Long-established in the agriculture industry, The Mosaic Co (MOS, Financial) has enjoyed a stellar reputation. It has recently witnessed a daily gain of 0.62%, juxtaposed with a three-month change of 31.8%. However, fresh insights from the GF Score hint at potential headwinds. Notably, its diminished rankings in financial strength, growth, and valuation suggest that the company might not live up to its historical performance. Join us as we dive deep into these pivotal metrics to unravel the evolving narrative of The Mosaic Co.

Understanding the GF Score

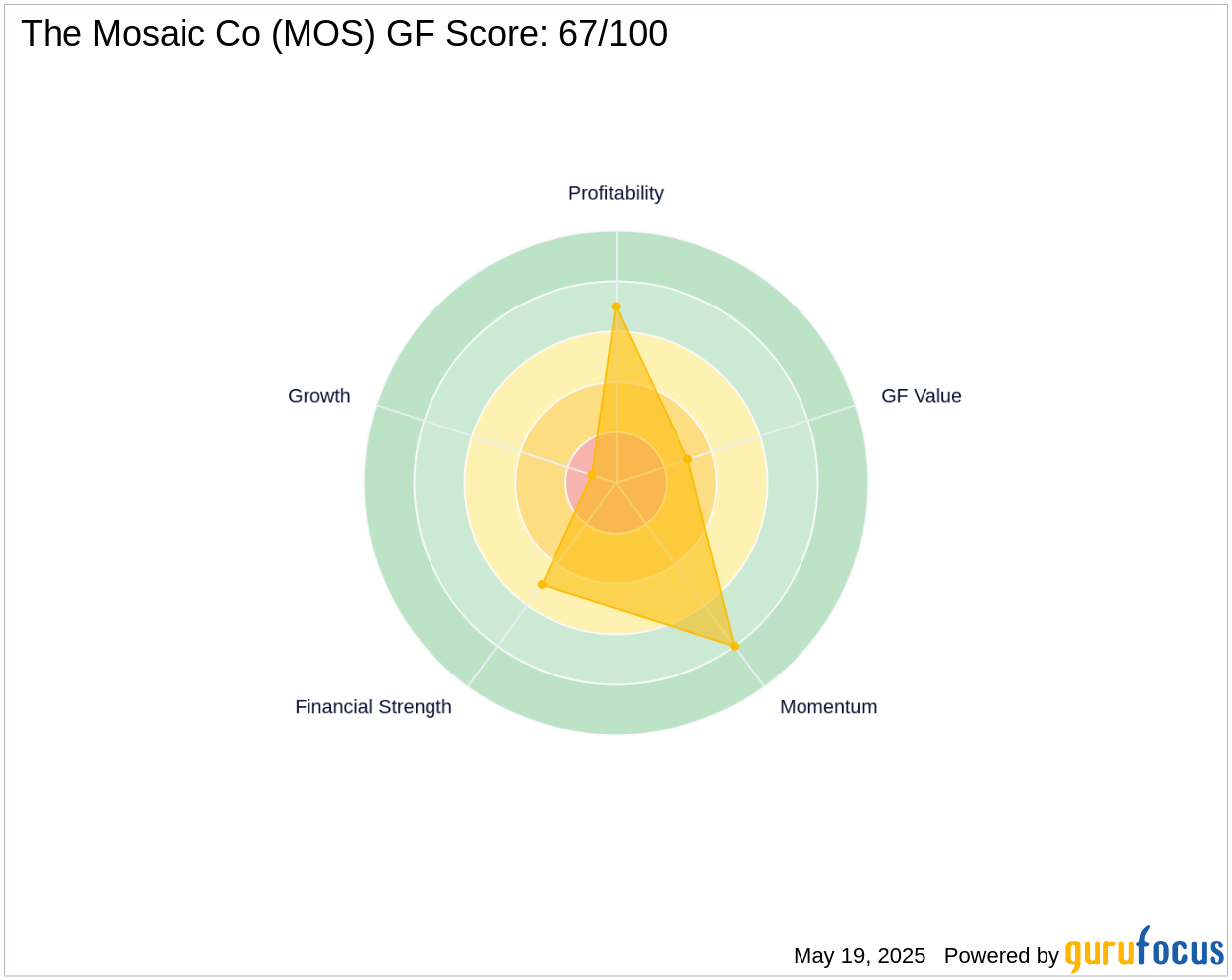

The GF Score is a stock performance ranking system developed by GuruFocus using five aspects of valuation, which has been found to be closely correlated to the long-term performances of stocks by backtesting from 2006 to 2021. The stocks with a higher GF Score generally generate higher returns than those with a lower GF Score. Therefore, when picking stocks, investors should invest in companies with high GF Scores. The GF Score ranges from 0 to 100, with 100 as the highest rank.

- Financial strength rank: 5/10

- Profitability rank: 7/10

- Growth rank: 1/10

- GF Value rank: 3/10

- Momentum rank: 8/10

Based on the above method, GuruFocus assigned The Mosaic Co the GF Score of 67 out of 100, which signals poor future outperformance potential.

Company Overview

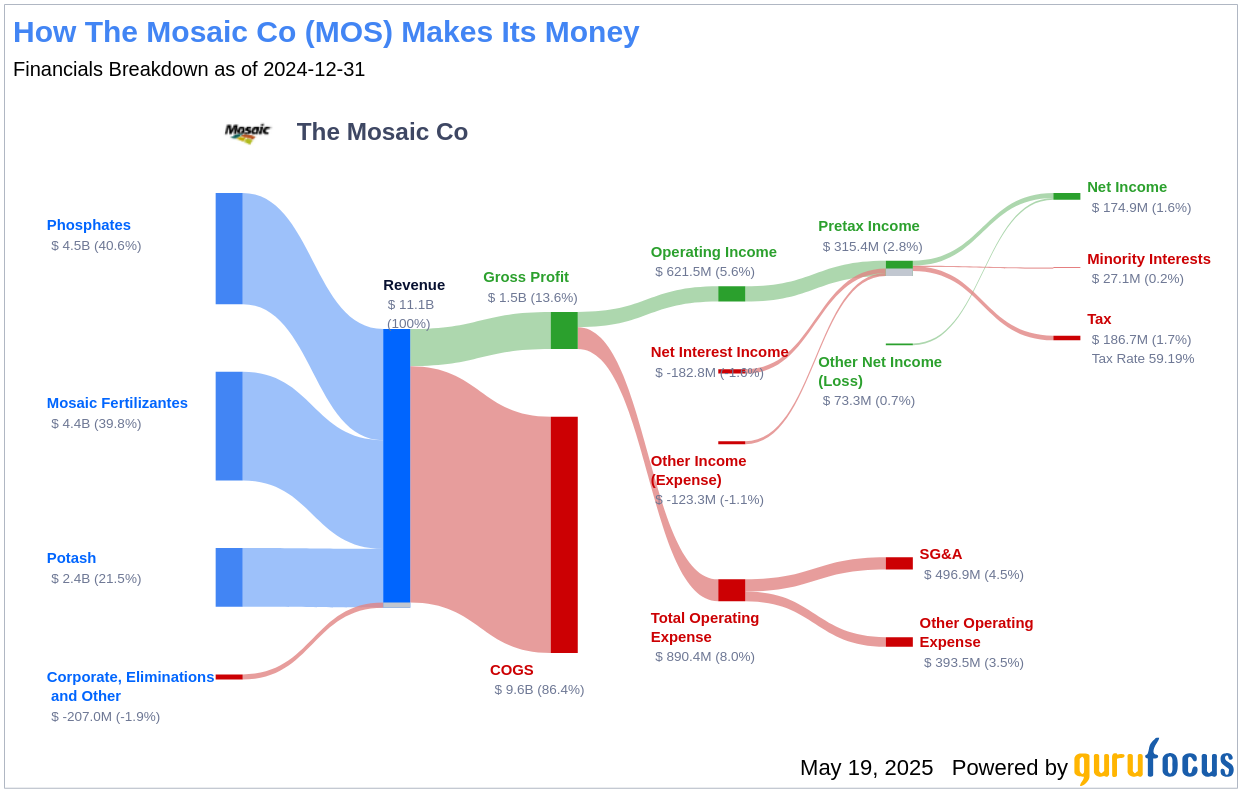

The Mosaic Co is one of the largest phosphate and potash producers in the world, with a market cap of $11.24 billion and sales amounting to $11.06 billion. The company operates phosphate rock mines in Florida, Brazil, and Peru, and potash mines in Saskatchewan, New Mexico, and Brazil. Additionally, Mosaic runs a large fertilizer distribution operation in Brazil through its Mosaic Fertilizantes business. Despite its vast operations, the company has an operating margin of 7.11%, which may not be sufficient to drive significant growth.

Financial Strength Breakdown

The Mosaic Co's financial strength indicators present some concerning insights about the company's balance sheet health. The Mosaic Co has an interest coverage ratio of 3.51, which positions it worse than 67.02% of 191 companies in the agriculture industry. This ratio highlights potential challenges the company might face when handling its interest expenses on outstanding debt. It's worth noting that the esteemed investor Benjamin Graham typically favored companies with an interest coverage ratio of at least five.

The company's Altman Z-Score is just 2.07, which is below the safe threshold of 2.99. Although this does not imply immediate danger of financial distress, the stock may face some financial struggles if the Altman Z-score drops below 1.81. Additionally, the company's low cash-to-debt ratio at 0.05 indicates a struggle in handling existing debt levels.

Growth Prospects

A lack of significant growth is another area where The Mosaic Co seems to falter, as evidenced by the company's low Growth rank. Lastly, The Mosaic Co predictability rank is just one star out of five, adding to investor uncertainty regarding revenue and earnings consistency.

Conclusion

The Mosaic Co's financial strength, profitability, and growth metrics, as highlighted by the GF Score, suggest that the company may face challenges in achieving future outperformance. While the company remains a significant player in the phosphate and potash industry, its current financial indicators and growth prospects raise concerns about its ability to maintain its historical performance. Investors should carefully consider these factors when evaluating the potential of The Mosaic Co. For those seeking companies with stronger GF Scores, GuruFocus Premium members can explore more options using the following screener link: GF Score Screen.

This article, generated by GuruFocus, is designed to provide general insights and is not tailored financial advice. Our commentary is rooted in historical data and analyst projections, utilizing an impartial methodology, and is not intended to serve as specific investment guidance. It does not formulate a recommendation to purchase or divest any stock and does not consider individual investment objectives or financial circumstances. Our objective is to deliver long-term, fundamental data-driven analysis. Be aware that our analysis might not incorporate the most recent, price-sensitive company announcements or qualitative information. GuruFocus holds no position in the stocks mentioned herein.