Procter & Gamble (PG, Financial) has indeed lost a lot of its mojo. The classic dividend payee of our century, operating in one of the most defensive sectors, has been seeing its revenues, earnings and cash flow sliding downwards, putting enormous pressure on it to keep its dividend growth story intact.

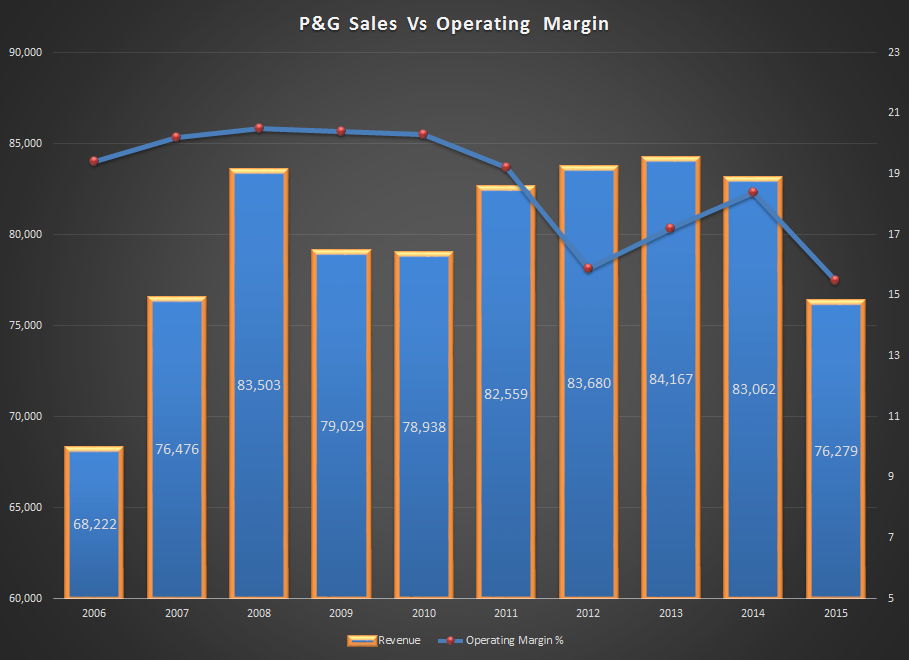

In the last 10 years, Procter & Gamble saw its revenues climb from $68 billion to $84 billion and then slide down to $76 billion. The company has been blaming macroeconomic conditions, commodity prices and overall growth of the market for the slowdown.

The company has also been divesting a lot of its products, such as Duracell to Berkshire Hathaway (BRK.A)(BRK.B), beauty brands like Clairol and Covergirl to Coty (COTY) for $12.5 billion, Hipoglós diaper cream to Johnson & Johnson (JNJ, Financial), and the Escudo brand of soap to Kimberly Clark (KMB, Financial) and so on.

“P&G said the 70 to 80 'core' brands it will focus on accounted for 90 percent of sales and more than 95 percent of profit over the past three years. Twenty-three of the brands have sales of between $1 billion and $10 billion.”

- Reuters

Now, if it was selling low-margin, low-growth brands from its portfolio and holding on to better performing ones, that could indeed have helped the company grow stronger with respect to operating margins, if not revenues. That does not seem to be the case, however. Why else would it have let go of Duracell, which has a huge market share and is an extremely predictable revenue source?

So, what the company has been doing is selling a mix of low- and high-performance brands from its portfolio, which does not really make sense for a company that needs better margins and revenue growth.

Let’s take a closer look at the phenomenon.

The Pricing Problem

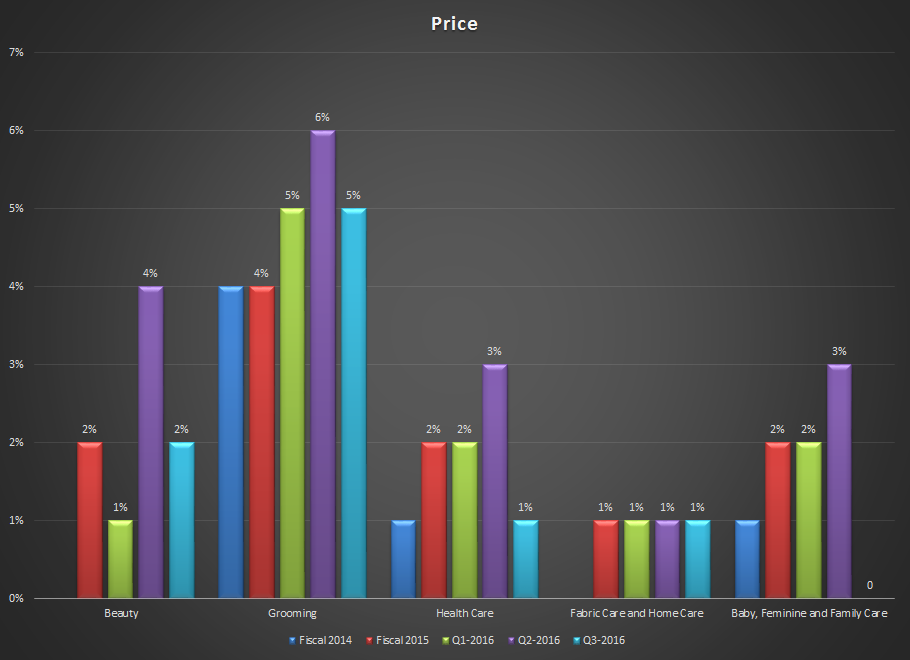

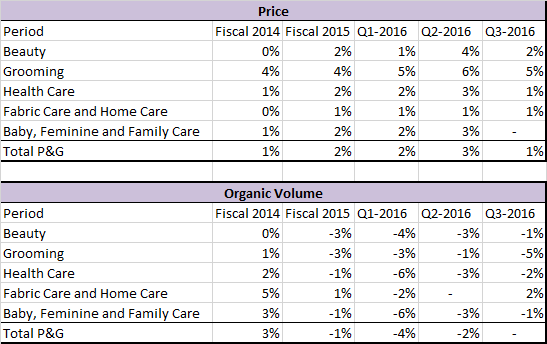

What you can clearly see from the data above is that price increases have been a staple at P&G since 2014 until the last reported quarter. While this is justifiable in a growing economy, sustained increases are bound to have a detrimental effect on any brand.

And that Procter & Gamble has been doing this with multiple brands was almost a guarantee that sales would ultimately drop because people would buy from the competition — simply because the competition in question was keeping their prices relatively steady. That is consumer behavior at its simplest form, and it is a pity P&G seems to have missed it.

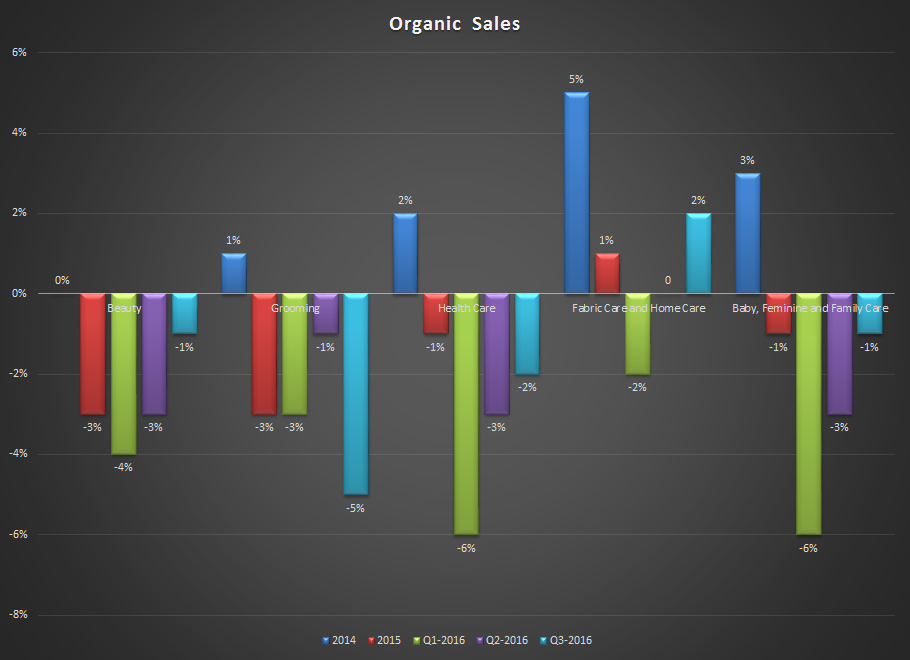

What we are seeing as a dip in sales volumes is simply a result of that sustained price increase strategy — nothing more. The market has and always will expect a consumer durables company to keep its top line growth intact in a stable economy, and that did not happen. It took the shortcut and kept pushing prices up. At some point, it had to give.

What the Future Holds for P&G

At the current size, things will not get any easier for Procter & Gamble. Macroeconomic conditions are against it, there is stiff competition everywhere it goes and it does not have that many options for brand acquisition at this point.

It is inevitable that the company will first have to shrink further in order to start growing again, but that is not going to happen by just selling off brands —Â especially if some of those brands are strong earners like Duracell.

The company clearly needs to hold onto its strongest brands, while looking at smaller, emerging brands to acquire. If revenues do not start showing an uptick soon, its dividends will continue to be under threat. Is has already announced one of the lowest dividend increases in its long history of payouts, so that problem is already knocking on its door.

At a forward price-earnings ratio of 20.2, the stock price still looks reasonable, but do not get in if dividend growth is what you are after. The next two years will show us exactly what direction P&G will take, and will ultimately reveal its growth plan for the next decade.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.