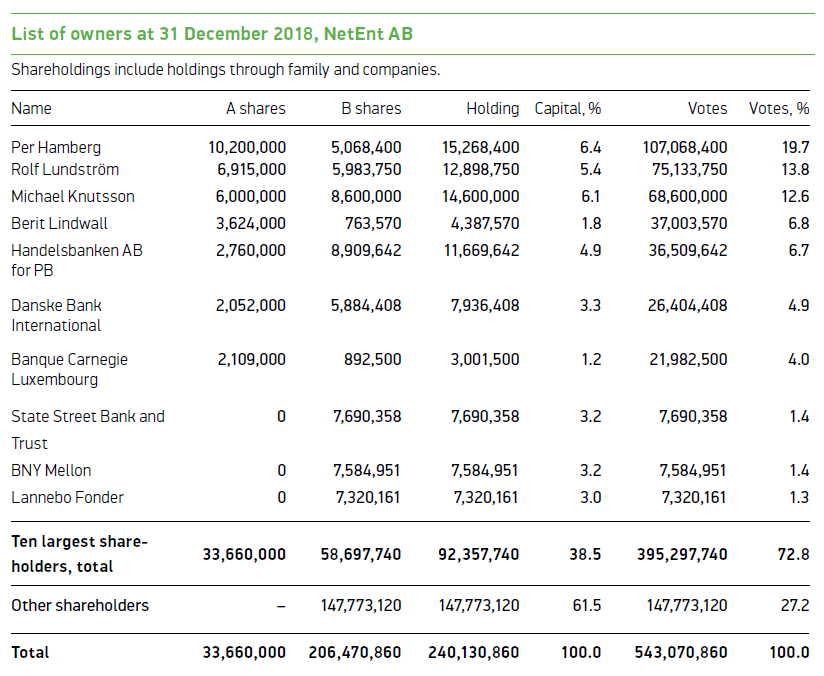

As of Dec. 31, 2018, two members of the board of directors were among NetEnt’s 10 largest shareholders and held more than 32% of the voting rights for 12.5% of the company’s equity:

Source: year-end report 2018

3 Company’s performance

3.1 Operating performance

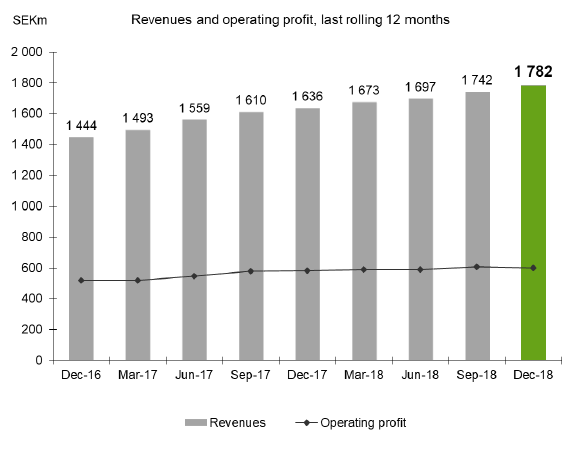

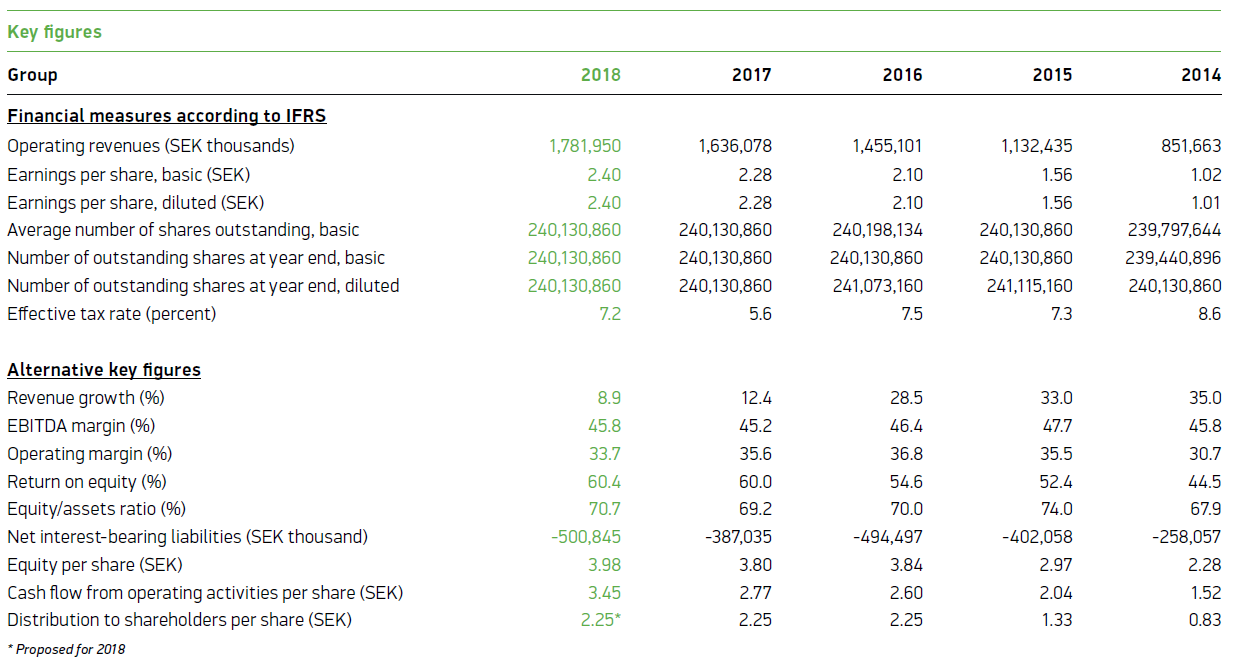

Revenues in 2018 decelerated to a single-digit growth rate after years of double-digit growth rates. During the period of January to December 2018, they amounted to 1.782 billion krona (versus 1.636 billion in 2017), an increase of 8.9%, boosted by a weaker Swedish krona against the euro. But the results marked a deceleration from previous years' double-digit growth rates. Revenues, which are mostly based in euros, increased by 2.3% compared to the same period in 2017. Nevertheless, the potential to grow further remains intact, and the outlook is favorable with a dynamic environment.

The company’s growth is driven by new license agreement and new customers’ casinos. NetEnt signed 31 new license agreements during the period and launched 38 new customers’ casinos. For 2019, NetEnt plans to release more games than it ever has, with a target between 30 and 35 games (it released 21 in 2018).

Profitability increased further despite slightly lower operating margin. Operating profit amounted to 601.1 million krona, compared to 581.6 million a year earlier, and the operating margin was 33.7%, compared to 35.6%. Adjusting for reorganization-related costs and the writedown of a virtual reality project, operating profit was 634.5 million, versus 581.6 million, and operating margin was 35.6%, versus 35.6%.

Â

Source: Company year-end report 2018

Earnings per share doubled over the last five years. Earnings per share continue their steady increase from 1.02 krona in 2014 to 2.40 krona in 2018, fueled by steady cash flows from operating activities.

Source: Year-end report 2018

3.2 Financial situation

The company is run by vigilant leaders:

NetEnt has no debt on its balance sheet. As of the end of 2018, the current ratio is at a comfortable level of 2.3, and the return on equity stands at 60.4%, which compares favorably to the rest of the industry.

The company has long-term prospects:

The gaming industry is expected to show robust growth in the next five to 10 years. NetEnt is extremely well positioned with a broad set of licenses ensuring strategic geographical diversification and contracts with key casino operators globally.

The company is stable and understandable:

The Group’s book value has grown on average by 30% annually over the last 10 years, albeit slowing recently (by 5% over the last 12 months).

NetEnt prioritizes geographical expansion on locally regulated markets, where it has a competitive edge through its experience and expertise.

The strategy is clear and driven by cost efficiency, focused geographic expansion on regulated markets and relentless creation of innovative high-quality games.

Moat: The company is a market leader with a diversified geographical presence and customer portfolio.

Source: Year-end report 2018

Source: Year-end report 2018

3.3 Market valuation of the company

The share price stood at 56 krona at the start of 2018 and collapsed over the following months to as low as 29.72 in April 2019. As a result, the price-earnings ratio declined sharply from 25 at the start of 2018 to the current level of 12.5, well below the industry median of 24.79, which looks extremely cheap considering it is a growth stock.

Similarly, the price-book ratio appears very cheap and is now at 7.55, down from the highs of around 30 in mid-2017.

The company’s shares can be acquired at an attractive price. As of April 15:

The margin of safety is 58% (fair value 71.46 krona based on DCF valuation model).

Low historical price-earnings ratio (12.5).

Low historical price-book ratio (7.55).

Low historical price to free cash flow (8.7).

4. Risks

One global risk can be identified that may impact the valuation of the whole sector. The environmental, social and governance (ESG) initiatives and the global drive towards responsible investment may succeed in changing investors’ perception towards gaming and lead some investors to underweight stocks classified as gaming companies.

Risks to NetEnt’s operations overall can be assessed to be reasonable to fairly low. NetEnt’s operations are exposed to risks that may impact earnings or financial position. They can be divided into industry, operational and financial risks.

Industry

The main risks that pertain to the industry in which NetEnt operates are regulatory and competitive. As NetEnt expands geographically, the revenue base becomes more diversified as dependence on political decisions in individual countries decreases. NetEnt is in continuous dialog with authorities and legislators on key markets regarding new or amended regulations and is arguably in a favorable position in comparison to competition since it has developed experience and expertise in implementing regulatory changes in various countries. Moreover, NetEnt actively assists regulators in devising sustainable regulations in line with customer demand and the reality prevailing in the cross-border digital market.

Operational

Operational risks faced by NetEnt include sustainability, dependence on large customers and exposure to business cycles. In order to retain key people within the organization, NetEnt continually works to remain an attractive employer by providing share-based incentive schemes and superior working conditions. Dependence on large customers and exposure to business cycles diminish as the company expands globally.

Financial

Financial risks encompass mostly the foreign exchange risk, liquidity risk, interest rate risk, credit risk and capital management risk. Most sales are in euros, whereas liabilities are mostly in Swedish krona, and no currency hedging is carried out at the moment, leaving the company exposed to euro-krona fluctuations. As of the end of 2018, NetEnt had no external loans or credit facilities, which implies low interest rate risks.

No single customer accounts for more than 6% of the company’s total revenues, and the three largest customers account for 14% of total revenues. This diversification of the customer base mitigates the credit risk exposure of NetEnt. The company’s financial liabilities essentially consist of accounts payables, which are largely covered by cash and cash equivalents to finance operations (strong current ratio close to 1.83), thus implying a low liquidity risk. As of the end of 2018, the company had no external liabilities to finance its operations: Capital consists of equity and the dividend policy is in the form of share redemptions.

Disclosure: The author owns shares of NetEnt at the time of writing.

Read more here:Â

Value Idea Contest: Hong Leong Industries Bhd

Value Idea Contest: National Beverage Corp is Interesting at Current Valuation

Value Idea Contest: Aspen Pharmacare

Not a Premium Member of GuruFocus? Sign up for a free 7-day trial here.

Â

Â