Most companies achieve growth status at the expense of near-term profitability. Amazon (AMZN) and Tesla (TSLA) are just couple of examples. However, companies like Facebook (FB) are profitable even in their growth phase. That's why Facebook deserves premium valuation. AÂ recent research piece from a Seeking Alpha contributor pointed out that Facebook is, in fact, not profitable. The author built his case on several arguments including the following:

- GAAP wrongly favors acquisition over internal development. Had Facebook developed apps internally, it would've incurred losses.

- Facebook's recent acquisitions are unprofitable, and the company is chasing, already tapped, advertisement market.

- Acquisitions are overpriced. Consequently, Facebook will write off goodwill in the future.

Facebook is profitable. GAAP doesn't favor acquisitions. Facebook's acquisitions will be profitable, and the acquisitions are not overpriced. Further, goodwill's write-off can't be predicted with certainty. The author compared Facebook to Amazon, but we'll stick to Facebook owing to the fact that Amazon is trading at lofty valuation and extensive research isn't required to prove that.

Back to Facebook, let's start with the GAAP discrepancy the author mentioned. Assets are acquired or internally built envisioning future economic benefits. The decision to acquire those assets can be good or bad. Same holds true for internal development. In case of poor internal development, related assets are written off and losses are incurred. Now, the approach used to gain future economic benefit doesn't affect the benefit; it's the quality of asset acquired or built. Facebook acquired WhatsApp, and Amazon built AWS. Write-offs can occur in both cases if respective products fail to gain traction in coming years. All in all, whether a product is internally developed or acquired, the risk of write-offs is present in both cases. Facebook's acquistion strategy can't be criticized simply because write-off risks are invloved. The point is that the possibility of a write-off with goodwill doesn't mean that GAAP favors acquisition.

Further, a capital surplus was also created to balance the goodwill, in the case of WhatsApp. Facebook issued 178 million shares that resulted in dilution, and EPS came under pressure as a result. In case of internal development, equity offerings or cash are used for financing purposes. All in all, financial impact of GAAP accounting is effectively the same for acquisitions or internal developments.

The case of arguing against goodwill treatment is same as saying that GAAP favors land acquisition over machinery. Why isn't the expense of acquiring land reflected in the income statement? Well, it's because of the perpetual nature of land. Same goes for the acquired goodwill. WhatsApp is a going concern and can't be amortized. If someone disagrees, please propose a denominator for the amortization calculation.

One other thing is that internal developments are also capitalized in the form of assets and intangibles. No expenses are shown on the income statement. And, if a company sells its internally developed assets, it gets a premium. That's the goodwill attached to internal development. Amazon's goodwill is already priced in its market cap. And, we can just speculate on how much of a write-off the market will slap on that going forward. The point is that if Amazon is not amortizing the intangible value it can get from selling AWS, for instance, then why should Facebook amortize the going concern assets it acquired?

To review, EPS is affected the same whether we acquire an asset or develop it internally. In acquisitions, EPS is affected by dilution. Internally developed assets are also capitalized. Hence, no expense is recognized. The effect on the EPS, in that case, can come from financing activities only.

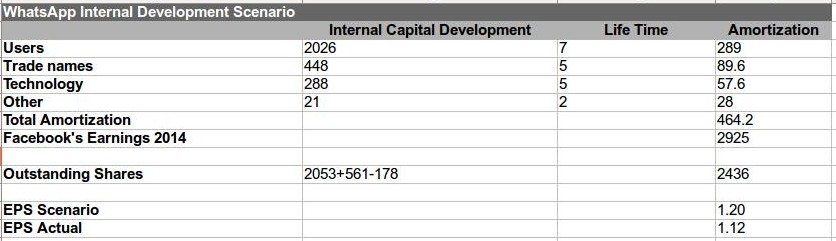

The other part of the author's first argument is that, if Facebook developed internally, it would've incurred losses. We strongly disagree. Acquisitions are naturally expensive as they entail premium; internal developments don't entail that. See the following sheet to get a clear picture.

Focus Equity Estimates, Amounts in million

It is assumed that Facebook developed WhatsApp for the amount it uses, in the balance sheet, for its limited-time intangibles related to WhatsApp. In reality, the cost of developing WhatsApp would've been less than that. Total amortization, for the internally developed assets, amounts to $464.2 million. Note that outstanding shares should be adjusted for 178 million shares as the company isn't paying any premium in this scenario. The projected EPS for Facebook is $1.20 as compared to the actual EPS of $1.12 during year ended 2014. And that's because internal development doesn't entail premium and risk of dilution. Yes, amortization is increased but adjustments in share count made up for that. All in all, Facebook would've been profitable irrespective of its approach to WhatsApp.

Another point raised against Facebook is that its acquisitions are unprofitable. It's true for now as the company is not actively monetizing its acquired assets. Let's take WhatsApp, for instance. The company is going to charge around $1 per year for subscription. That's $900 million a year for foreseeable future. Note that subscriber growth hasn't halted yet. Regarding the criticism about chasing advertising dollars, mobile is a growing advertisement market. Chasing that makes sense. Further, Facebook is efficientlymonetizing its mobile platform.

Regardless of that, the acquisitions' profitability argument, in itself, isn't potent. Facebook is not chasing advertising dollars only. It can tap into micro financial services market through its apps, especially in emerging markets. The company is already testing fund transfer service through its messenger app in the U.S. WhatsApp can be used as a platform to connect brands with consumers, and subscription is already in the cards. Further, emerging market users are going to settle for $1-$2 subscription amid WhatsApp's cost benefits over carrier texting. Another thing is that, WhatsApp users are smart phone owners, which have higher household incomes. So, comparing the average wages of developing markets with developed markets is a futile comparison. In effect, WhatsApp can easily generate $2 per MAU going forward. Cost of managing the platform is already being absorbed in the books of Facebook. Therefore, $2 per user will be the net addition to the income. See the projection below:

Focus Equity Estimates

The chart depicts that WhatsApp is a $5.4 billion NPV project for Facebook assuming earnings of $2 per user. Even with premium acquistion price of WhatsApp, Facebook seems in the money in terms of valuation. And, this is just the base case. Facebook is generating $2 per MAU from its Facebook platform without even charging subscription. WhatsApp can bring material advertisement dollars if the company decides to go that way.

To answer the criticism, Facebook's acquisitions will be profitable as depicted by the net present value of WhatsApp. The NPV calculation also answers the objection related to the price paid for the acquisition.

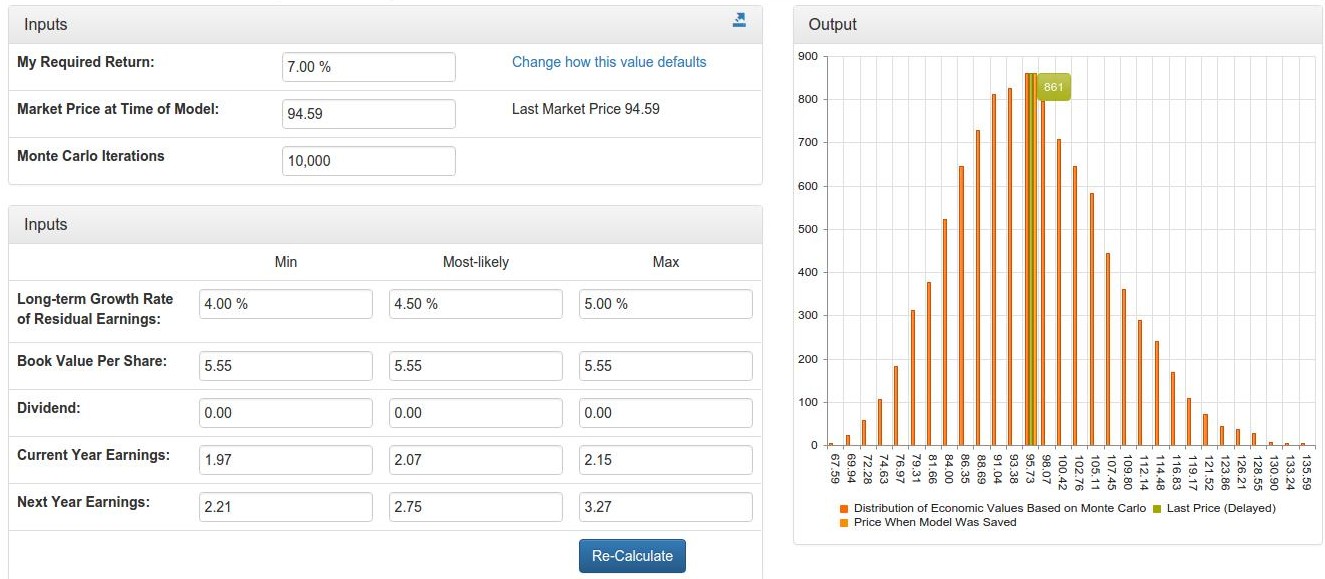

Let's see the value of Facebook using Monte Carlo simulation.

(click to enlarge) Source: Prudena

Source: Prudena

The chart reveals that Facebook is fairly valued based on a 7% required rate of return. However, we think that WhatsApp and Instagram monetization will take the stock higher.

Final Thoughts

Facebook is profitable as evident from the results, and it would've been profitable if it built WhatsApp internally. Facebook is making intelligent acquisitions in order to dominate the mobile revolution. WhatsApp is a positive net present value project. There is no evidence that Facebook will write-off goodwill. However, Monte Carlo valuation reveals minimum upside. But, the stock is a buy amid Facebook's domination in mobile space and upcoming catalysts including virtual reality and WhatsApp, Instagram monetization.